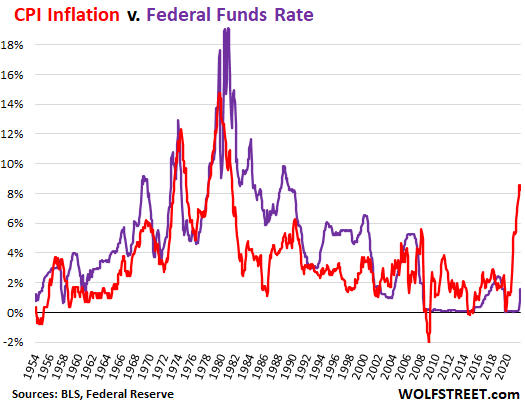

There are those who believe that the U.S. can avoid an economic downturn while simultaneously battling a 40-year high in the inflation rate. The problem? There has never been a time when annual inflation has been reined in by more than two percentage points without a concomitant recession.

Never.

And that suggests bringing 8.6% down to 6.6% is likely to come with negative GDP.

There’s more.

Meaningfully reducing inflation typically demands a Fed Funds overnight lending rate (purple line above) that is higher than CPI (red line above). Does anyone believe that Powell and his colleagues will be hiking the Fed Funds Rate from the 1.5%-1.75% level all the way up to 6%, 7%, or 8%?

The economy is already waning. In Q1, GDP was negative. And the Fed itself is forecasting zero growth in Q2.

Should Q2 actually come in with negative growth, that will be the second consecutive quarter of contraction. And by the bulk of textbook definitions for recession, two consecutive quarters with negative GDP fits the bill.

In other words… we might have arrived already.

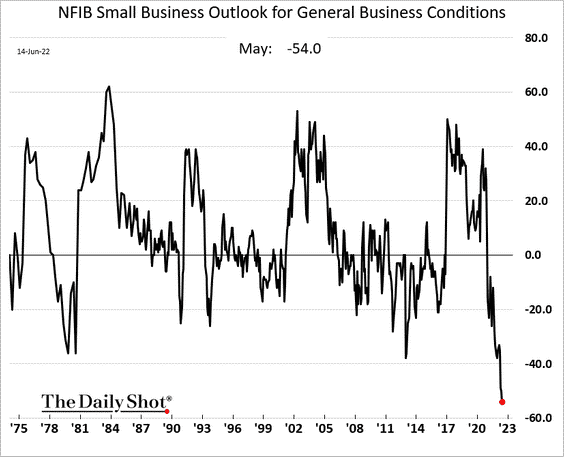

There are additional signs as well. The heart and soul of the U.S. economy is the “small business.” And small businesses have never been more downbeat than they are right now.

What does all of the evidence imply for stocks? It means we haven’t come close to seeing the bear market lows.

Not for the major indexes like the S&P 500, the Russell 2000 or the Nasdaq. Nor have we seen the lows for profitless tech in “greater fool” investments like the ARK Innovation ETF (ARKK).

Would you like to receive our weekly newsletter on the stock bubble? Click here.