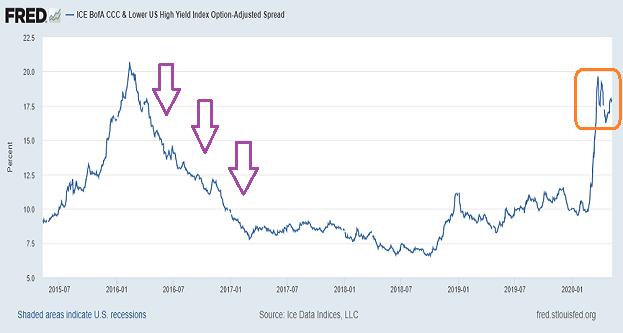

In 2016, oil prices fell dramatically, sending shivers down and up the spines of energy bondholders. Investors worried that a slew of energy companies would go belly up.

In 2020, weak demand for oil is only part of the economic concern. Fragile demand across a wide variety of industries — brick-n-mortar retail, hospitality/tourism, basic materials, energy, lending/financials, commercial real estate, auto, restaurants, sports/leisure, airlines, transporters and more — is likely to persist.

The probability that a wave of bankruptcy filings will hit has kept CCC junk bond spreads elevated. Unlike 2016, however, the investment public is not convinced that central bank liquidity and tech stock speculation will be sufficient to push down the borrowing costs of questionable corporations.

Bankruptcies, of course, can wipe out stockholders too. It follows that cautiousness in the junk bond market about inevitable insolvencies strongly suggests that the bear is still lurking.

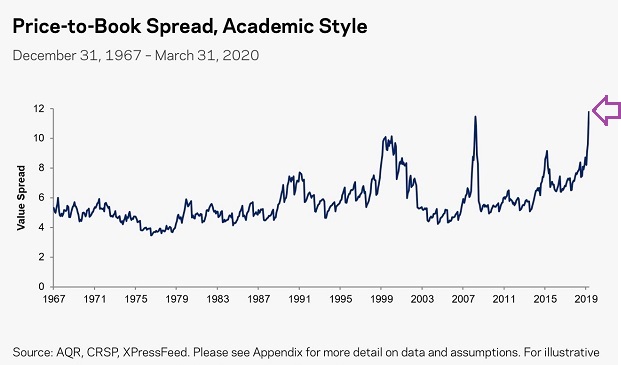

Granted, speculators may continue to push stocks higher, defying economic rationale. Yet even stock investors may begin to wonder about the price they are currently paying relative to “book value.” The highest price-to-book (P/B) in market history is one more sign of stock bubble silliness.

Would you like to receive our weekly newsletter on the stock bubble? Click here.