The Federal Reserve explains away rising costs across commodities, shipping, food, retail and rent as “transitory.” They might be right.

On the flip side, the stock bubble is ignoring inflation-adjusted data as it relates to valuation. Specifically, in the three previous instances when real earnings yields (E/P) fell below 0%, stocks eventually collapsed.

Granted, the crash in October of 1987 was relatively short-lived; the same is true for the way that the March of 2020 crash reversed itself. Nevertheless, 2021’s similarity with the late 1990’s tech wreck and the 2008 financial crisis is ominous.

There are those who attempt to dismiss the present circumstances. They take comfort in the fact that asset price inflation — rising prices for stocks, bonds, real estate, collectibles — has been making families wealthier.

Asset price inflation might be a good thing for the wealthier among us. Wealthier folks own most of the assets. Yet it may turn out to be less than a blessing should asset prices plummet.

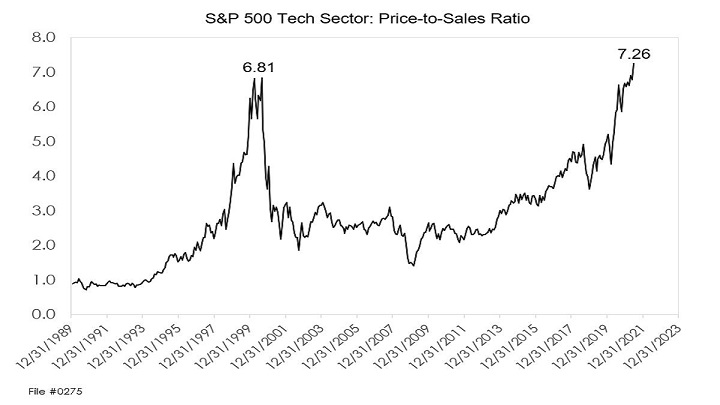

Indeed, stocks are not “fairly valued.” They are insanely overpriced. Even the tech sector is beginning to look frothier than it did in 1999-2000.

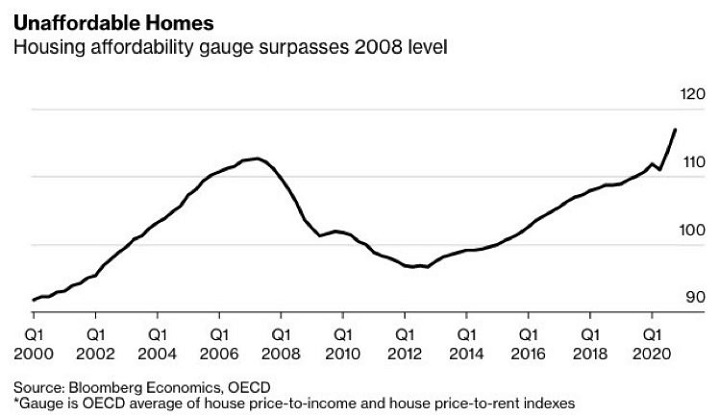

Equally concerning, stocks are not the only asset class with questionable valuations. Home prices relative to household income and prices relative to rent have never been higher. Not even during the mid-2000s housing bubble.

Keep in mind, the chart below is not a gauge of prices by themselves. This is price as it relates to income; price as it relates to rent. In other words, homes are decidedly unaffordable despite drastically lower interest rates.

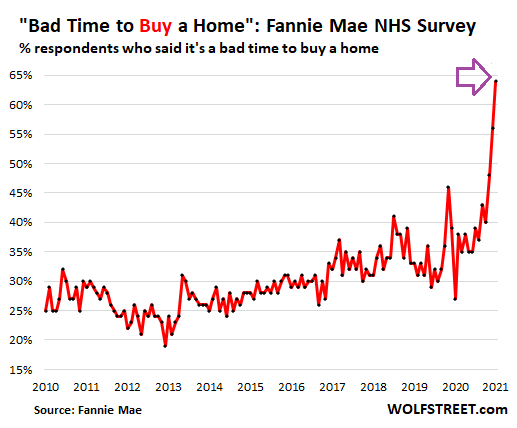

Consumers are starting to become discouraged. The percentage of folks who currently say it is a “bad time to buy a home” hit an eye-popping record of 64%. What’s more, the primary reason for the sentiment is stratospheric home prices.

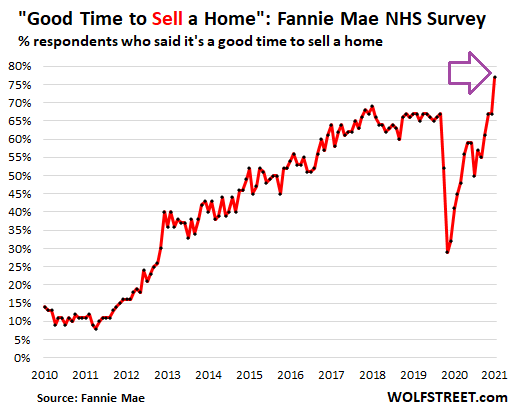

In contrast, those who indicated that it was a “good time to sell a residence” pole vaulted to 77%. What happens if these surveys play out over the coming months/years? If motivated sellers overwhelm tepid buyer demand, home prices could drop precipitously.

Stock enthusiasts might counter that there are a fixed number of stock shares in supply. And with the Federal Reserve backstopping assets to preserve the wealth effect, buyers and holders cannot lose.

However, the notion that the Fed is all-powerful and that faith in its policies will never be challenged is flawed. Another flaw? The idea that stock shares in existence do not expand.

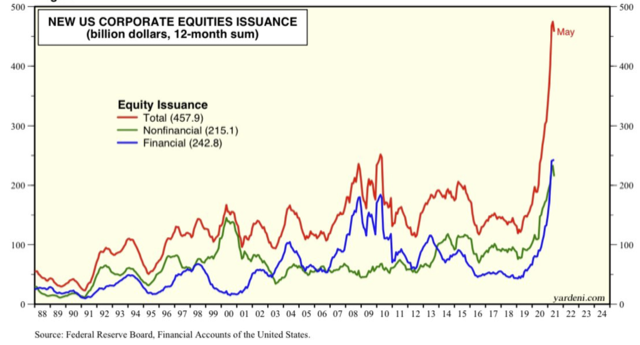

Scores of public corporations are tripping over themselves to issue more shares. Meanwhile, the supply of shares coming to market via traditional IPO or backdoor Special Purpose Acquisition Companies (SPACs) is more vibrant than at any point in recorded history.

Is there an easy answer for managing the risk of participation in the 2021 stock bubble? No, there is not.

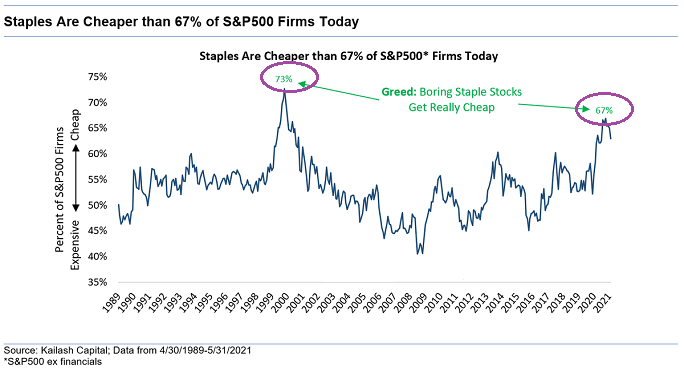

That said, the consumer staples sector may provide a bit of shelter. Many of the biggest companies in the segment would be capable of passing along inflationary pressures to consumers without much of a hit to the bottom line.

More noteworthy? Staples are less bubbly on a relative basis than the rest of the S&P 500.

Would you like to receive our weekly newsletter on the stock bubble? Click here.