Scores of pundits are getting bullish on stocks. Their reasoning? We may have reached peak pessimism.

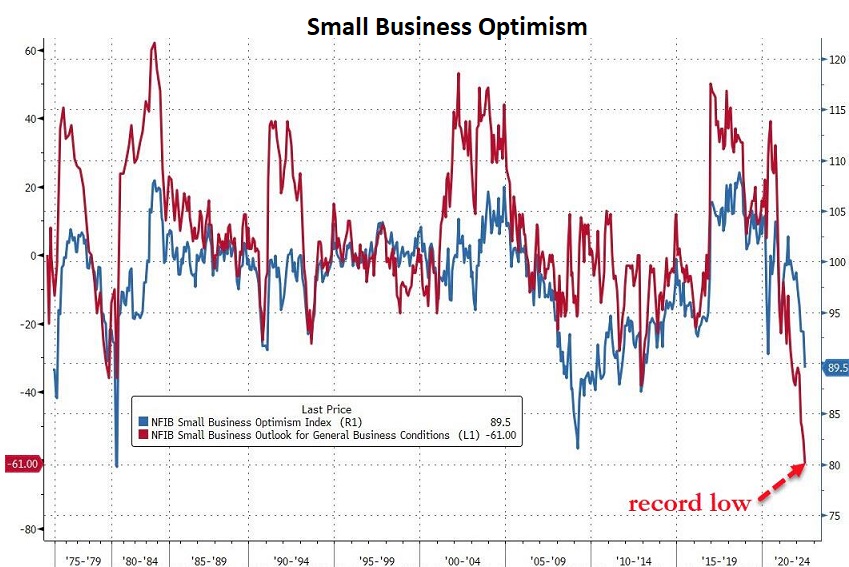

For example, small businesses have never expressed more concern about the outlook for future business conditions.

However, the stock market is probably not pessimistic enough. The S&P 500 is only down 17.3% from all-time highs at a time when economic recession is a near-certainty.

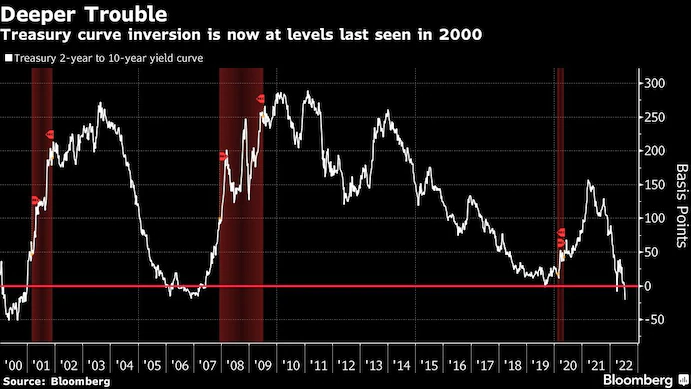

It is worth noting that three-month Treasury bills as well as two-year Treasury notes both yield significantly more than 10-year notes. This “inversion” has preceded each of the past seven recessions.

In a similar vein, banks are unlikely to profit when they have to borrow short-term dollars at higher rates than what they might earn from longer-term loans (e.g., mortgages, cars, business, etc.). Lenders who do not have an incentive to lend? That is a recipe for economic hardship.

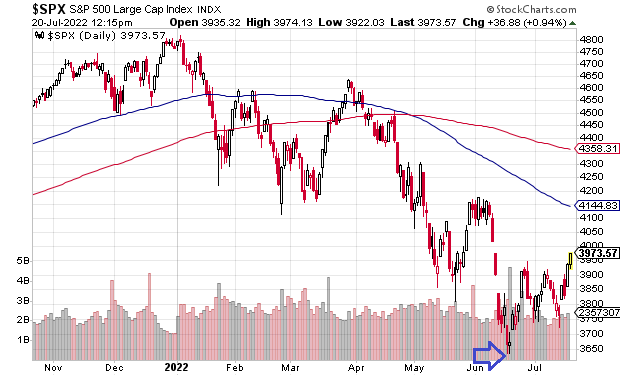

It follows that the upward trajectory since the mid-June stock lows are likely to represent a “dead cat bounce.”

Keep in mind, the average stock market decline in a recession approximates 33%. The S&P 500 would need to tag the 3200-3300 range before reaching average depths.

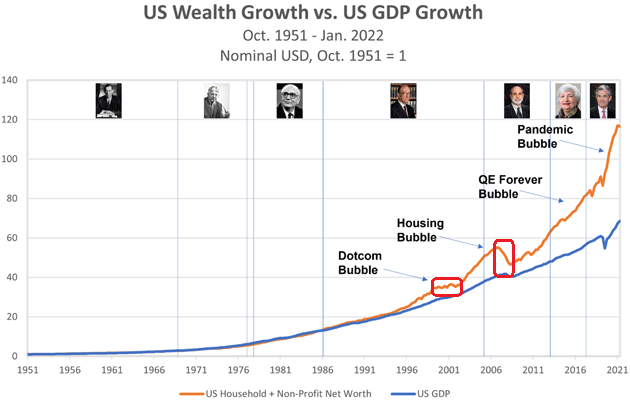

What’s more, stocks have yet to revert to the trendline growth of the economy. Net worth via stocks, bonds and real estate came in closer contact with economic growth (GDP) in previous recessions.

Would you like to receive our weekly newsletter on the stock bubble? Click here.