In late August of 2000, the median stock in the S&P 500 hit its highest Forward P/E level ever. A 12-month Forward P/E of 26.

For the better part of the last two decades, investment gurus routinely rebuked the foolishness of paying 26 times estimates of corporate earnings 12 months out. The notion became emblematic of stock bubble lunacy.

Nevertheless, here in late August of 2020, stock bubble madness is back with a vengeance. Investors have pushed prices up to the point where Forward P/Es for the median stock in the S&P 500 have once again reached 26.

What does it mean when stock valuations reside at the 100th percentile of historical levels? It means that the average (median) stock has never been more expensive.

Meanwhile, some things defy every imaginable aspect of logic. The mania for Apple (AAPL) shares fits the bill.

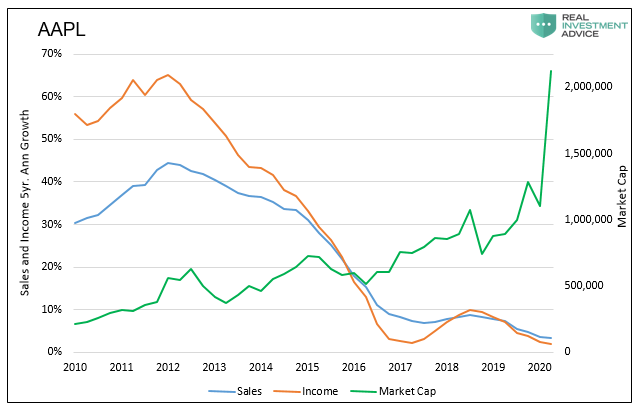

According to Michael Lebowitz, sales at Apple over the prior five years have grown at a meager 3.2%. Equally unimpressive? Income has only grown at 1.8%.

Granted, Apple makes wonderful products and provides wonderful services. Yet it is not growing like gangbusters to justify a price-to-book (P/B) of 29.4, a price-to-cash flow (P/CF) of 30.2 or a Current P/E of 37.8.

The above-mentioned valuations are more than double their long-term 10-year averages. In fact, share prices would need to fall 50% just for the stock to approximate Apple’s (AAPL) longer-term metrics.

A 50% haircut to restore sanity? That’s right. And it would have to fall a whole lot further to get those shares on the cheap!

Would you like to receive our weekly newsletter on the stock bubble? Click here.