How do you know that we’re living in a monstrous stock bubble? Bullishness on ever-higher asset prices exists for every imaginable circumstance.

For example, no matter who wins the election, stocks will surge. If it’s Biden, gobs of fiscal stimulus will be sent to the American consumer. Maybe more than once. If it’s Trump, ongoing tax cuts and regulatory reform will stimulate the economy.

(And don’t be a naysayer. If there’s the slightest hiccup, the Federal Reserve will print more money and buy more market-based securities. You cannot lose!)

Record debt levels? Who cares. Anemic corporate earnings? Not important. Permanent layoffs? Government will take care of them. Extreme stock overvaluation? Price is irrelevant in a post-pandemic stock market.

Stocks have nowhere to go but up because they’ve got the ultimate backstops. The Fed prints money that it shouldn’t print. The government spends money that it doesn’t have.

Of course, there are a few folks who are questioning this mainstream wisdom. Asset manager Cole Smead explained that Microsoft (MSFT) stock cannot produce any wealth for investors over the next 10 years with a price-to-earnings (P/E) ratio of 40. He acknowledged the company’s greatness, though warned that investors are paying an irrational price today for a piece of the Microsoft pie.

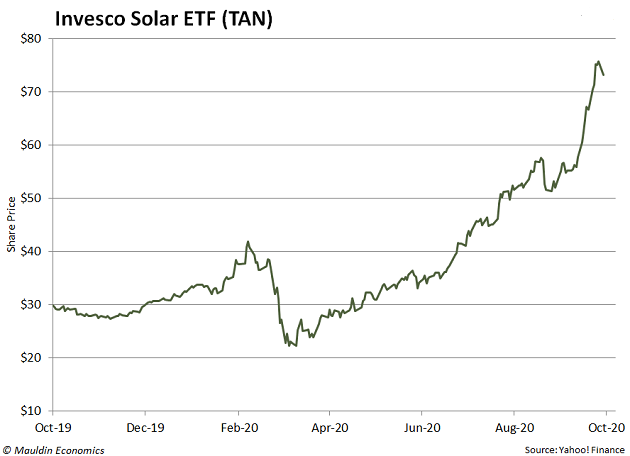

In a similar vein, are solar companies genuinely worth 90% more than they were before the pandemic hit in earnest? Granted, hopping on the TAN express with the expectation of a Biden victory may have been a fabulous momentum decision. On the flip side, TAN’s aggregate P/E also pushes a 40 handle. It’s hard to envision a 10-year period where that kind of P/E multiple is sustainable.

(There may be a place for green energy in your portfolio. Just don’t be shocked by a consequential sell-off in your favorite ETF — one that requires years to recover.)

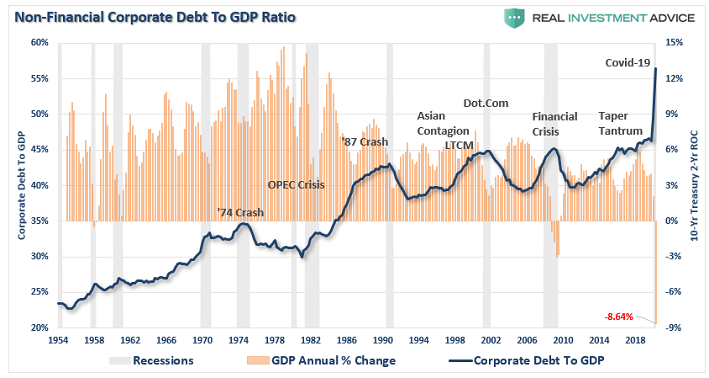

In truth, companies have never been so indebted. And not just to their bondholders. They are now slaves to a zero percent rate paradigm that the Federal Reserve must maintain indefinitely (if not forever).

Notice that in the three previous recessions, companies reduced their debt-to-GDP levels. In fact, every time that the percentage approached 45%, it marked a peak in the borrowing cycle.

Not in the coronavirus recession. The Non-Financial Corporate Debt to GDP ratio catapulted up to 55%!

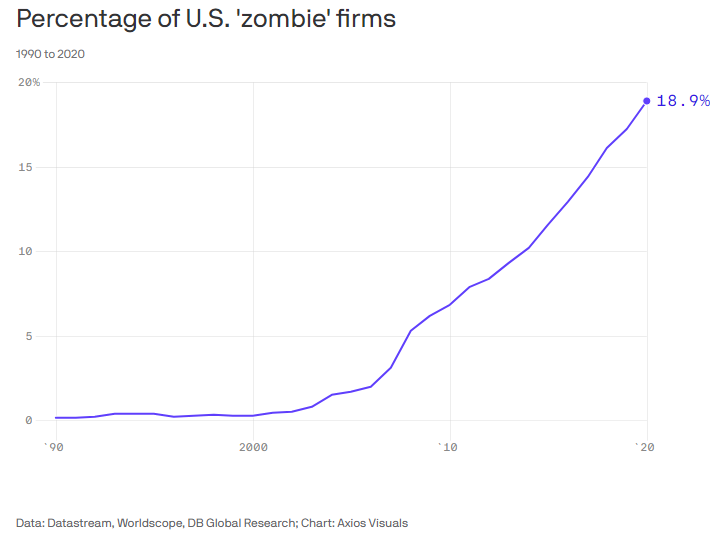

Investors may only be seeing the bright side of ultra-low interest rates. Do they tend to inflate stock prices? Sure. Yet negligible borrowing costs can also leave the financial system more vulnerable to overleveraged entities, some of which should fail, but are foolishly being kept alive.

In what situation is it better to have nearly one-fifth of your companies with higher debt servicing costs than profits? Zombie corporations are those that the Fed is keeping alive for a little longer, even though the ‘walking dead’ die soon enough.

Going forward, is it likely that overleveraged corporations will be able thrive? Some won’t even be able to survive. That won’t be good for employment. And it sure as heck won’t be good for stock prices, even if Federal Reserve gamesmanship has convinced market participants otherwise.

Would you like to receive our weekly newsletter on the stock bubble? Click here.