Most folks understand it now. The “Everything Bubble” burst.

Like the dot-com balloon in 2000. Like the housing froth in 2008. Over-hyped assets eventually plummet.

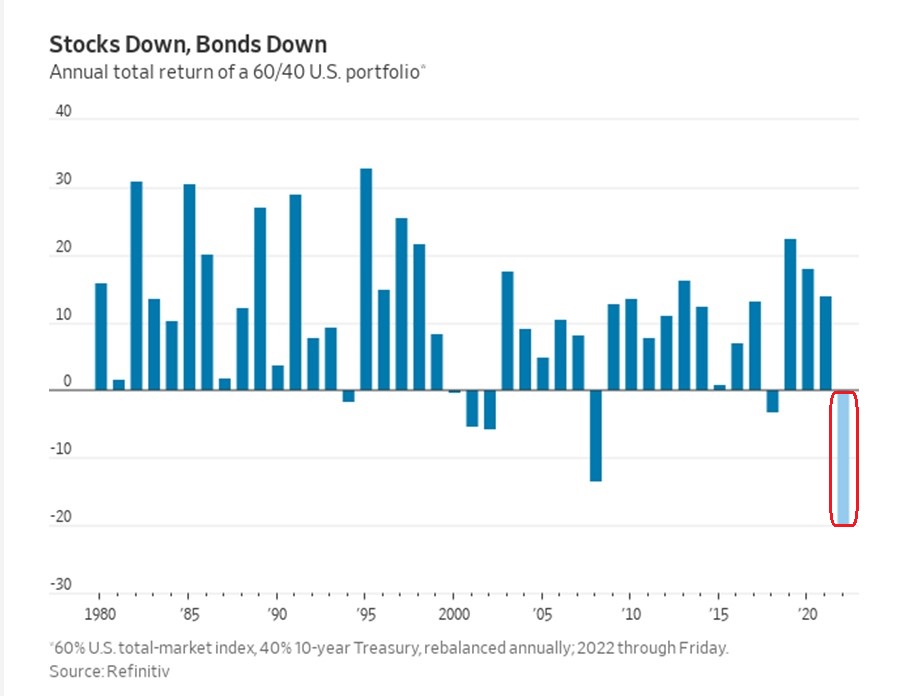

In the first nine months of 2022, bonds and stocks have simultaneously succumbed to dramatically higher borrowing costs. The losses on the ever-popular 60/40 mix have never been worse.

The pain is even uglier under the surface. Whereas popular index funds may be down anywhere from 25%-33%, the average stock within those benchmarks has given up 33%-47%.

Now that is ugly.

So when will the market turn back around? How much further will things fall? Nobody has a crystal ball.

On the flip side, one can identify the circumstances that would make risk assets like stocks appealing again.

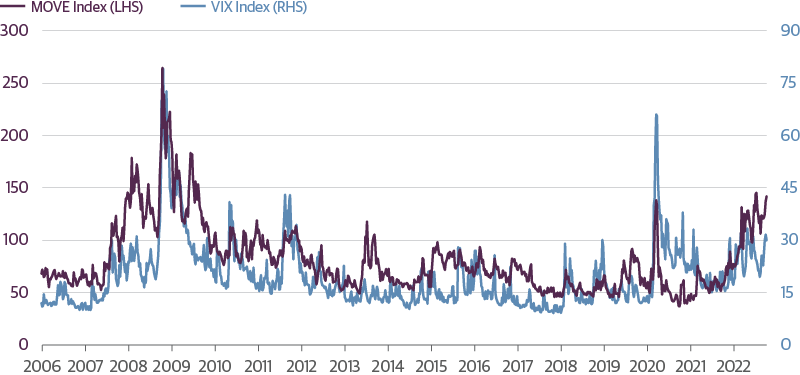

1. Volatility Must Spike. As bad as things are, stock volatility (VIX) remains relatively subdued… all things considered. For the Federal Reserve to stop tightening, as well as consider providing stimulus, the VIX needs to spike the way it did in 2008, 2011, and 2020. (See the light blue line below.)

Other than the 2008 financial crisis, bonds have never been this volatile. But they too may need to spike before the Fed blinks. (See the purple line below.)

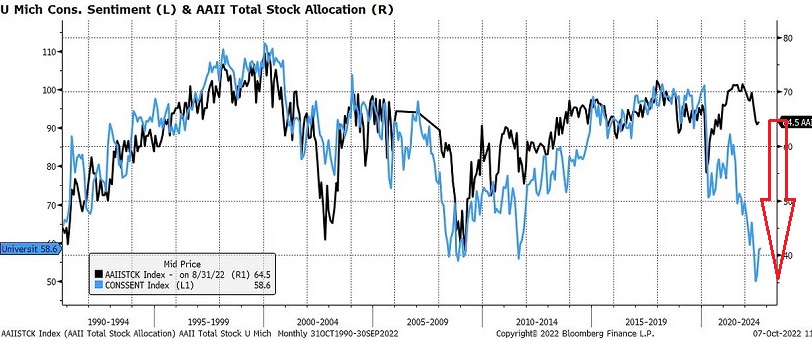

2. Stock Allocations Must “Catch Down” to Sentiment. Scores of analysts have been hanging their collective hats on the notion that stock sentiment is so bad, asset prices must move higher. Yes and no.

Yes, there can be relief rallies as well as short squeezes that send stocks rocketing off 52-week lows and two-year lows. This happens in bear markets.

However, for rallies to become bona fide bull market bonanzas, the bulk of the investment community needs to give up hope. Quit. Capitulate.

Granted, stock sentiment has rarely been this awful. Nevertheless, the investment community is still clinging to more than 60% in stocks. Capitulation is often achieved when that 60% falls to 40%.

3. The Trend Must Change. Presently, the monthly closing price of the S&P 500 is well below its long-term moving average. It has closed below its moving average for seven months in 2022. (See the red dots in the chart.)

In a similar vein, the blue trendline is definitively sloping downward. (See the blue trendline’s direction.)

While many had hoped that the current downtrend would emulate 2018 and/or 2020, the current circumstances appear to share more in common with prior bear markets (e.g., 2000-2002, 2008-09, etc.). Those stock bears were far more brutal than what 2022 investors have experienced.

Regardless, the monthly closing price of the S&P 500 would need to close above its long-term trendline. And the slope of the blue trendline will need to turn upward. Until then, stocks will be under pressure.

Would you like to receive our weekly newsletter on the stock bubble? Click here.