Here in 2020, market participants are willingly paying an enormous premium for profits. In particular, corporate profitability is roughly the same as it was nine years ago. In Q2 of 2011, however, the S&P 500 traded around 1300, not 3000+.

The speculative risk taking has become reckless, if not altogether absurd. Yet it is not unprecedented.

The belief in a new economic paradigm during the late 1990s created the 2000 tech bubble. Unfortunately, its inevitable bursting led to 50% losses for the S&P 500 and more than 75% price depreciation for Nasdaq devotees.

So where does today’s confidence come from? The unshakable faith in a post-pandemic utopia?

Hardly.

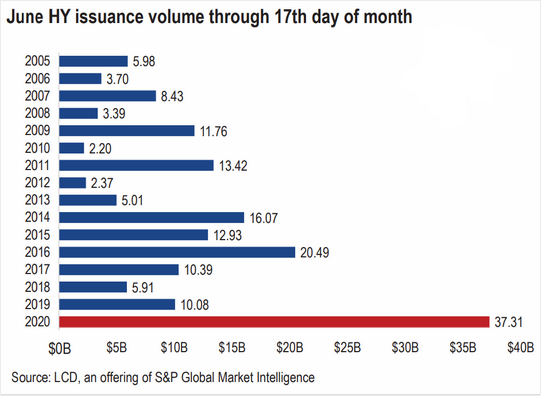

Today’s giddiness is attributable to a “do-whatever-it-takes” Federal Reserve. And that means digitally printing as much money as possible to hoover up the bonds of good businesses, bad businesses and ugly businesses.

Bad businesses are like families with poor credit scores. Only lenders often deny families with poor credit scores access to credit, whereas the Fed is making sure that bad businesses have plenty of access to 5% and 6% borrowing terms.

It used to be that debt-laden companies with questionable recovery plans would see their stock shares suffer accordingly. In particular, if a company could go bankrupt, its stock value would be wiped out.

Not so today. The Fed’s intentions to rescue everyone and everything is largely overriding legitimate economic issues (e.g., potential for persistent unemployment, prospect of renewed geopolitical tensions, possibility of coronavirus disruptions, threat of bankruptcy wave, etc.).

One might make the case that in the depths of the market despair this past March, the Fed had to calm financial markets to get credit flowing again. Yet why is it now okay to reflate the bond and stock bubbles that existed before the coronavirus crisis?

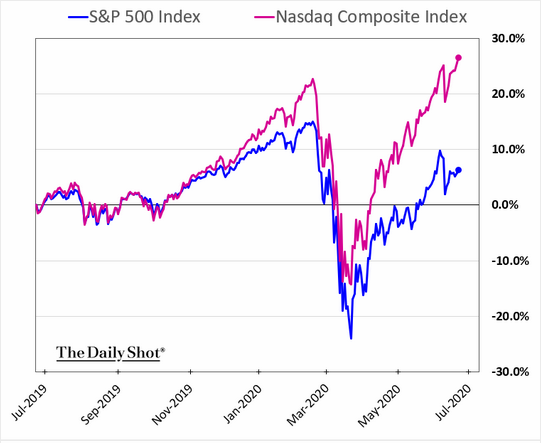

The S&P 500 is a mere 7%-9% from reclaiming its all-time peak. Meanwhile, the Nasdaq has broken out to new records.

That’s not all. The Nasdaq has dramatically decoupled from the S&P 500 with the relative performance differential reaching 2000 basis points (20%).

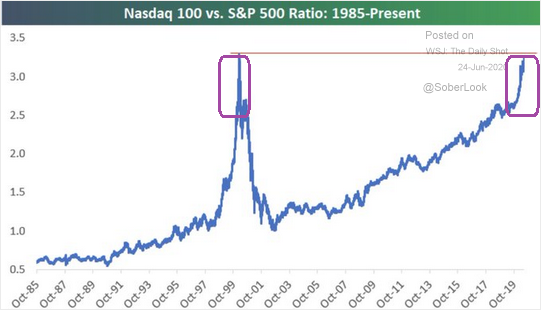

The Nasdaq 100 (QQQ):S&P 500 (SPY) price ratio paints a similar portrait. In essence, relative outperformance is hitting extremes.

Will the Nasdaq tech train continue to reap the benefit of price agnostic trading? With trillions of Fed dollar liquidity getting into the financial markets, many are betting that the party will last forever.

Of course, many have experienced terrific parties, only to wake up later with painful hangovers. Protecting one’s portfolio during severe hangovers may be more critical than hoping for perpetual records on the Nasdaq.

Would you like to receive our weekly newsletter on the stock bubble? Click here.