Occasionally, there are volatile sell-offs on renewed coronvirus fears and/or tensions with China. That happened here on Friday, June 26.

Yet the Nasdaq still logged an all-time high time this week. Meanwhile, the S&P 500 is only 9%-11% off its February record.

Without a doubt, the Federal Reserve has been successful in reflating bonds and stocks in its desire to maintain the wealth effect. Buying trillions of assets with freshly printed dollars has lessened the pain for debt-strapped corporations as well as their investors.

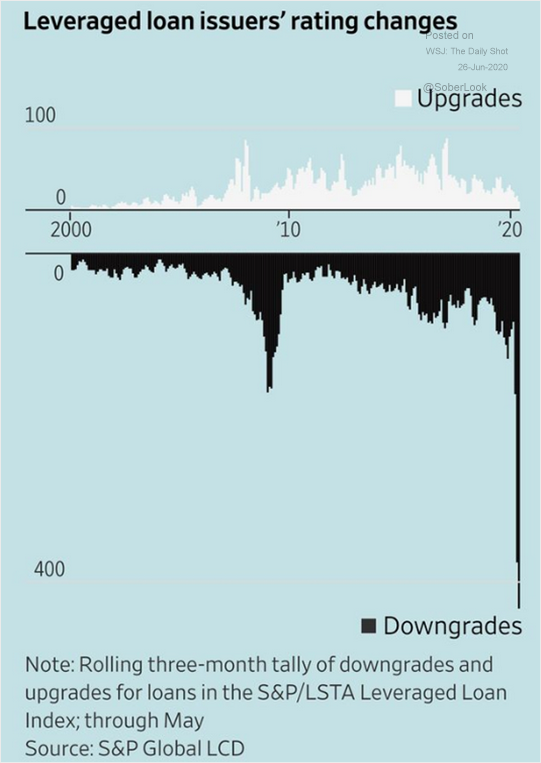

On the flip side, there are areas of financial stress that the Fed has yet to solve. For instance, the Fed will NOT acquire non-AAA rated bonds of collateralized loan obligations (CLOs) with newly originated leveraged loans. Rating agency downgrades coupled with corporate bankruptcy activity could scare off investors who worry about lower-rated slices of CLOs.

Of course, the Fed has proven that it can change its direction in a split second. They’re buying munis. They’re buying junk corporates. If they feel that they need to shore up issues in preferreds, convertibles and/or leveraged loans, something tells me that they’ll get it done.

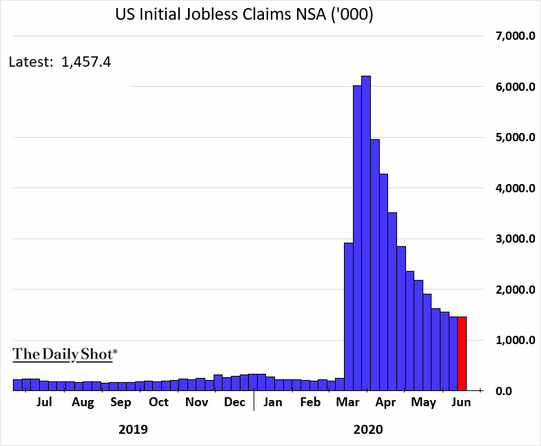

However, all of the money printing in the world may not create jobs. And right now, jobless claims have leveled off at an uncomfortably elevated data point. This likely suggests that millions and millions of positions have been lost permanently.

Structurally high unemployment would mean less consumption in the broader economy. And, by extension, companies would find themselves reporting lower earnings for much longer.

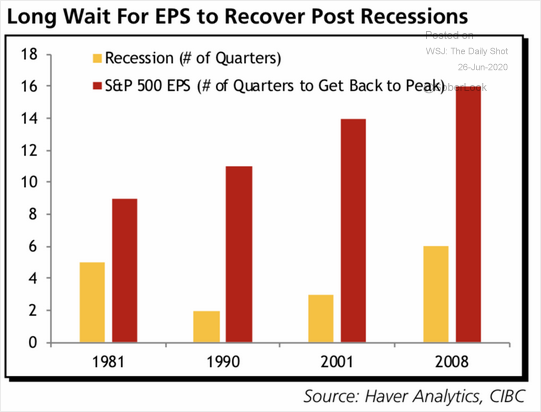

For perspective, each of the previous three recessions — 1990, 2001, 2008 – had been successively more devastating. Not surprisingly, the deeper the recession, the longer corporations needed to recover earnings per-share (EPS).

It stands to reason, then, the hit to the economy in 2020 will exact a heavier toll than prior recessions exacted on corporate profits. What it also means is that companies would be lucky to see break-even EPS data by 2023-2024.

For the S&P 500 to remain in and around the 3000 level in price, while EPS spends multiple years in recovery, is a travesty. What’s really happening? Trillions of electronically printed dollars that the Fed injected into the financial system is chasing a limited supply of public shares, where bond yields are anemic and money has to wind up somewhere.

Then again, even Fed liquidity may have its limitation. All of the extra dollars may prefer the safety of cash if the reality on severe overvaluation ever comes to the forefront.

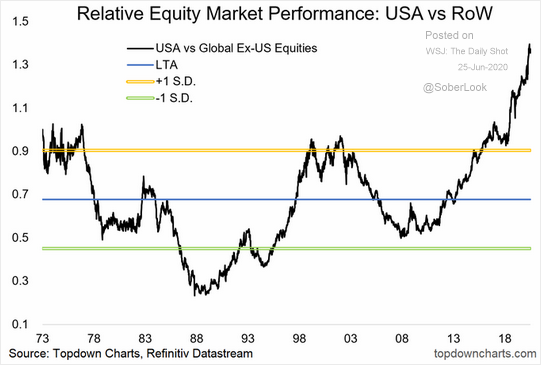

There’s another possibility. Those American dollars may prefer the shares of foreign corporations with more attractive valuations.

The discrepancy between what U.S. investors have been willing to pay for domestic stocks and foreign stocks has no precedent. Note: Two of the worst U.S bear markets in history — 1973-1974 and 2000-2002 — occurred when U.S stocks exceeded or approached 1.0 standard deviation in relative out-performance.

How does one even begin to describe the relative performance differential between U.S. stocks and foreign stocks these days? In 2019-2020? There are no words for it.

Would you like to receive our weekly newsletter on the stock bubble? Click here.