Institutions — mutual funds, pensions, insurance companies, corporations, sovereign wealth funds — often represent smarter money. Indeed, stock prices tend to rise when institutional buying is robust.

However, history has been less kind to mom-n-pop investors (a.k.a. “retail”). In the past, when average individuals became irrationally enamored with stocks, a market meltdown was not far behind.

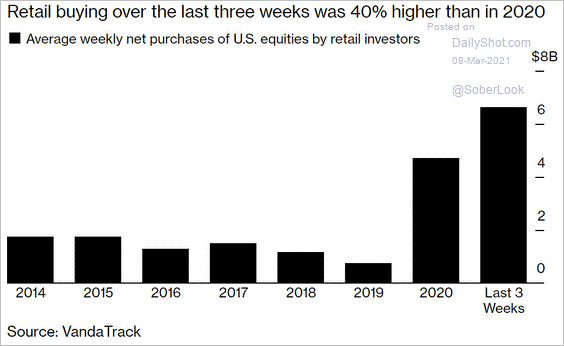

Here in 2021, retail trading activity is way up. For instance, the average daily volume for the largest e-brokers hit 6.6. million shares in December. That was a record. Yet average daily trading increased to 8.1 million shares by January, notching a 23% increase.

Is the jaw-dropping amount of trading activity split between sellers and buyers? Hardly. Net buying has launched into orbit, helping to keep stock prices near an all-time high.

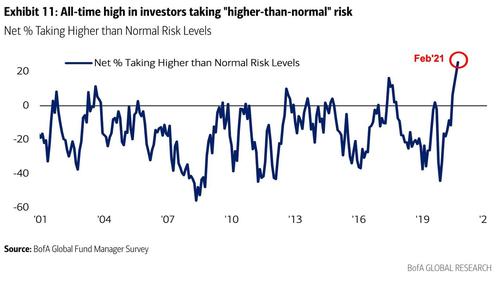

There’s more. The percentage of folks who are taking more risk than they might otherwise take has also hit an extreme.

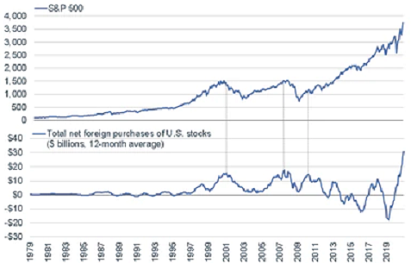

Retail investors are not the only participants looking to “win big.” Net foreign buying has witnessed a remarkable surge.

Spikes in foreign purchases of U.S. stocks may be a warning sign, though. Recent spikes preceded prominent 50% bear market losses in the dot-com collapse (3/00-9/02) and the financial crisis (10/07-3/09).

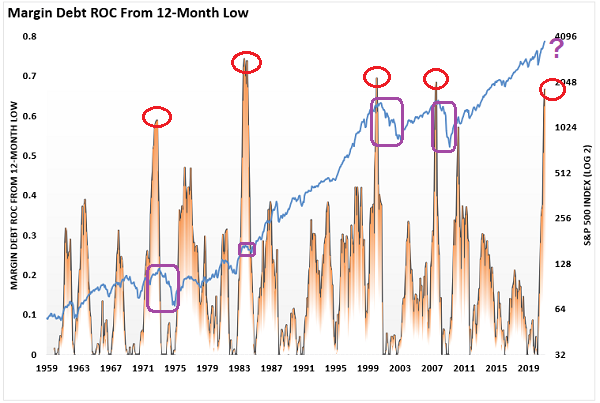

Perhaps there would be less cause for concern were it not for the boom in leverage. Specifically, investors are borrowing money and using their stock shares as collateral to buy even more.

Today’s upswing in margin debt? It is eerily similar to what occurred prior to the 50% losses during the 1973-1974 bear market and the aforementioned disasters this century.

Bottom line? Consider how and when to rebalance.

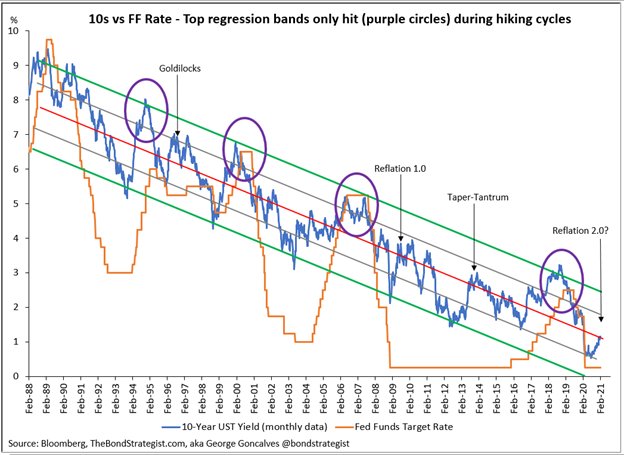

For example, bonds have had a terrible time over the last three months. And the financial media continue to fret rising rates. On the other hand, yields are unlikely to climb meaningfully from their current levels unless the Federal Reserve begins raising the Fed Funds rate (FFR).

Does anyone honestly believe the Fed is gearing up for a rate-hike campaign? Not bloody likely. The Fed is far more likely to start buying longer maturity bonds via yield curve control.

As difficult as it may be to believe, then, you may want to rebalance your portfolio. That might involve selling some stock and buying some bonds.

Would you like to receive our weekly newsletter on the stock bubble? Click here.