The Federal Reserve electronically created close to $5 trillion for the U.S. government to hand out in the pandemic. Here in 2022, we are seeing the consequences of our government’s money printing gone awry.

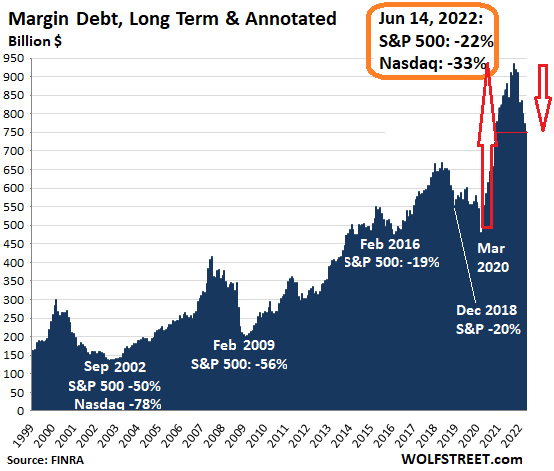

For instance, 2020 investors “took advantage” by borrowing on margin to finance stock market dreams. Indeed, the steep spike in margin debt that occurred between March 2020 and October of 2021 is unmatched in history.

Unfortunately for some folks, margin debt peaks eventually meet with “margin calls.” That’s a fancy way of saying that when stocks stark to sink, those who borrowed to finance stock acquisitions are forced to sell. And forced selling leads to more selling, until the predominant market reality becomes grotesque loss.

That’s what is taking place today. And yet, the unwinding of margin debt may only be getting started.

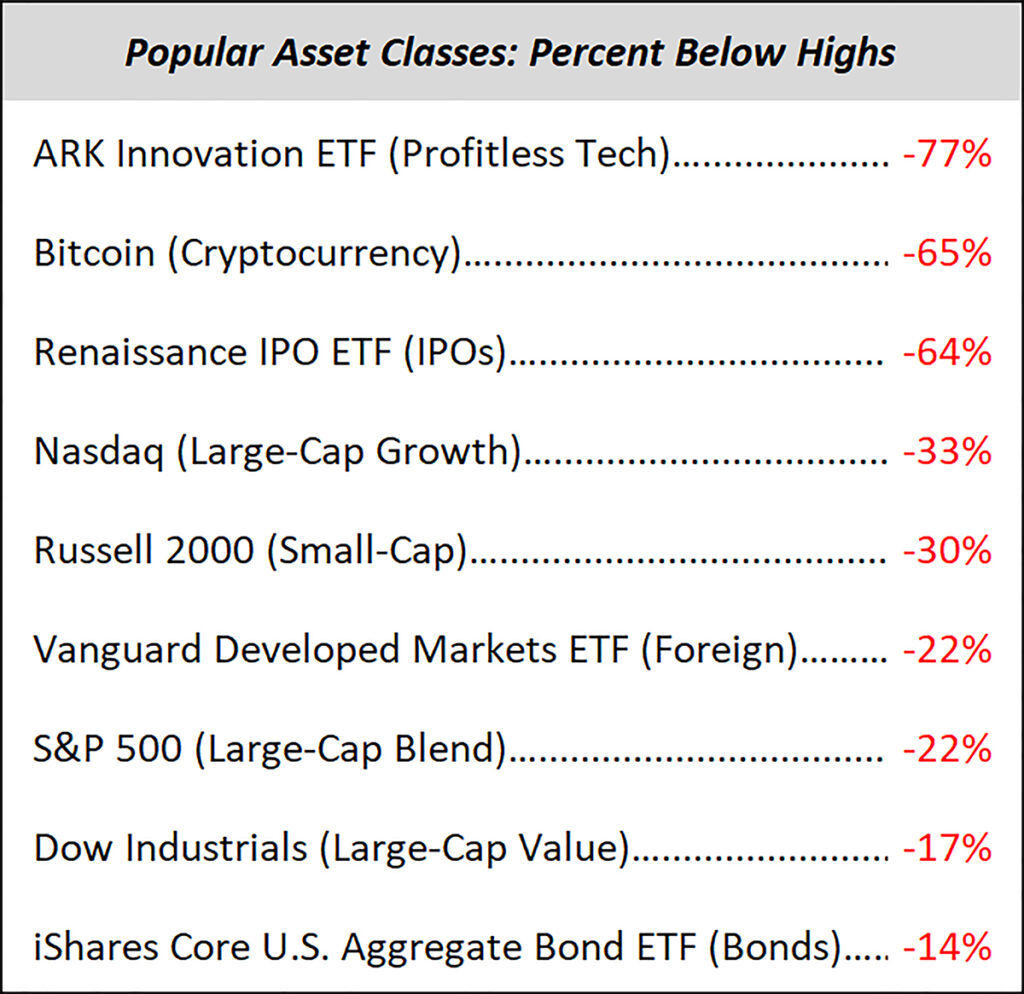

Most of the “drop from the top” has occurred in the profitless technology space – car tech, real estate tech, financial tech (a.k.a. fintech), tech tech.

- Carvana: -94%

- Redfin: -92%

- Teladoc: -90%

- Coinbase: -88%

- Rivian: -84%

- Shopify: -83%

- Palantir: -83%

Yet, even the most well-respected names have been coming unglued. Just get a gander at the FANNG cluster.

- Netflix: -76%

- Meta (Facebook): -57%

- Nvidia: -54%

- Amazon: -45%

- Google: -28%

Most of the damage, however, has been confined to growth-oriented companies. Profitless tech, crytpo-cultish, IPOs. The broader large-cap space as measured by the Dow Industrials and the S&P 500 has barely been scratched by the bear.

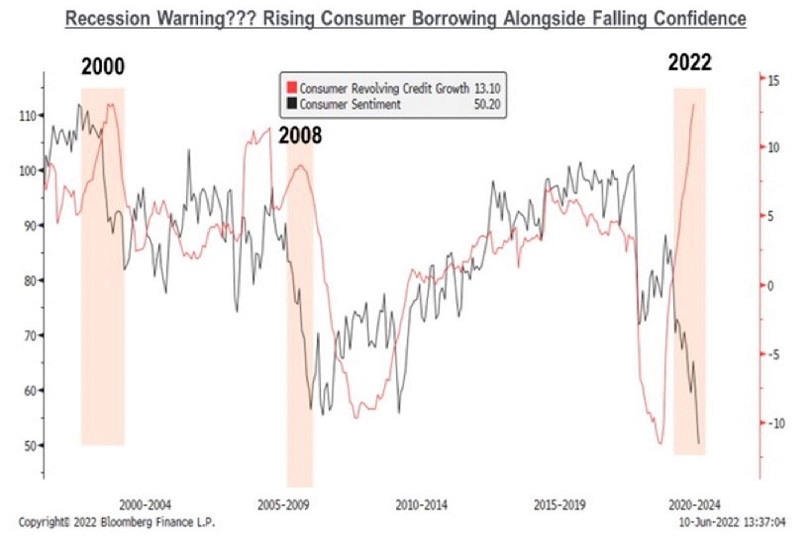

In all likelihood, though, these indexes will “catch down” to the rest of the carnage. With consumers using their credit cards to pay for goods and services, and with the Fed aiming to reestablish credibility as an inflation fighter, the economy will experience a recession.

Recessionary stock bears? Those typically do not end until big-time indexes like the S&P 500 plummet 35%-50%.

Would you like to receive our weekly newsletter on the stock bubble? Click here.