There are times when one ought to look beneath the covers.

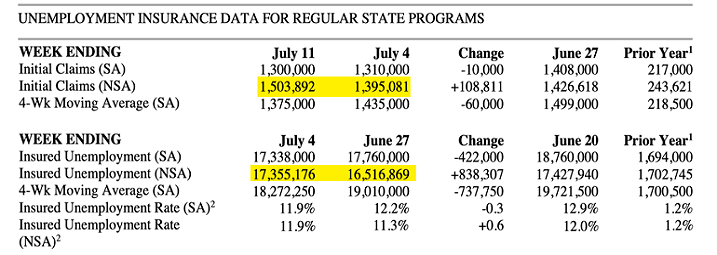

For example, if you merely scroll the headlines (7/16/20), you’d read that initial jobless claims fell to a post-pandemic low of 1.3 million. Never mind the persistently high claims above one million. Things are getting better, right?

Not so fast. The Labor Department “seasonally adjusts” the figures. Unadjusted data show that initial and continuing claims are on the rise.

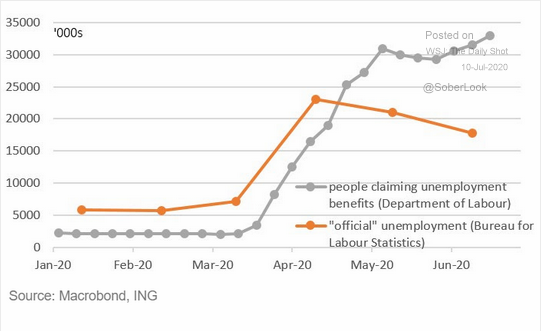

There have been similar discrepancies when it comes to other aspects of unemployment. For instance, a whopping 23% of the US civilian workforce collects unemployment payments. These folks are not working, nor are they retired.

Yet, somehow, the official government stat for the U.S. unemployment rate is a tick higher than 11%. What gives?

Due to the pandemic, the U.S. government relaxed its rules for collecting unemployment. So, while the Department of Labor has seen a record number of unemployment claims near 35 million, the Bureau of Labor Statistics (BLS) is only counting certain classifications. The BLS’s figure, then? Just 17.35 million.

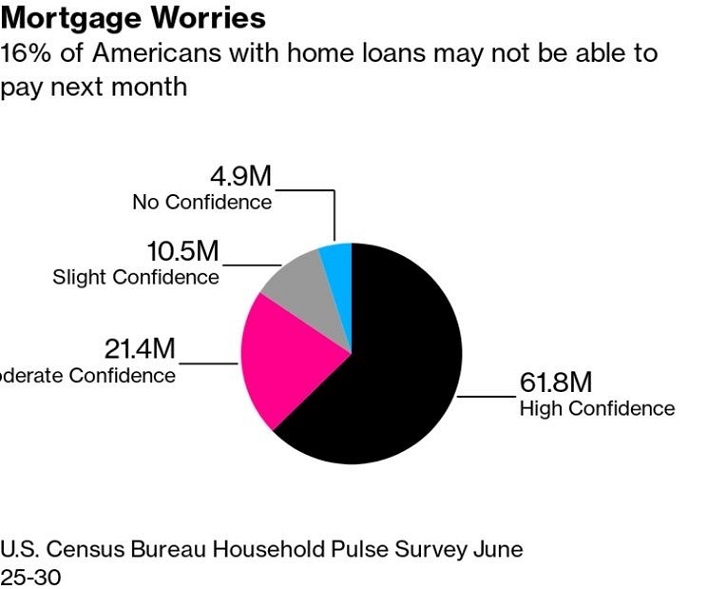

The problem with ignoring economic reality is that it can come back to bite investors in the backside. For instance, if 16% of Americans do not believe that they will be able to pay their mortgages in July, how can these consumers spend on the products and services of public corporations?

(They can’t. And that makes it difficult, if not impossible, for those corporations to grow their earnings per stock share.)

Consumer weakness. The probability of longer-lasting unemployment. Rising corporate bankruptcies. State shutdowns. Potential for higher corporate taxes. Nothing matters… until it suddenly does.

So, is the entire stock market as strong as people believe? S&P 500 ex “mega cap growth” is down roughly 15% on the year. The 10 mega-cap growth stocks? They have collectively gained more than 30% in 2020.

That is correct. 10 stocks have pulled an entire index up from significant losses of -15% to 0%. So much for diversification.

These 10 names primarily represent a love affair with “New Economy” technology. However, extraordinary overvaluation in the select few can reverse course, dragging down the price of the large-cap benchmarks dramatically.

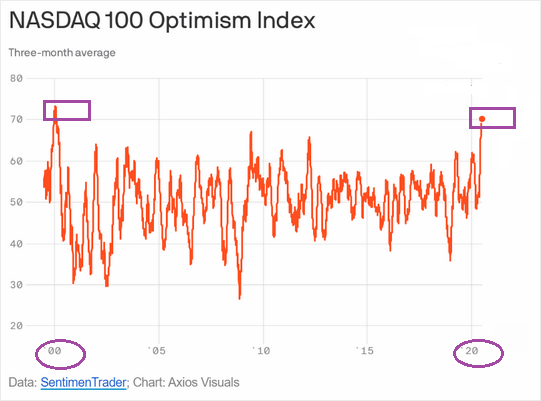

Consider what transpired at the turn of the century. A misplaced belief in all things tech eventually led to -80% top-to-bottom declines for the Nasdaq 100 (QQQ). Perhaps ironically, 2020 investors are nearly as optimistic about the Nasdaq 100 today as they were in 2000.

In contrast, investors have not wanted anything to do with bank stocks. Banks rely on their ability to charge borrowers more interest than they pay depositors. At the moment, though, rock-bottom interest rates and anemic loan growth have been eviscerating profit margins.

At least when it comes to the banks, profits matter. The KBW Bank Index is still down -35% through mid-July.

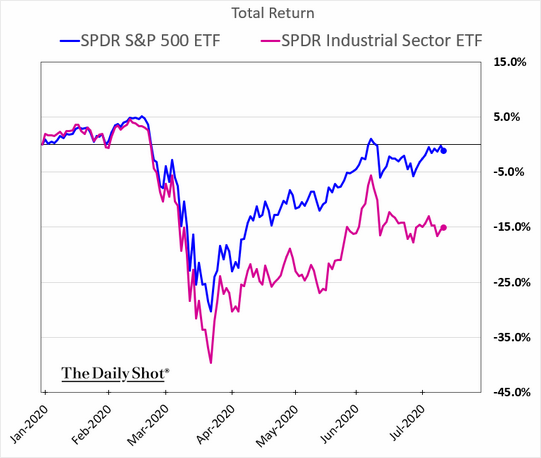

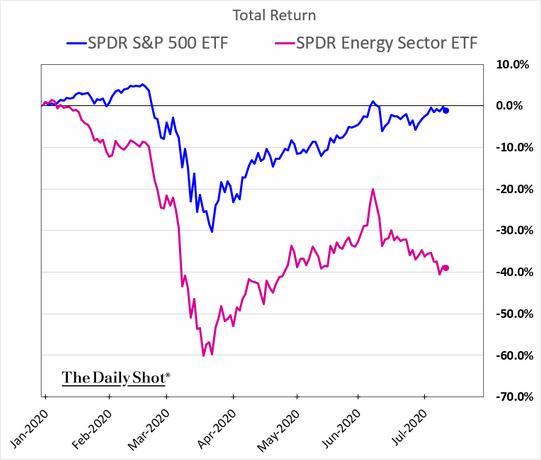

Can the stock market continue to thrive without the banks? What about “old economy” stalwarts like industrials and energy?

It is a story as old as time. The “haves” and the “have nots.”

What happens next? Either the prosperity of the 10 mega-cap growth standouts will spread to the other 490, or economic gravity will fill the mega-cap stock balloon with lead.

Mega-cap stocks certainly belong in investor portfolios. Nevertheless, you can mitigate over-allocating to “the market” with less risky propositions.

For example, the preferred shares of data center real estate investment trusts (REITs) offer stable yields above 6%. Digital Realty’s 6.350% Series I Cumulative Redeemable Preferred (DLR.PRI) trading at $25.30 implies a 6.27% yield. The risk of your investment being called is only 1.24%.

One might also want to look at financial sector survivors outside of the traditional banking segment. Take a look at the preferred shares of the global investment leader and private equity king, KKR. Its 6.75% Series A Preferred Units (KKR.PR) trading at $26.02 are yielding nearly 6.5%. Although the call date is not until next year (6/15/2021), the 4% premium to $25.00 liquidation is about as much call risk as one might wish to take.

Would you like to receive our weekly newsletter on the stock bubble? Click here.