The central bank of the United States, the Federal Reserve, creates digital dollar credits to buy bonds. If you buy bonds to depress interest rates and to inject money into the financial system, you get higher asset prices. Stocks. Bonds. Real Estate.

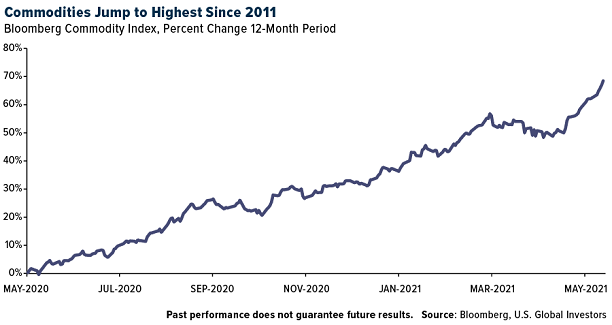

Of course, the Fed does not merely print dollars to push up asset prices or stabilize the financial system. The central bank also endeavors to finance the government’s deficit spending. When deficit spending becomes excessive, you see soaring consumer price inflation and skyrocketing producer price inflation.

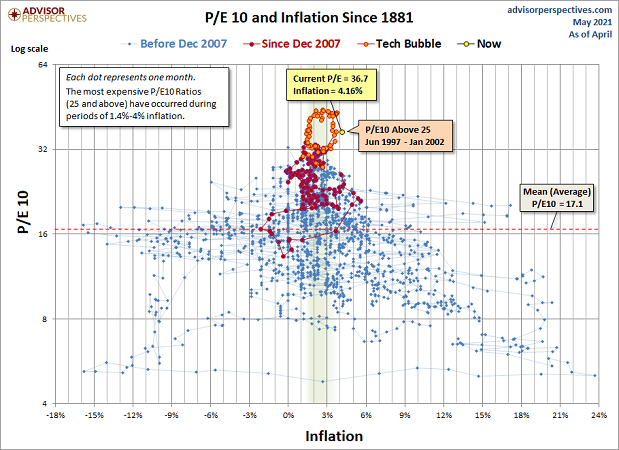

Simply put, stuff costs a boatload more. (And that includes the price of boats.)

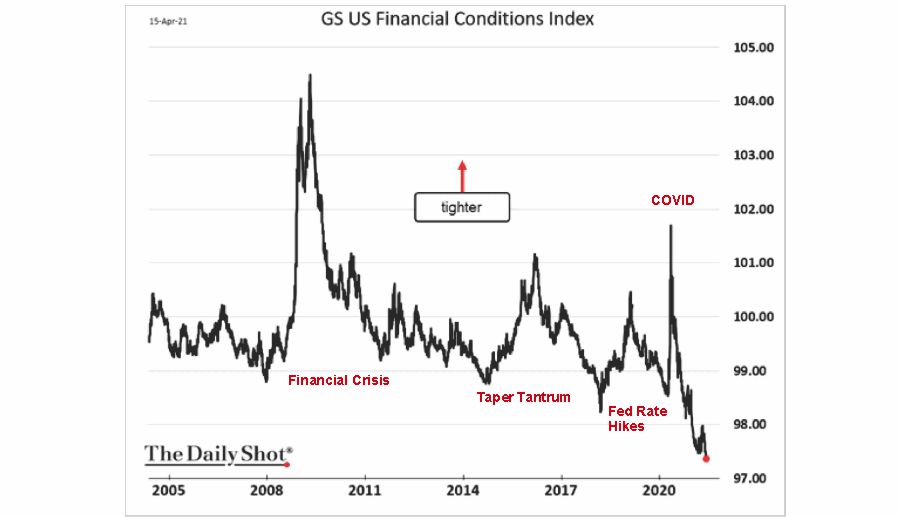

The fact that materials, wholesale products, and services cost so much more could be very troubling going forward. After all, the primary way to fight the erosion of purchasing power (a.k.a. “inflation”) is with tighter financial conditions. That means less money printing by the Fed. It also implies higher interest rates.

Naturally, tighter financial conditions hurt bonds. It happened when the Fed hiked rates in 2018. Bonds also faltered in 2015 when investors feared the tapering of the Federal Reserve’s bond purchasing program.

In a similar vein, Fed rate hiking campaigns precede significant stock sell-offs. Fed tightening that led into 2000 eventually burst the tech stock bubble. What’s more, the rate increases (2003-2007) that preceded the housing bubble resulted in the real estate collapse and a financial crisis in 2008. Even the rate hiking that occurred from 2017-2018 led to the -20% bearish decline in the fourth quarter of 2018.

It is worth noting that the Federal Reserve may not even need to signal an intent to tighten. Financial conditions may tighten anyway if there is a crisis of confidence in the bond community and/or across the lender landscape.

In other words, if higher rates are coming, it’s not just bond investors who might sing the blues. Stock investors could suffer the way that they did in 2000, 2008, 2018 and/or 2020.

Right now, for example, short interest in the most prominent corporate bond ETF (LQD) has never been higher. And if those folks are right about higher corporate borrowing costs/yields, stocks could tumble.

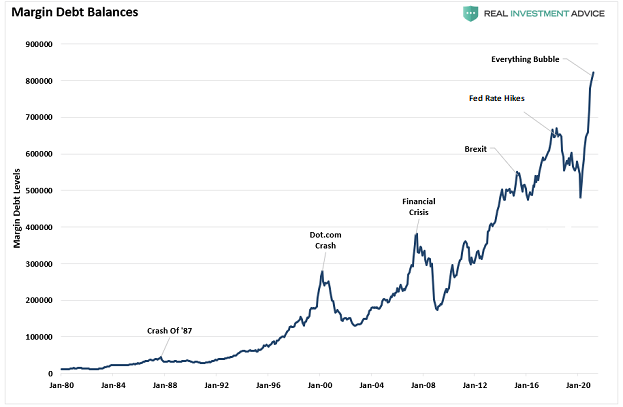

Worse yet, a vicious stock bear can become self-reinforcing. For instance, there is more leveraged, debt-infused, long stock exposure today than ever before. Borrowing money to buy stocks in good times helps to push prices even higher.

On the flip side, when selling activity becomes pronounced, brokerages force margin account holders to increase their cash levels. Those “margin debt calls” lead to forced selling of everything and anything. Even the best stock assets get tossed out the window during a mad scramble to raise cash.

With inflation running hot, with market valuations double the historical norm, with circumstances emulating aspects of the turn-of-the-century stock bubble (2000), what could possibly go wrong?

Would you like to receive our weekly newsletter on the stock bubble? Click here.