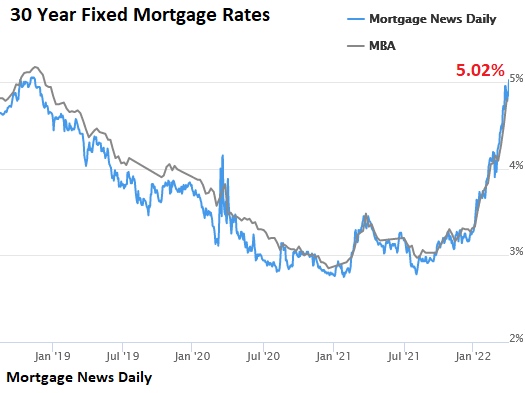

Higher borrowing costs are already slamming the brakes on real estate. For example, a few months ago, one might be able to get a 30-year mortgage at 3%. That mortgage has catapulted all the way up to 5%.

The difference between borrowing $500,000 at 3% and borrowing it at 5% comes out to nearly $7,000 more per year. Every year.

There’s more.

Home prices are now 30%-40% higher than they were the last time a 30-year mortgage came in at 5%. The consequence? Millions of families no longer qualify to purchase a home.

Best case scenario? Real estate values flatten out across an extended period. More likely, perhaps, home values sink.

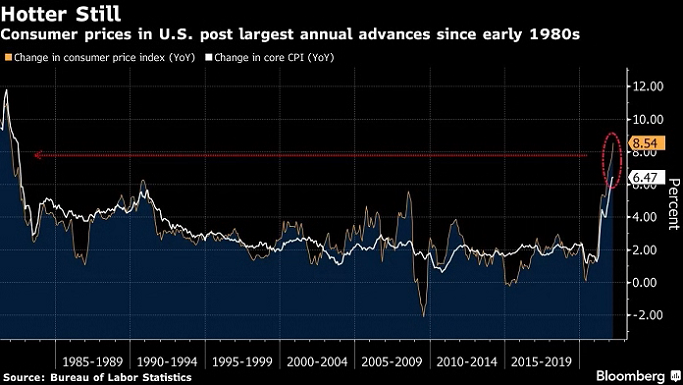

The fact of the matter is that things are getting very expensive. Consumer prices are rocketing at a pace that households have not seen in 40 years.

The backdrop implies that the U.S. government must “do something” about the painfully high cost of living. Specifically, the Federal Reserve will continue to raise its lending rates as well as terminate its money printing activity.

In sum, when the price of money goes up this far (and this fast), people and businesses may not be able to come to terms with the higher borrowing costs. Economic activity may suffer.

How has the stock bubble responded? One might say that stocks have been resilient so far.

However, stock sectors that typically do well in a strong economy – technology, consumer discretionary, industrials, “growth” – have been laggards. In contrast, stock sectors that typically hold up well in a shaky economic environment – consumer staples, health care, “value” – have emerged as leaders.

One way to visualize the shift from growth to value is to chart the performance of the Nasdaq alongside a value-oriented fund like Vanguard Value (VTV). Over the last six months, the Nasdaq has returned -5% in volatile fashion, whereas VTV has quietly gained more than 5%.

Will the Federal Reserve be successful in its battle against inflation? Maybe. Forty years ago, the Fed beat back rapidly rising consumer prices, but the actions came at the expense of an economic recession; investors also experienced a 30% bearish retreat in the stock market (1981-1982).

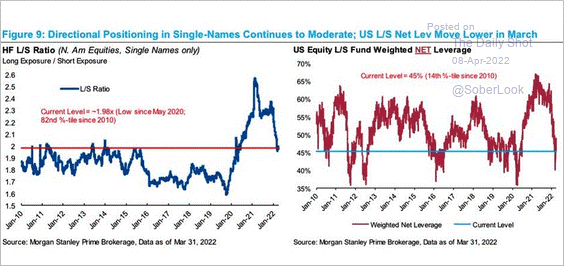

The so-called smart money is worried. Hedge funds continue to cut exposure/net leverage to individual equities.

With stocks likely to lose (possibly a lot) while the Fed is fighting inflation, and cash guaranteed to lose when adjusted for inflation, investors feel obligated to place money somewhere. Commodities have been one answer.

There may be another: Short-Term Treasuries.

Consider the reality that one is likely to garner 2% from a 1-2 year proxy over the next 12 months. And when the Fed shifts from fighting inflation to fighting a recession as well as bearish stock depreciation in 2023 – when the Fed eventually reverts back to zero percent rate policy – an investor can anticipate bond price appreciation.

Will it be a windfall? Hardly. Yet it should be better than holding cash alone.

Additionally, should the stock bubble get rocked for 33%-50% losses, one will be able to use these low-risk holdings to acquire exceptional stock bargains. Short-term government bonds and short-term investment grade credit should provide one with the optionality to acquire company shares at a remarkable discount.

Would you like to receive our weekly newsletter on the stock bubble? Click here.