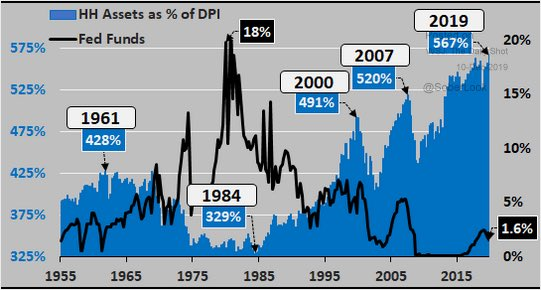

The Federal Reserve has engineered a variety of asset bubbles by suppressing and manipulating borrowing costs. Leading up to the bursting of 2000’s stock bubble, household assets as a percentage of disposable personal income nearly reached 500%. In 2007’s real estate bubble, it reached 520%. By 2020, after a decade characterized by quantitative easing and zero-percent rate policy, household assets as a percentage of disposable personal income reached a staggering 567%.