A few weeks ago, most pundits in the financial media had declared that the bear market was over. If nothing else, they insisted, we had already seen the bearish lows.

They were wrong about the bear market being over. And they are almost certain to be wrong about the June lows holding up.

Perhaps ironically, they have been blaming their ill-conceived prognostications on the Federal Reserve. The Fed, they say, is too aggressive with raising rates. Never mind the fact that the same commentators based their predictions of bull market nirvana on a notion that inflation is/was peaking, whereby the Fed could pivot back to cutting rates and printing money to stimulate the economy.

Now? The consensus in the financial media are coming around to my long-standing views. The Fed will look to vanquish inflation with higher borrowing costs and less dollars in the financial system… “until something breaks.”

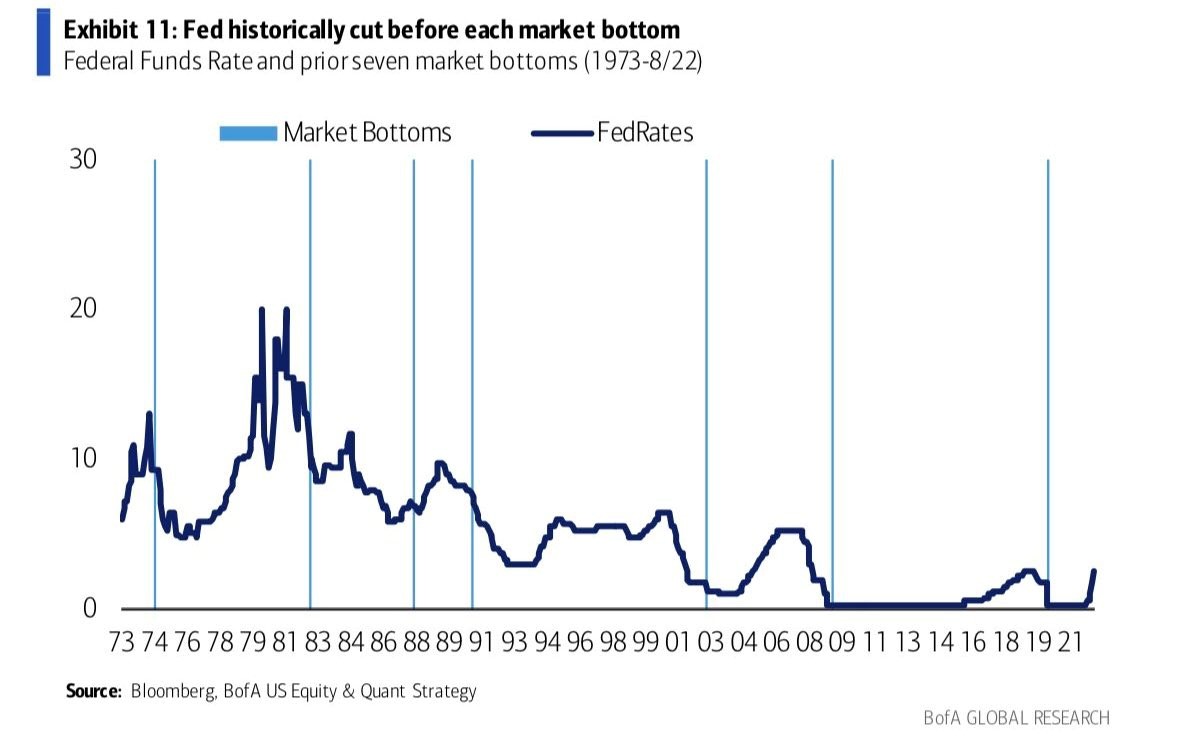

There is extraordinary precedent for the idea that something will need to break for the Fed to cut and run. Most notably, stock market bottoms have never occurred without the central bank starting to cut rates. And something typically needs to go awry before the Fed comes to the rescue.

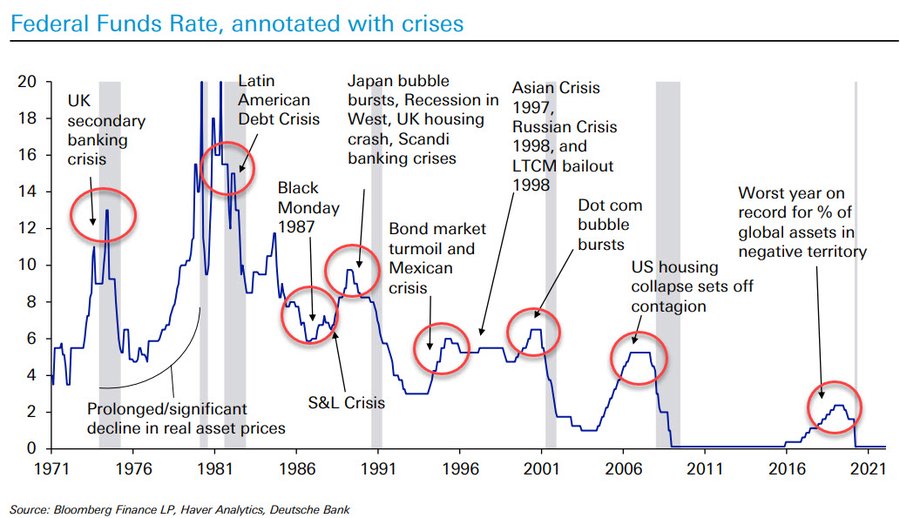

Not only is it worth noting that rate cuts were necessary precursors for every stock market bottom, but one can line up the crises that precipitated Fed action. Take note of the reality that some of the things that “broke” occurred outside of the U.S.

Once again, then, Fed rate cuts have preceded every market bottom. And yet, the mainstream financial media continues to insist that the market already bottomed back in June.

If something needs to break before the Fed starts slashing rates, and if the rate cutting action is necessary before the bear bottoms out, what will fracture? And when will it happen?

Real estate is one possibility. While the residential property market is not suffering from bad lending standards and systemic bank failure, it is struggling mightily. Mortgage rates are twice what they were two years ago, with property prices 40% higher than they were two years ago. Few who wish to buy can afford to do so.

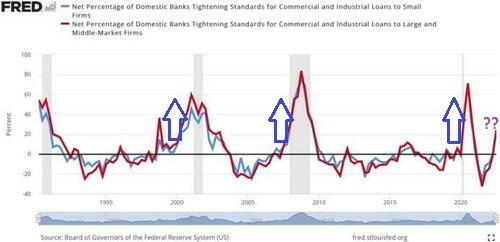

And for those who might still qualify, banks are getting stingier about lending. The last three times that lenders tightened their standards at a pace like today, a recession was close at hand.

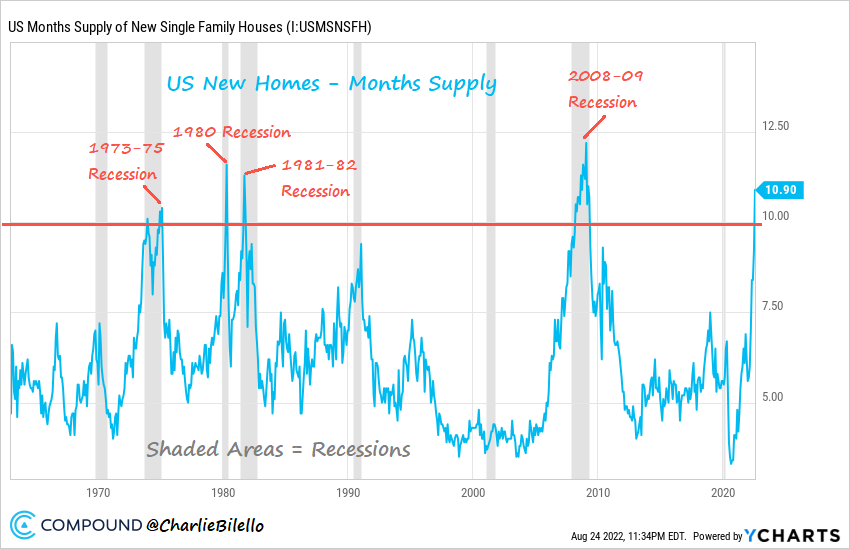

Speaking of economic hardship, each time in the past that new home inventories exceeded 10 months of supply, the U.S. economy was already in a recession. Each time.

The reality that our Fed is tightening straight into a recession is troublesome. Even if real estate can hold serve, something else will fall apart. Recessions themselves have a way of pulling back the sheets on what is broken, and the Fed is unlikely to see it in time to keep stocks from plummeting to fresh bear market depths.

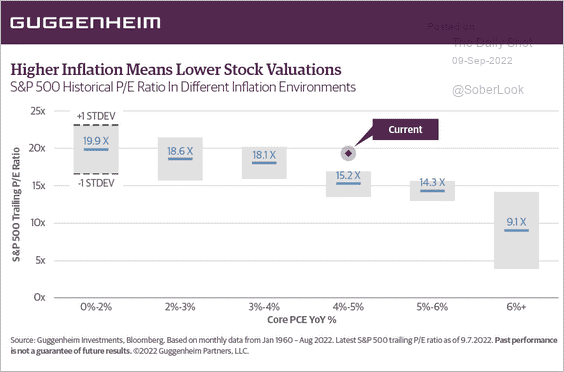

Even from a valuation standpoint, stocks have only given up about half of what is necessary to return to fair value. For instance, fair value for the S&P 500 based on historical P/E in different inflation environments might be in the 3100-3250 range. That might represent a top-to-bottom bear of roughly -33%.

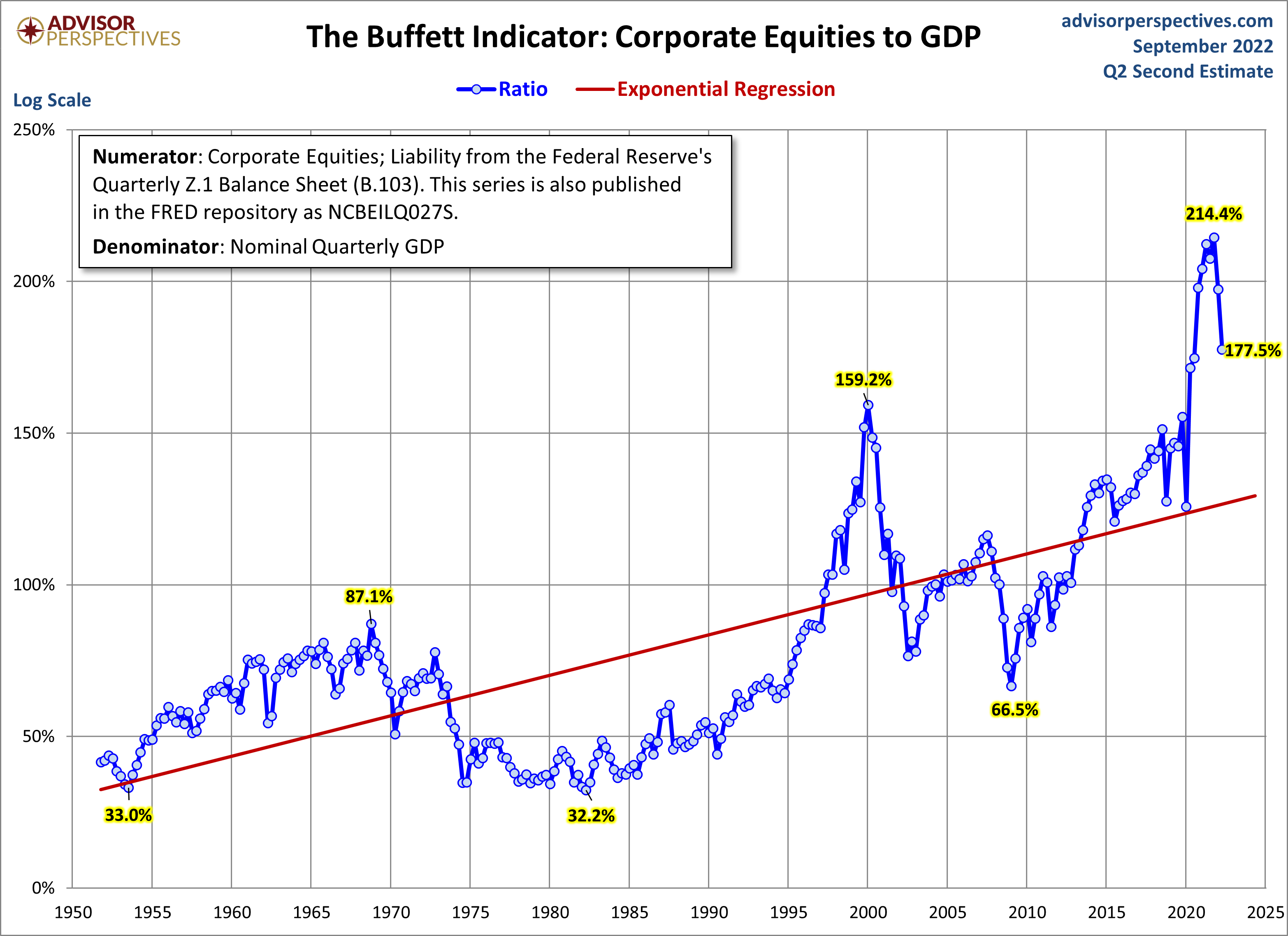

Some indicators are a little less rosy. Warren Buffett’s favorite valuation indicator, market capitalization-to-GDP recently clocked in at 177.5% above its norm. Getting back to its regression line – reverting to the mean – might require the S&P 500 to fall as low as the 2300-2400 level. That would represent a top-to-bottom descent of -50%.

Will stocks get slammed that badly? Probably not. The Fed is unlikely to sit by passively if the stock market shows signs of repeating the 50% price eviscerations that occurred in the 2000-2002 collapse or the 2008-2009 disaster.

On the flip side, the Fed will not cut its overnight lending rate or end the reduction of its balance sheet (a.k.a. “quantitate tightening” or “QT”) until something shatters. One should not anticipate a stock market bottom before the S&P 500 falls below a 30% mark (3350). And it may, in fact, drop considerably lower.

Would you like to receive our weekly newsletter on the stock bubble? Click here.