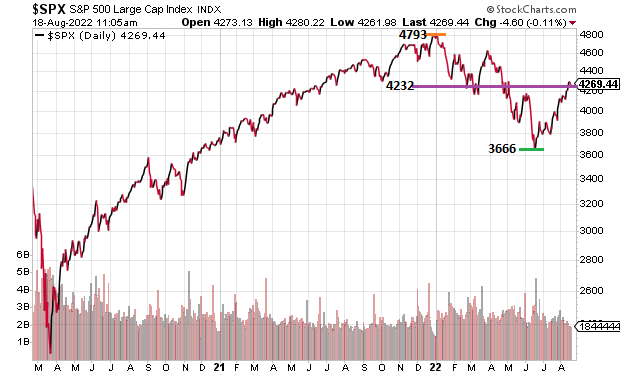

Have we seen the bottom for the stock bubble?

Bullish enthusiasts point out that when stocks have recovered more than 50% of their bear market losses, they’ve never fallen to new lows. For these folks, once the S&P 500 surpassed 4232, the bear market ended.

On the flip side, the only time that a bear market low occurred during a Fed tightening cycle was during the 1987 stock market crash. At that time, however, the S&P 500’s forward P/E was less than 10. Today? The WSJ.com estimate is 18.7.

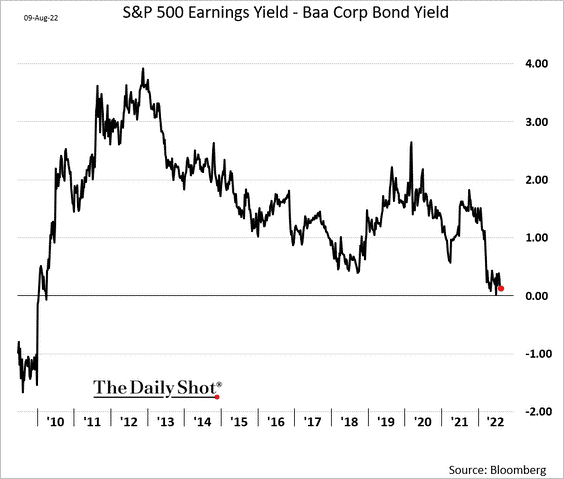

One can also see severe stock overvaluation at the earnings yield (E/P) level. The earnings yield is a meager 5.3%. Why take outsized stock risk when the E/P is only marginally better than 5.1% — the yield one can get from a medium-grade corporate bond?

In truth, many are betting that the Federal Reserve will be giving up the inflation fight sooner rather than later. Not only that, the bet is that the Fed will be forced to start cutting rates to stimulate the economy again.

That is a pretty strange bet.

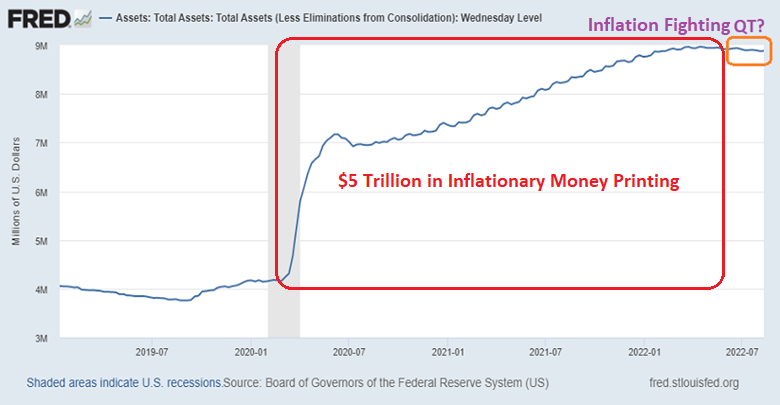

For one thing, the central bank plans to reduce its own inflationary footprint by getting rid of hundreds of billions, possibly trillions, of dollars on its balance sheet. The Fed intends to move at a clip of $95 billion per month beginning in September.

In other words, trillions of dollars that helped push the demand for stocks through the roof throughout 2020 and 2021 will slowly be coming out of the financial system. The “tightening” will occur alongside additional rate hikes.

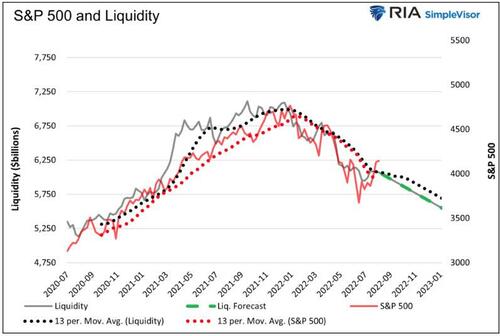

Recently, Michael Lebowitz, an investment analyst and portfolio manager for RIA Advisors, set out to quantify the Fed’s impact on the S&P 500. He developed a formula that addresses when the Fed is adding liquidity to the financial system or removing it. If the Fed keeps its promise to reduce its balance sheet by $95 billion a month, Lebowitz anticipates the S&P 500 hitting 3500 by the end of 2022.

More critical than a price forecast is the reality that stocks correlate highly with the direction of Federal Reserve intervention. And the Fed may be in tightening mode for a whole lot longer than the market expects.

It follows that, unless the Fed intends to cause irreparable damage to its inflation-fighting credentials, stocks will be heading lower. Much lower.

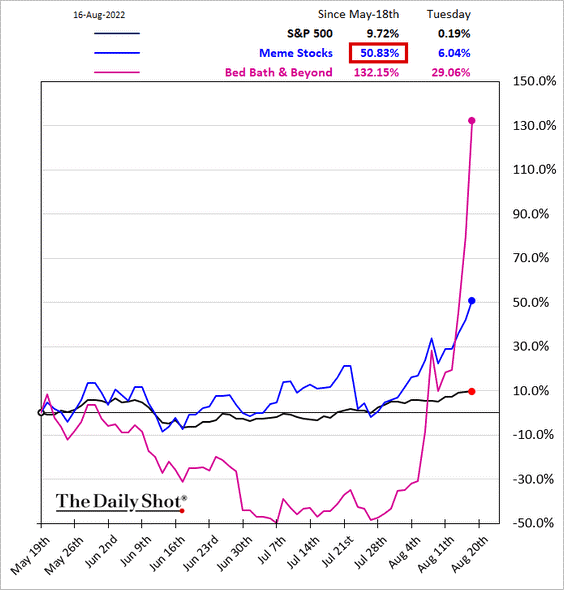

Except for meme stocks… where stupid is as stupid does.

Would you like to receive our weekly newsletter on the stock bubble? Click here.