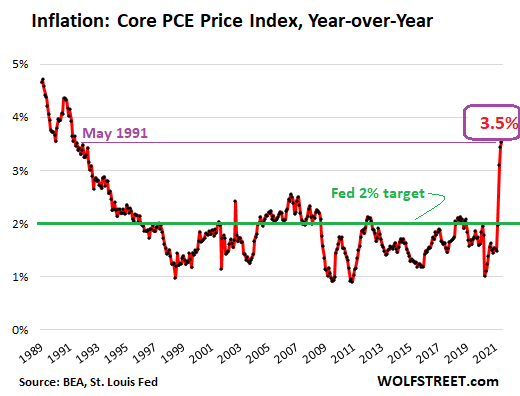

Government leaders choose to ignore rising food and energy costs when discussing inflation data. Yet, consumer staples companies do not ignore rising costs. Nearly all of them — Procter & Gamble, Coca Cola, Kimberly Clark, Tyson, General Mills — are passing along higher costs to consumers.

Even when one excludes food and energy from the picture, prices in other areas of the economy have moved up sharply. Year-over-year, costs have hit three-decade highs.

One way to offset higher prices in everything from utilities to consumer services is to benefit from asset price inflation (e.g., stocks, bonds, real estate). Unfortunately, a large percentage of people in the economy do not own enough assets to offset an ever-rising cost of living.

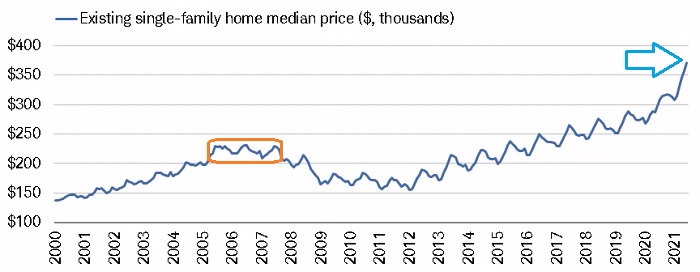

For those of us who do own assets, though, it is impossible to overstate the impact of the “wealth effect.” Real estate has been particularly effervescent.

For perspective, consider the mid-2000’s housing bubble peak. Existing home prices leveled out around $230,000. Today? Median prices have not only hit $360,000, but there is very little evidence of a leveling out period.

As it stands, year-over-year home prices are up 23%. Even with a 30-year mortgage in and around the 3.00% arena, prospective homebuyers may soon determine that the total costs have become untenable.

What about stocks? Do they still make sense for new dollars?

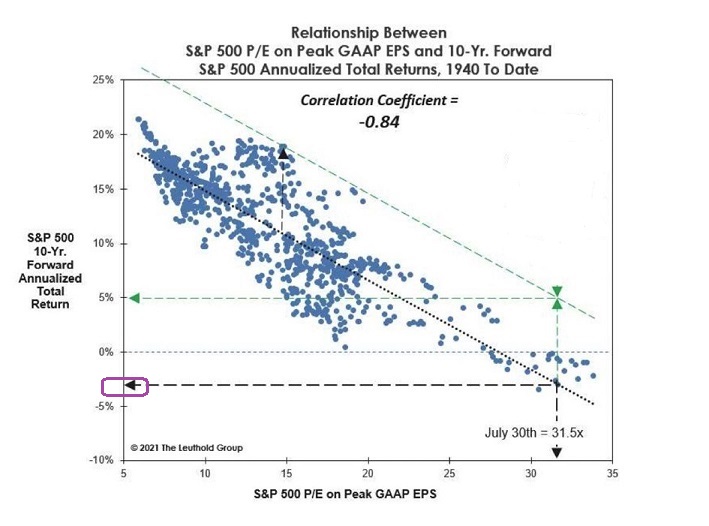

Consider the relationship between Peak Price-to-Earnings (P/E) on the S&P 500 with 10-year forward returns. As of July 30th, forward returns are projected to be roughly -2.5% annualized for the next decade. (See the purple box below.)

Naturally, Peak P/E is not a perfect metric. Its predictive power is roughly 84%. One might even argue that we could see 5% annualized returns across the next decade if the metric experiences its largest ever error in 80 years of data. (See the green arrow above.)

Anyone who finds comfort in the deviation that leads to a 5% annualized projection may wish to recheck his/her premises. Every indicator worthy of note is belching on the hyper-valued stock bubble.

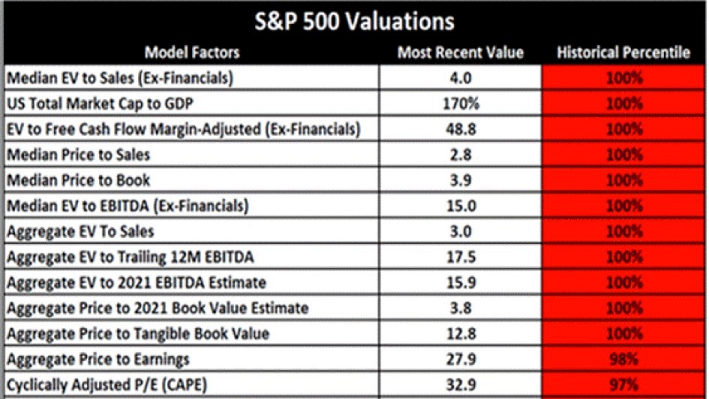

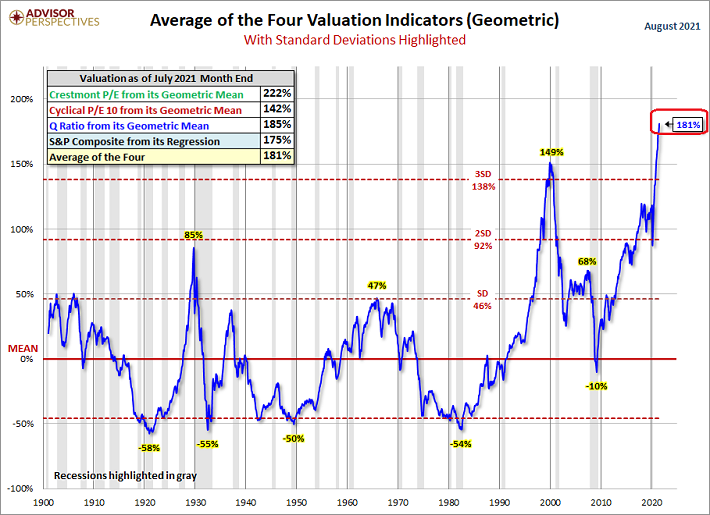

Another way to visualize the stock bubble? An average of prominent valuation measures demonstrates that participants are investing at a remarkably treacherous time.

Examine the chart above again. Right now, hold-n-hope investors face a greater risk of severe losses than they did in 1929, 2000 or 2008.

To be fair, overvaluation in stock pricing does not imply imminent danger. Yet pricing extremes in financial assets (e.g., stock, bond, real estate, etc.) present vulnerability.

For example, the U.S. Federal Reserve is hoping that inflationary pressures begin to subside. If those pressures prove to be durable, however, then the Fed may have to raise interest rates.

Indeed, inflation could force the Fed to terminate the practice of printing billions of electronic dollars to buy Treasury bonds and mortgage-backed bonds — a policy that manipulates rates much lower than they would otherwise be. And that’s not something investors are prepared for.

Sell-offs can happen slowly at first. And then all at once.

Some may already be losing the faith on the hottest tickets to ride. For instance, the multi-billion dollar ARK Innovation ETF (ARKK) has been dealing with net outflows.

Imagine what would happen to the never-say-die Nasdaq if this trend continues. You may begin to see sizable losses for Tesla, Zoom, Square, Shopify and other “disruptors.”

Would you like to receive our weekly newsletter on the stock bubble? Click here.