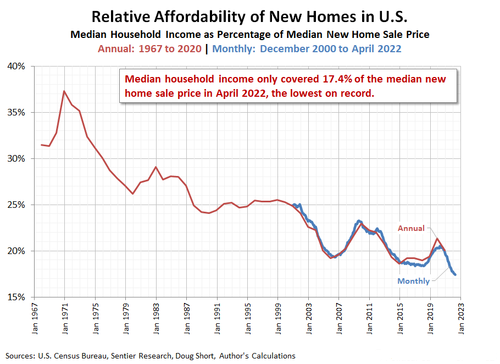

Depending on the measure, housing has rarely been less affordable. For instance, if one looks at average (median) household income as a percentage of median new home price, homes have never been less affordable.

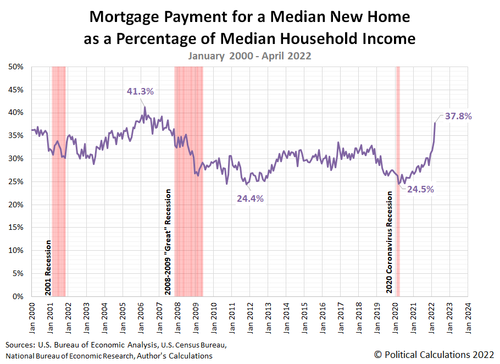

If one simply looks at mortgage payments, however, the payment as a percentage of household income is still lower than the mid-2000s housing bubble. Not that we should be comforted by the idea that 37.8% of a typical family’s income goes towards a mortgage alone.

What the charts are not able to highlight? Demand destruction.

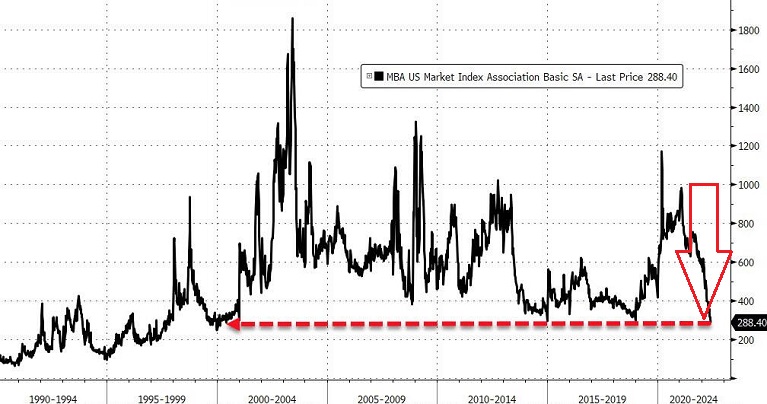

With the Federal Reserve having guided 30-year mortgages from the 3% level to the 5% level, the pace of people applying for mortgages has collapsed. Relatively few are even trying to buy a home this summer.

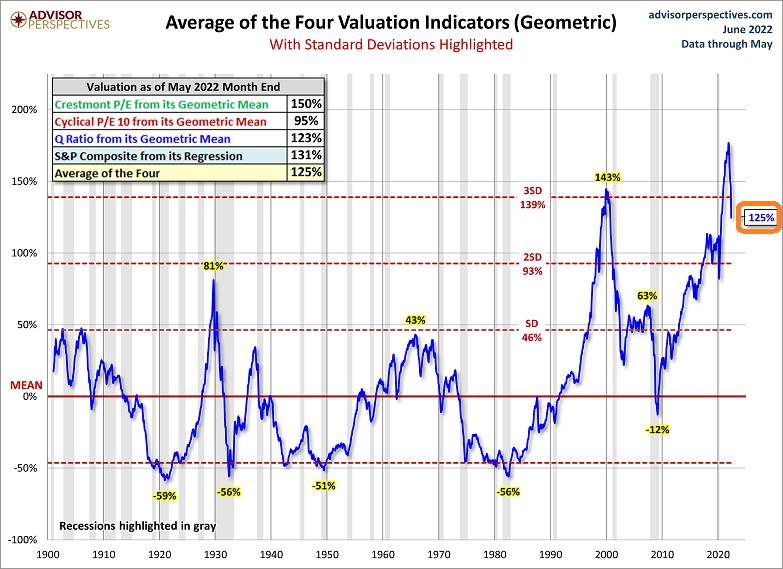

What’s more, if the current residential real estate bubble plays out like its predecessor, the shock to the economy would send stocks tumbling. Especially since the stock market remains egregiously overvalued.

Would you like to receive our weekly newsletter on the stock bubble? Click here.