The current price-to-sales (P/S) ratio for the S&P 500 is 2.4. That is higher than it was at the peak of the 2000 stock bubble.

I decided to screen large-cap U.S. companies for outrageous P/S valuations — those that jumped the 15x revenue barrier. According to Morningstar, 63 U.S. public corporations have surpassed P/S ratios of 15.0.

Ironically, many of the offenders are darlings on Wall Street. Nearly all of them are on Jim Cramer’s “Buy, Buy, Buy” list.

Tesla, Zoom, Crowdstrike. Hey, it’s the future!

Adobe, Cloudfare, Snowflake. No price is too high for a piece of the future, right?

Some folks might disagree. Scott McNeely, former CEO of Sun Microsystems, comes to mind.

One of the hottest stocks during the late 1990’s market euphoria had been Sun Microsystems. A few years after the bubble burst, Mr. McNeely discussed the lunacy of its P/S valuation of 10 in the year 2000.

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

If a P/S ratio of 10 was insane back then, what might one conclude about P/S ratios greater than 15 today?

The only conclusion for buyers of these companies at these prices is that price no longer matters. What does? Too much Federal Reserve money in the system chasing too few available shares of “game-changing” technologies.

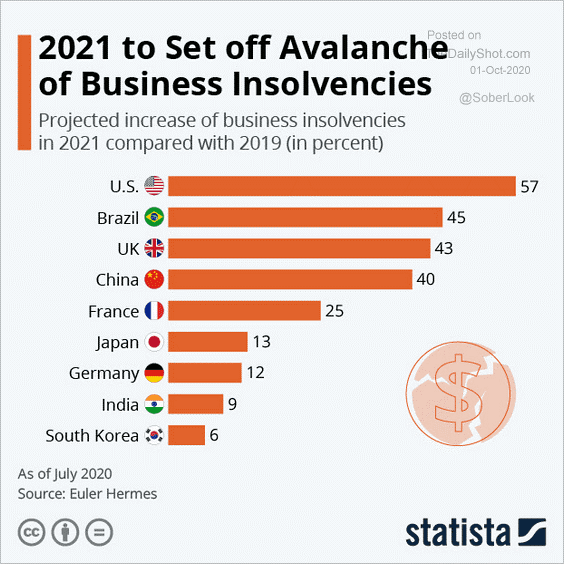

After all, a projection of a 57% increase in business insolvencies isn’t shaking confidence.

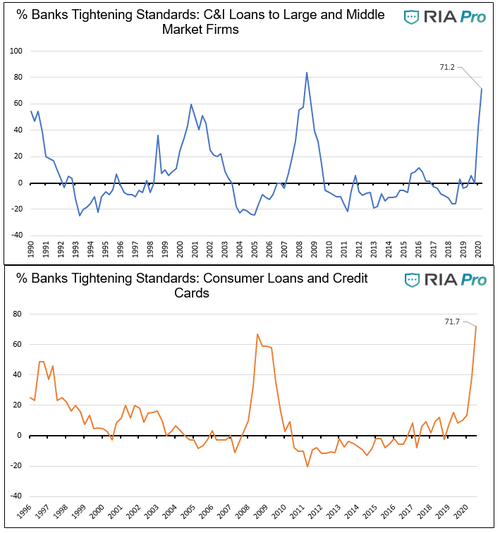

The tightening of credit for small businesses and consumers does not seem to rattle any cages.

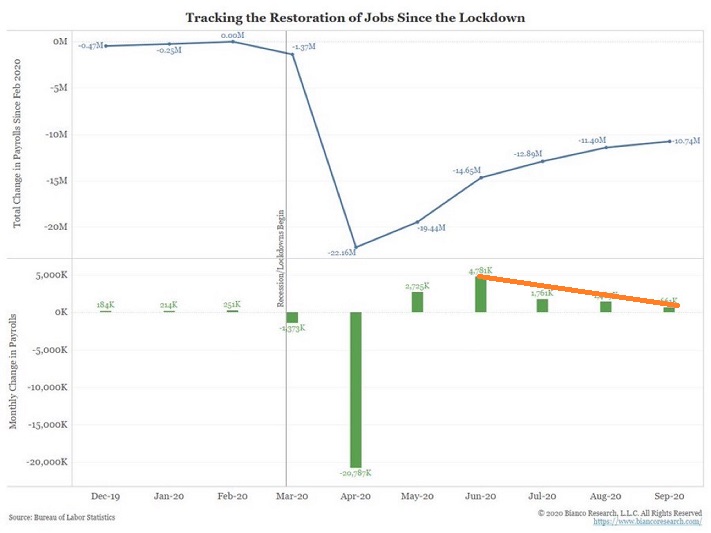

The loss of momentum in employment data does not seem to bother investors either. (See the orange line.)

Apparently, the bulk of market participants believe that the sun will come out tomorrow. And they’re betting their bottom dollars on brighter days ahead, from vaccines to economic well-being to government stimulus.

On the other hand, when this decade’s stock bubble bursts, people will look back the way that CEO McNeely of Sun Microsystems looked back. And they’ll ask, “What were you thinking?”

Would you like to receive our weekly newsletter on the stock bubble? Click here.