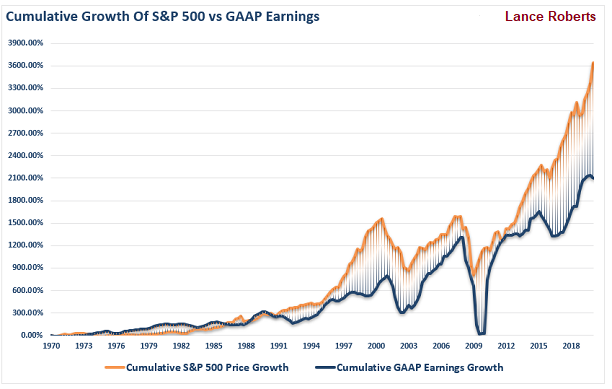

Corporations should use generally accepted principles (GAAP) when reporting their earnings. Instead, they prefer to discuss “non-GAAP” earnings to make profits look better than they are.

So what happens when you strip away the chicanery of non-GAAP to look at GAAP? According to Lance Roberts, the S&P 500’s price growth is even more disconnected from GAAP earnings growth than what investors witnessed at the peak of the 2000 stock bubble.