Is the stock market overvalued, undervalued, or fairly valued? One of the most popular metrics for making that call is the cyclically-adjusted price-to-earnings (CAPE) ratio.

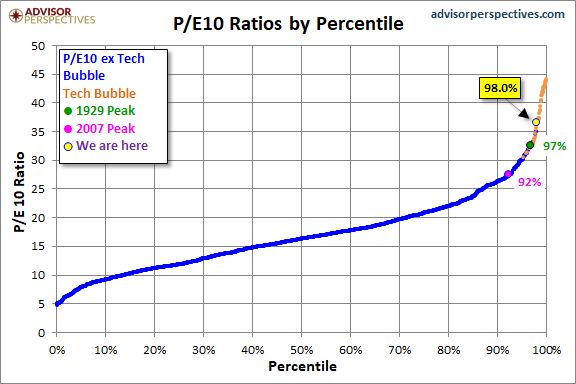

The CAPE ratio, also known as P/E10, has averaged 17.0 since the 1880s. It reached an epic level of overvaluation in 1929, hitting 32.6 prior to the infamous stock collapse and subsequent Great Depression.

Where does the CAPE ratio (P/E10) stand today? 36.5.

That’s right. Historically speaking, stocks are nuttier in 2021 than they were in 1929.

There are those who are quick to point out that P/E10 reached stupider levels in 1999 and 2000. Right before the tech stock bubble imploded.

The fact that there were a number of months in the late 1990s and early 2000s when stock prices were more overvalued than they are right now is cold comfort. The S&P 500 went on to lose 51% between March 2000 and October 2002, while the Nasdaq plummeted 78%.

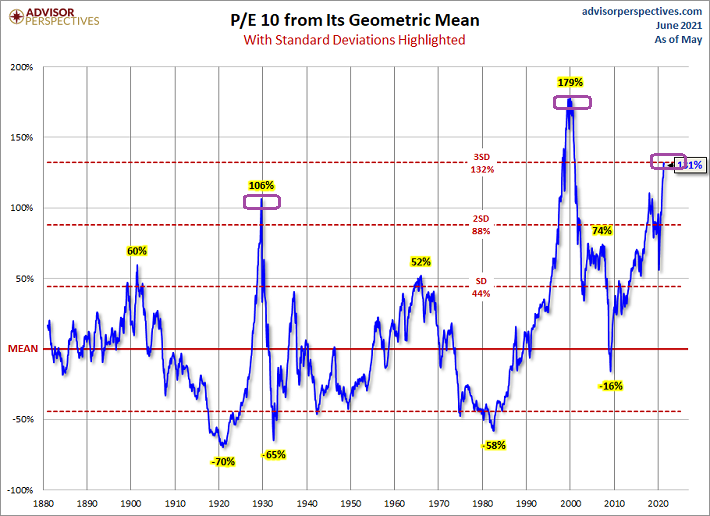

Equally disconcerting? Today’s PE/10 is three standard deviations above its mean.

Granted, overvalued stocks can remain overvalued for quite some time. Prices may be able to hold onto elevated levels for as long as the Federal Reserve can commit to zero percent interest rates (ZIRP) and hundreds of billions in asset purchases (QE).

Some experts believe that the Fed cannot continue its ultra-loose policies. Most notably, inflationary pressures may force the Fed’s hand.

It follows that a number of investors have been seeking protection from a volatile sell-off, one that might occur if the Fed dials back its mammoth support. Protection against a gut-wrenching stock collapse has not been this expensive since investors fretted tighter Fed policies in the summer and fall of 2018.

In particular, when the price of tail-risk protection via the Skew Index popped above 150 in prior instances, stocks cratered shortly thereafter. In 2018, it was a 19.9% decline on the S&P 500. In 2020, it was a 33.9% bearish drop.

Is the “Skew” suggesting that the stock market is due? Indeed, the Skew Index can be a proxy for investor sentiment.

With market overvaluation at extremes, with investors looking for S&P 500 price protection, it makes sense to mind the “Skew.” Consider trimming some of the more aggressive holdings in your portfolio. Selling high often provides one with an opportunity to buy lower.

Would you like to receive our weekly newsletter on the stock bubble? Click here.