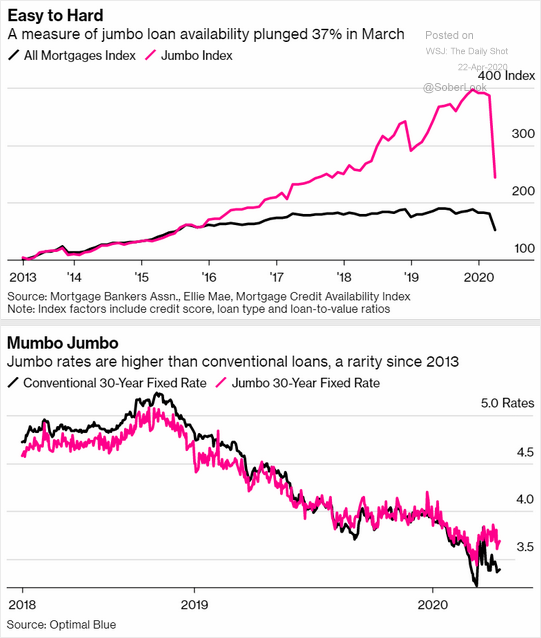

Lenders continue tightening their belts. For example, it’s getting harder and harder to procure a jumbo mortgage loan, as its availability has cratered by 37%. Even if one qualifies for a jumbo, he/she will see higher rates than conventional loans for the first time since 2013.

Obviously, this will not help the housing market. Nor will it help the “wealth effect.”

People who feel wealthier due to stable employment prospects and ever-rising asset prices consume more. People who feel less wealthy due to unemployment/underemployment/reductions in salary as well as lower asset prices (e.g., stocks, bonds, real estate, etc.) consume less.

The sharp decrease in consumption has already forced a number of oil producers and retailers into bankruptcy. Shareholders of these companies have been wiped out.

Ironically, the stock market continues to trade around its 50% bear market retracement. This is unlikely to last. The Federal Reserve, Bank of Japan and European Central Bank can crank up the electronic printing press as much as they want, but they cannot force lenders to lend; they cannot force consumers to take on more debt either.

Would you like to receive our weekly newsletter on the stock bubble? Click here.