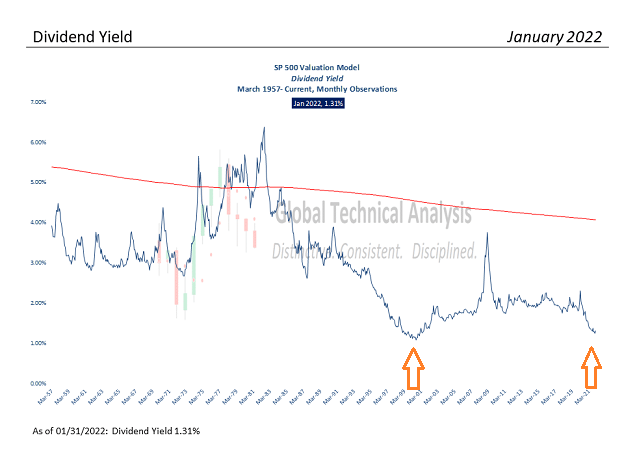

The dividend yield for the S&P 500? About 1.3%. That’s about 65 basis points lower than the yield on a 10-year Treasury bond.

The dividend yield is also nearing lows not seen since the stock market crash at the turn of the century.

Some investors might be asking themselves the question: “Would I rather get a risk-free 2% from the federal government for 10 years… or 1.3% from stocks with the possibility of price appreciation to boot?” After all, stocks almost always have positive price gains over a decade, don’t they?

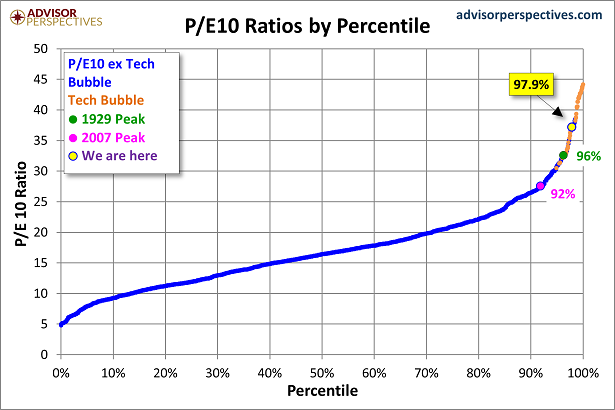

Indeed, most 10-year rolling returns for the S&P 500 are positive. However, when 10-year rolling returns have been negative, the periods typically began at extreme valuation levels.

For instance, when the tech stock bubble burst in 2000, the subsequent decade witnessed price losses. Ironically enough, the present-day stock bubble boasts equally obscene valuations as measured by the CAPE P/E10 ratio.

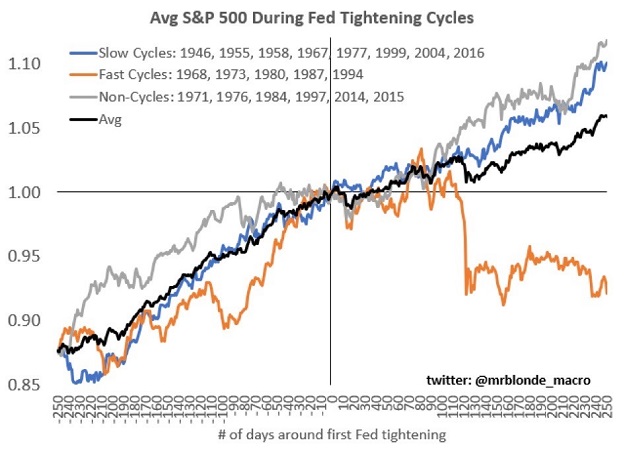

There is another reason to compare today’s stock bubble with the tech stock mania from 1999-2000. Federal Reserve monetary policy.

Specifically, the Fed started to raise interest rates in June of 1999. It was a slow process. Yet, by March of 2000, stocks could no longer withstand the rate hiking pressure. The S&P 500 plummeted 51%; the Nasdaq experienced a 76% price collapse.

Should investors take comfort in the notion that the previous stock bubble did not pop until nine months after the Fed began hiking rates? Probably not.

The Fed tightening that began in 1999 was carried out rather slowly. The Fed tightening that is about to occur today is expected to be rather aggressive in an effort to curb inflation. And fast Fed tightening cycles tend to see losses right out of the rate hiking gate.

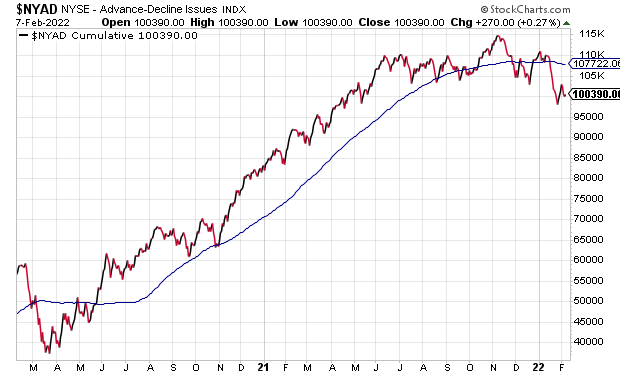

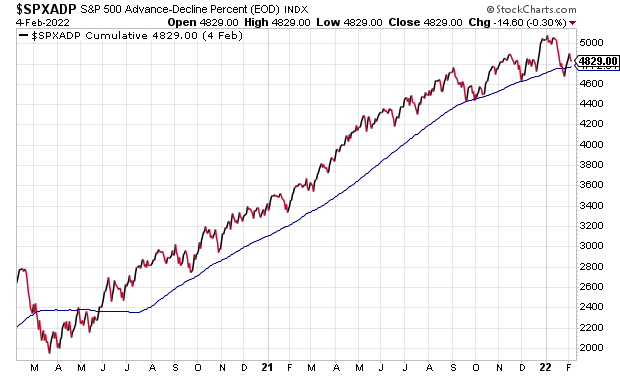

In fact, the stock bubble may be deflating already. The technical price damage in the New York Stock Exchange’s Advance Decline (A/D) appears to be gathering steam.

On the flip side, the S&P 500 continues to hold up better than broader measures of equity health.

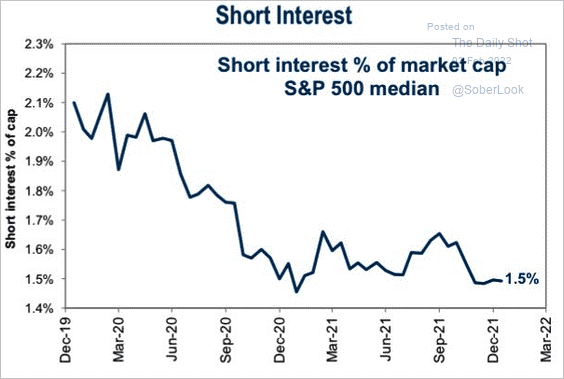

Additionally, right now, there are very few folks who are interested in shorting stocks.

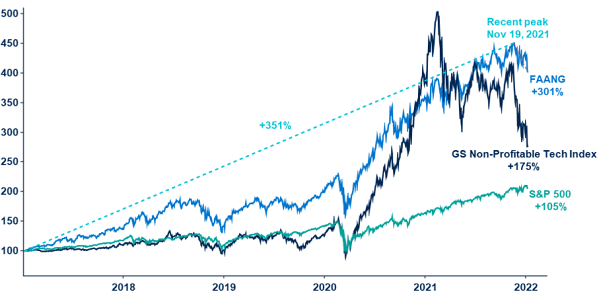

If you are a buyer, despite mounting evidence that stocks may struggle in the coming months, be mindful of quality. Profitless companies may rocket when the Fed is tossing trillions of dollars into the arena. They tend to get whacked when the Fed is tightening the reins.

Would you like to receive our weekly newsletter on the stock bubble? Click here.