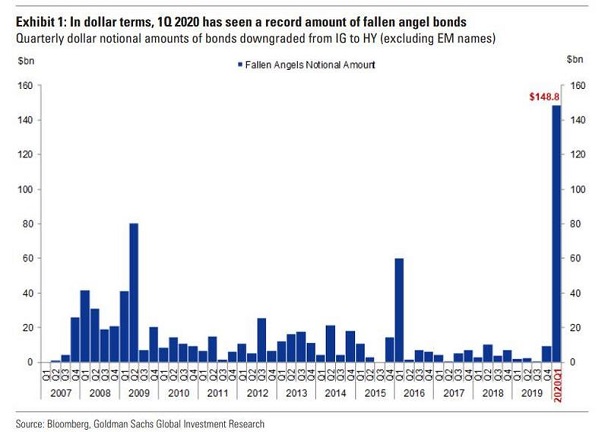

They call ’em, “Fallen Angels.” They’re bonds that the credit agencies demote from investment grade (IG) to high yield (HY).

Unfortunately, there’s nothing angelic about a wave of downgrades happening all at once. And that’s what transpires in recessions.

For example, in the first quarter of 2020 alone, $150 billion in “high quality” IG bonds have been re-rated as HY, or “junk.” Goldman Sachs analysts anticipate $550 billion more in fallen angel activity over the next two quarters, bringing the total to $700 billion.

Putting the tsunami into perspective, 10% of the IG universe must get dumped from pensions, mutual funds and investment grade bond ETFs. And it likely would not stop there.

BBB-rated debt already comprises one-half of the IG marketplace. Triple Bs can be deadly since they are only one notch above a double B junk rating. In other words, estimates on the downgrade wave are likely to be understated.

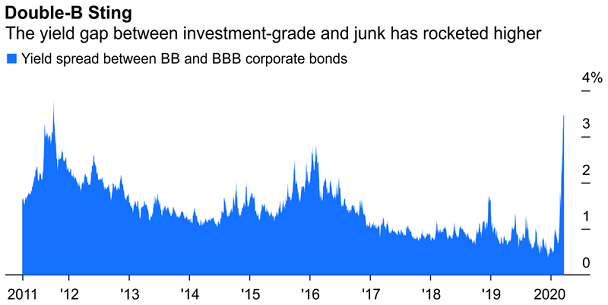

Right now, the yield spread between BB and BBB is north of 300 basis points. Borrowing costs for fallen angel companies are literally skyrocketing. And there’s no telling if they will come back to earth quickly enough for these businesses.

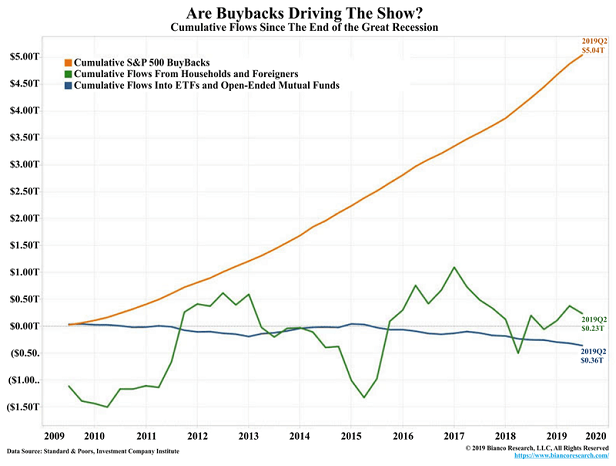

Bondholders are not the only ones who get hurt. Those looking to avoid dreaded downgrades scramble to shore up their balance sheets by slashing dividends, selling assets and ending stock buyback programs. Those receiving downgrades? Higher borrowing costs mean there won’t be money for buybacks or dividends at all.

In sum, stocks tank when companies struggle to service their debt and/or take actions to improve their balance sheets. And in a world where stock buybacks contributed mightily to the 2020 stock bubble, a sharp reduction in those buybacks is going to be painful.

Please click here if you’d like to receive our weekly newsletter.