Late in 2005, my wife and I cashed in our two properties and decided to rent. We were a year early when we walked away from the real estate bubble that eventually destroyed tens of millions of families nationwide.

Fifteen years ago, the math on ownership failed to add up. We leased a 4-bedroom, 3-bath home in our neighborhood for $2700 per month. Buying that property? In a 20% down scenario? It would have fetched $4,400 in principal and interest alone.

Part of the problem, of course, was that buyers could acquire these properties with 0%-2% down and no documentation of income. Others even managed to secure negative amortization scenarios. And yet, few recognized that this path to riches was filled with potholes.

Perhaps I should not be surprised, then, by the number of people inquiring about Apple and Tesla at these prices. They’re not genuinely after guidance; rather, they would like permission and/or validation for a pre-existing intention to buy.

Who wants to hear facts about the insanity of Tesla’s 1100 Forward P/E or 12 P/S? Besides, most people stopped believing in ‘Old Economy’ valuation metrics.

On the other hand, even the most ardent believer in ‘New Economy’ price gains might want to look at a price chart. After all, in the history of large company stocks, one would struggle to find anything quite like Tesla’s vertical price movement. (And if you do find it, you’re going to see an equally powerful price collapse.)

Where investors go astray is that they get caught up in the greatness of the companies themselves. They will focus solely on how Tesla is revolutionizing the way that people live. Same goes for the first $2 trillion behemoth in Apple.

However, the fact that these innovators are so wonderful does not imply that it is sensible to acquire their shares at any price. A $40 million beachfront estate is not automatically worth $400 million or $4 billion or $4 trillion, simply because there’s no other property quite like it on the shores of Laguna.

Similarly, Germany is the 4th largest economy on the planet. It is home to hundreds of remarkable corporations. Yet Apple is now worth nearly as much as all of Germany’s public companies… combined. How is that for perspective!

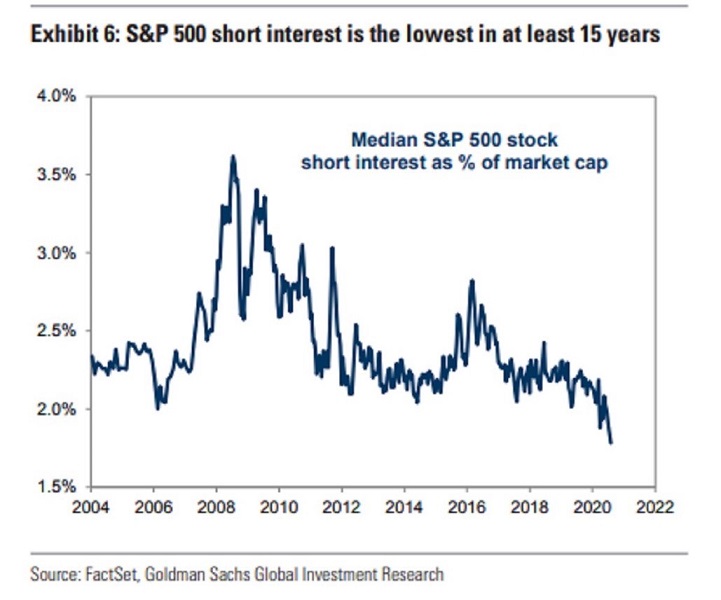

Right now, you may not be able to find many investors willing to short mega-cap growth stocks like Apple. In fact, some are so intimidated by the Federal Reserve’s money printing resolve, short interest is virtually non-existent.

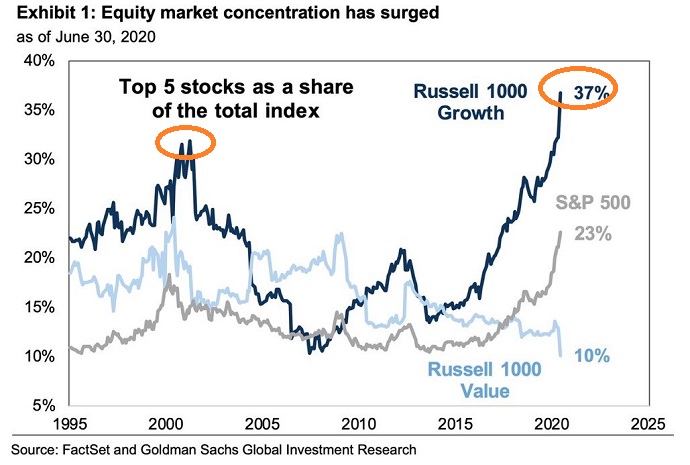

If history is any guide, though, extreme equity market concentration in a handful of growth names will become problematic. And a bursting of the stock bubble will inflict extraordinary pain on the least prepared.

Would you like to receive our weekly newsletter on the stock bubble? Click here.