You hear the stories in everyday life. A neighbor receives $75,000 up and above an astronomical listing price for a home. A friend boasts about making a killing in a crypto like Dogecoin or a meme stock like AMC Entertainment Holdings (AMC).

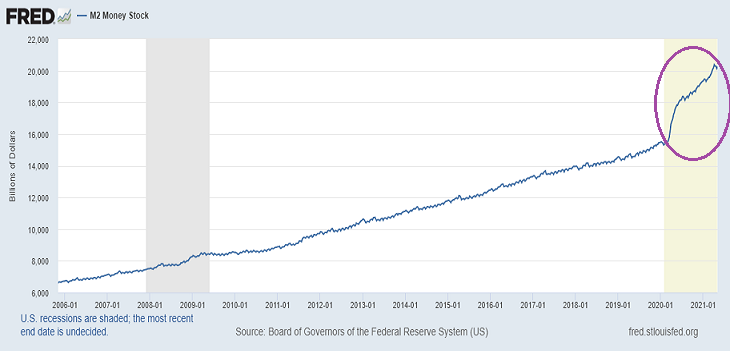

The primary reason for the monumental boom has been well-documented. The federal government distributed massive amounts of debt-financed stimulus to families and businesses, while the Federal Reserve injected trillions of digital dollars into a zero percent interest rate (ZIRP) financial system.

One problem with having an excess of money chasing a limited supply of goods and services? The dollars do not stretch as far as they used to stretch (a.k.a. “inflation”).

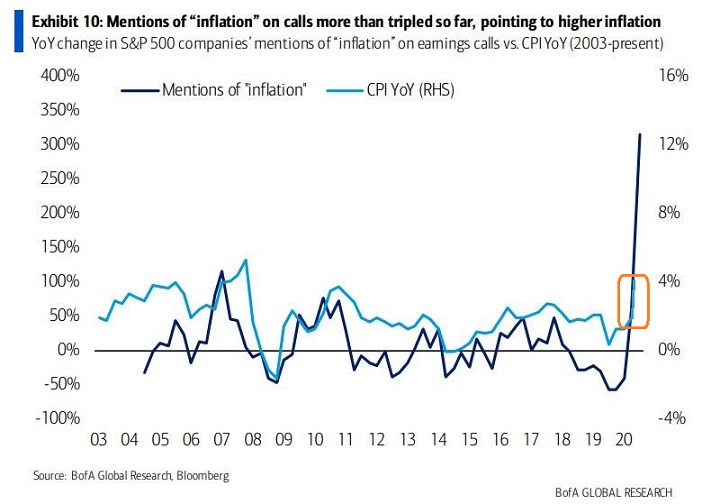

Businesses may have to cope with higher energy, food, labor, and materials costs. Often, they pass those costs down to consumers.

In the chart below, notice the spike in the dark blue line. This represents the concerns that businesses have expressed regarding inflation. Meanwhile, the lighter blue line shows a spike in the “official” inflation data of the Consumer Price Index (CPI).

Many folks erroneously assume that ever-rising real estate and stock portfolios will offset pains elsewhere (e.g., food, gas prices, store-bought products, services, etc.). Yet the primary prescription for fighting inflation – less money printing coupled with higher interest rates – would likely punish asset values.

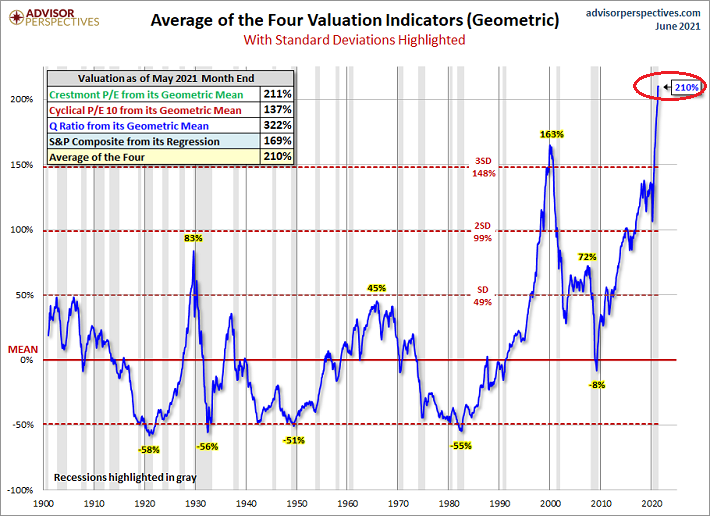

Could home and stock values weather an inflation storm? Perhaps if valuation levels were not so obscene.

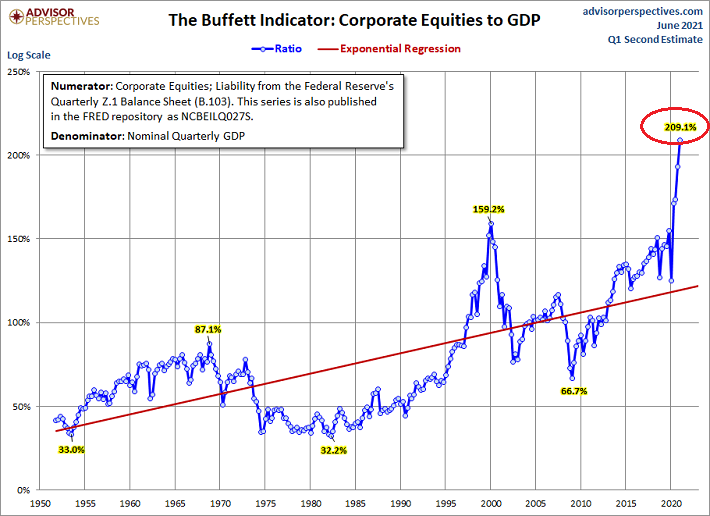

The valuation composite below is already four standard deviations above normality. That makes the irrational exuberance of the 2000 tech stock bubble appear rational.

The United States has feasted on low inflation and ever-declining interest rates for 40 some-odd years. If the four-decade paradigm shifts, asset pricing would likely revert back to the mean.

Yes, 50%-60% losses. A reckoning that is similar to 2000-2002 is more likely than not.

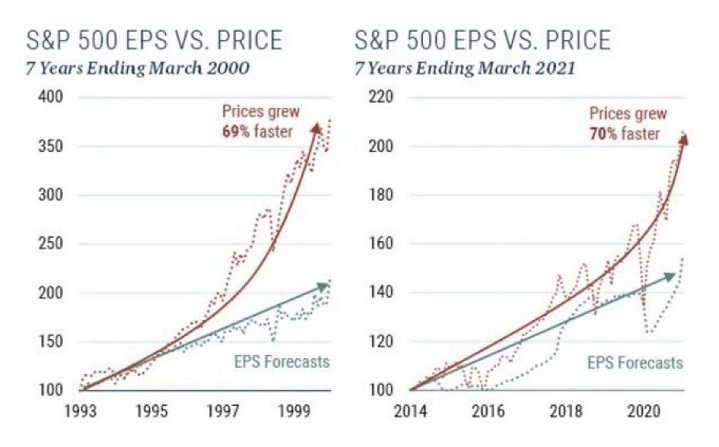

Not sure if the come-uppance will be as ugly as it was when the tech bubble burst? Get a gander at the late 1990s run-up and the present-day circumstances.

Prices will not outpace corporate earnings (or EPS forecasts) indefinitely. The only question is… will inflation be the stock bubble’s pin?

Keep in mind, the rip-roaring recovery from COVID is already factored in. Warren Buffett himself would be a fool to add money to stocks at peak valuations.

Would you like to receive our weekly newsletter on the stock bubble? Click here.