Rising interest rates? Check. Geopolitical tensions? Check? Inverted yield curve? Check.

According to the research firm, CFRA, these factors alone are highly likely to be accompanied by a stock bear. When a recession has developed within 12 months of these items, though, a bearish price reckoning occurred 100% of the time.

There are other concerns as well.

The United States is currently experiencing the worst inflation since the early 1980s. Equally disconcerting, the U.S. stock market sits at its most extreme valuations across a a wide variety of tried-and-true metrics, like price-to-earnings, price-to-sales, the Q Ratio, and market-cap-to-GDP.

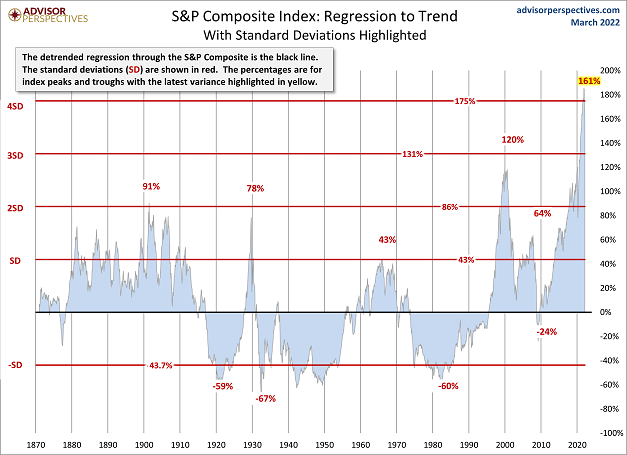

Note: Stock market overvaluation reached three standard deviations above its mean in the 2000 stock bubble. Here in the 2022 stock bubble, the market is four standard deviations above the mean, hitting levels that have never occurred in the history of available data.

Add it all up, and the stock bubble may deflate dramatically.

The most optimistic scenario is that the Federal Reserve’s tightening — hiking the Fed Funds Rate (FFR) and reducing its balance sheet — beats inflation without causing a recession. Yet that did not work out so well in 1981-1982 when stocks gave up 30%.

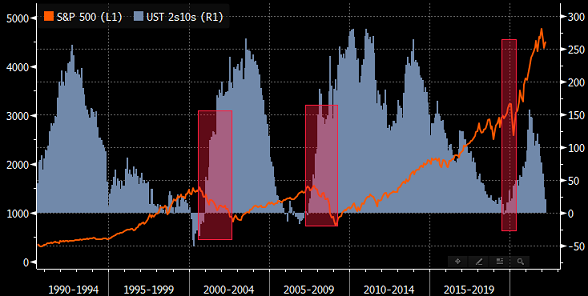

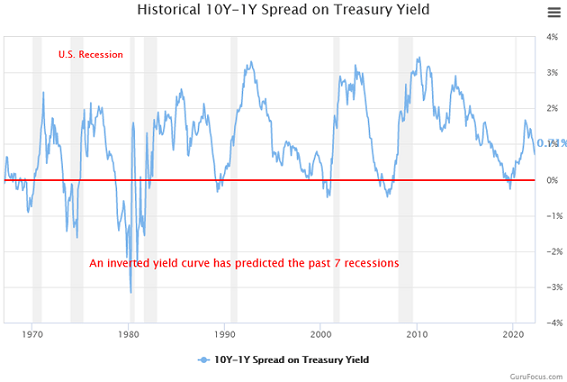

With the inverted yield curve alone, recession may be preordained. Two-year Treasuries already yielded more than ten-year Treasuries. And the 1Y is on its way.

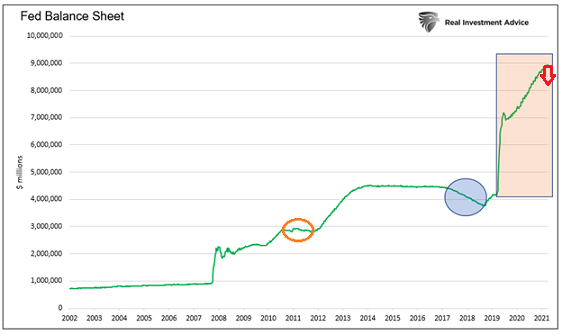

Keep in mind, since the Fed began quantitative easing in 2008, the direction of its balance sheet has corresponded with the direction of U.S. stocks 85% of the time. In 2011 and in 2018, stocks were slightly down.

With Fed board members promising to rapidly decrease its balance sheet in May of 2022, what are the chances that stocks ignore those implications?

It is worth noting that the S&P 500 has experienced 26 bear markets since 1928. The average depreciation for those bears? -36%.

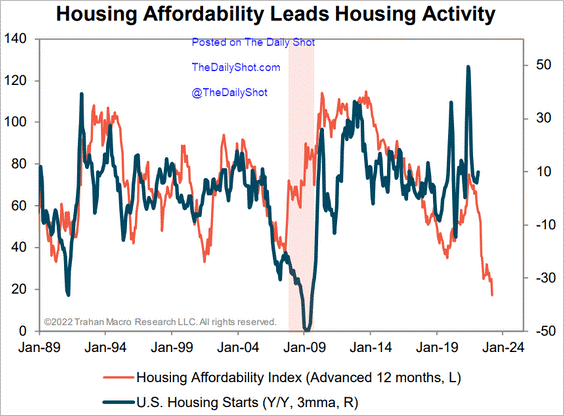

Of course, bigger collapses tend to accompany bigger problems. We have the most hyper-valued stock pricing on record. We are experiencing one of the worst inflationary cycles. And the cross-currents from housing unaffordability may be an equally pesky fly in the proverbial ointment.

That’s right. Housing is even less affordable than it was in 2007, right before the Great Recession and the -52% top-to-bottom losses for the S&P 500.

As popular yield curves continue to invert, the mainstream media and Fed officials will downplay the signal. They’ll talk about an economic soft landing. They will “play up” the possibility of a minor recession that can be offset by the eradication of inflation.

Sounds good… in theory.

On the flip side, why should investors believe the stock market will prove resilient in the face of 8-9 rate hikes as well as significant balance sheet reduction? When the evidence clearly points in the opposite direction? When monumentally higher borrowing costs destroy affordability in housing? When a single-family residence now takes up eight-to-ten years of personal income, a figure that is 50% greater than the long-term average?

The only reason is faith. A belief that before the economy itself breaks, and before the stock market falls too far, the Fed will have the foresight to shift immediately back to balance sheet expansion (a.k.a. electronic money printing) and zero percent rate policy. That’s the hope.

Unfortunately, hope may not be the best path forward. Rationality may make more sense.

In particular, instead of thinking how the stock market is going to make you rich, one can think about ways to avoid losing a ton of money. Managing stock bubble risk is sensible for avoiding financial regrets. Better yet, one is likely to have the opportunity to acquire beaten down assets (e.g., stocks, bonds, real estate, etc.) at bargain prices.

Would you like to receive our weekly newsletter on the stock bubble? Click here.