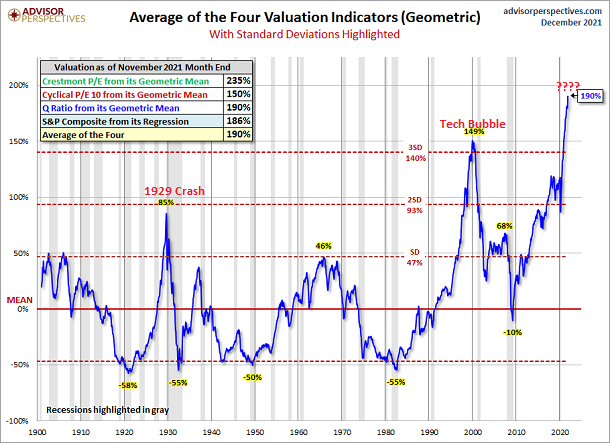

At the start of 2022, the stock market had been sitting atop its highest valuation extremes ever. In fact, our modern-day circumstance rivaled 1929’s super-bubble as well the dot-com hysteria in 2000.

By June of this year, the S&P 500 had descended as much as 26% from its all-time high. And, at present, the market is down approximately 15.5% from a record peak.

So is the worst behind us? Unlikely.

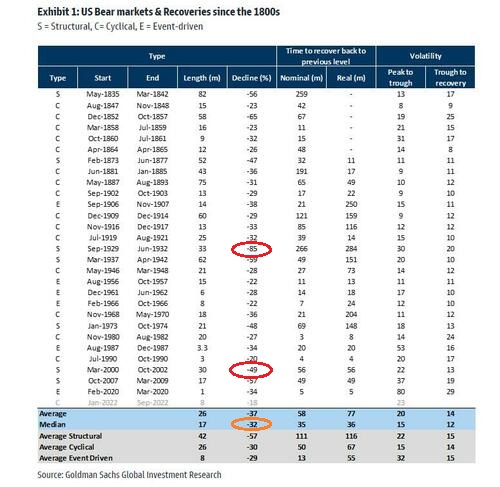

The median bear market across close to 200 years of data is -32%. Yet declines from stock bubble peaks tend to be far more ferocious.

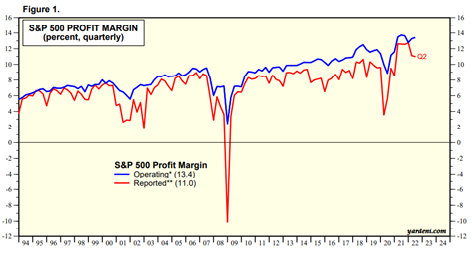

In a similar vein, the economics of dramatically higher borrowing costs do not favor corporate profit margins accelerating. Indeed, margins will decelerate over the coming quarters, as companies deal with higher interest payments and higher input expenses (e.g., labor, materials, etc.).

Said differently, the earnings (E) in price-to-earnings (P/E) ratios will move lower. If the E moves lower and stock prices (P) stay the same or rise, stocks will remain egregiously overpriced.

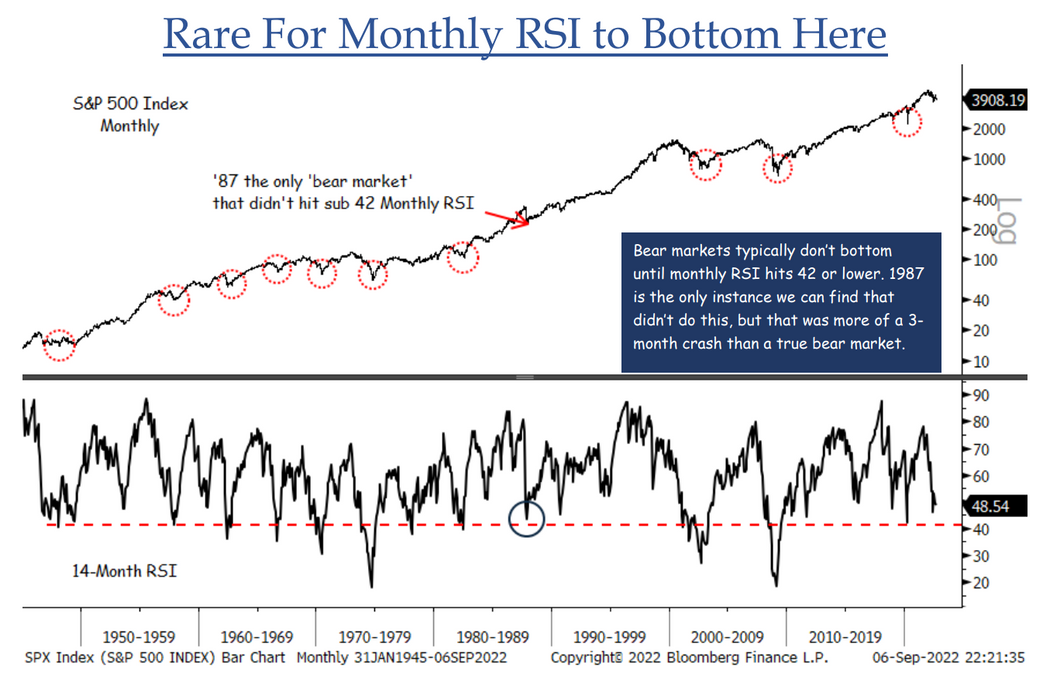

There are other problems with the idea that the worst is in the rear-view mirror. For example, the monthly Relative Strength Index (RSI) has not yet seen the low 40s — an area that is consistent with investor capitulation.

Additionally, the monthly close for the S&P 500 has yet to finish above its long-term trendline. Until it does, the stock bear will persist.

What we have seen since the 2022 lows is most consistent with a bear rally. Investors buy the sharp sell-off in anticipation of the worst being over.

Unfortunately, corporate fundamentals are deteriorating and market technicals are still ‘breaking bad.’ What that implies is that stocks are almost certain to head for new lows.

The good news? Genuine opportunity always emerges from the ashes. You just do not want to leap into a forest fire that is only 50% contained.

Would you like to receive our weekly newsletter on the stock bubble? Click here.