Many people assume that “stocks” have been a great investment over the last year. Few realize that the gains have primarily been confined to the U.S. large-cap space.

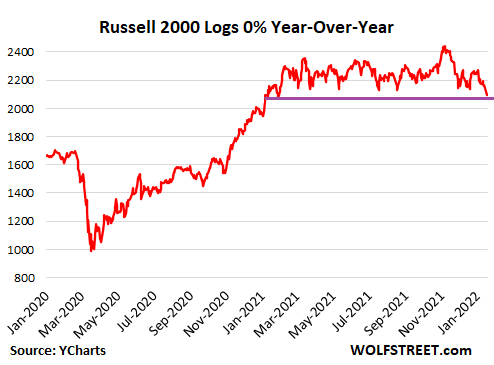

Smaller company stocks represented by the Russell 2000 have gone absolutely nowhere over the last 12 months.

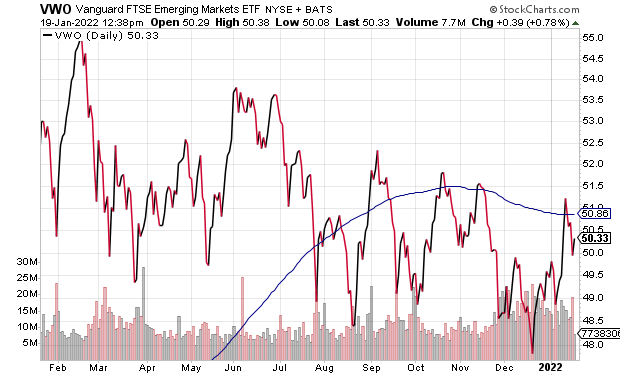

In a similar vein, international stocks in developed market indexes have flatlined since May of 2021. Meanwhile, emerging market equities have experienced nothing but losses.

More recently, of course, large-cap U.S. stocks have been “correcting.” The Nasdaq has witnessed a 10% pullback from its highs; the S&P 500 has given up as much as 5% from a record peak.

Is the price movement yet another buying opportunity? Maybe not.

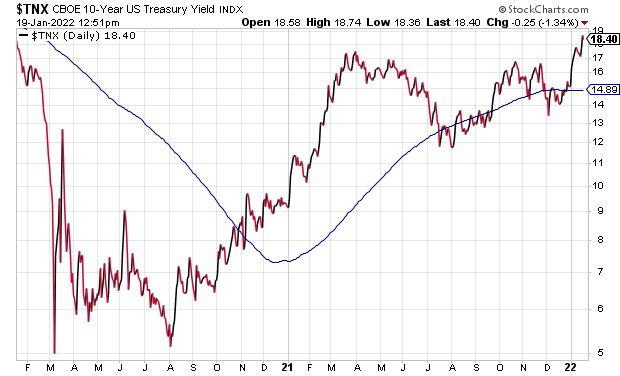

Large-cap stock excitement has been a function of ultra-low interest rates, federal government stimulus, and Federal Reserve money printing. Now, however, the Fed has entered a tightening phase to battle inflation. Not only have the decision makers at the central bank decided to terminate digital money creation to buy bonds, but they will raise overnight lending rates.

The result? Borrowing costs are now quite similar to what they were before the pandemic.

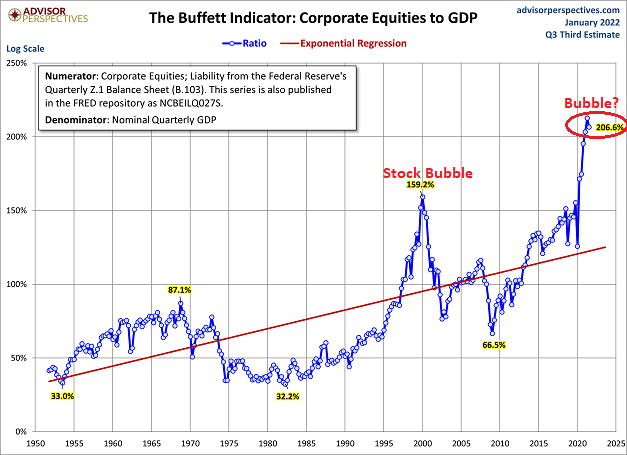

Borrowing costs may be the same as two years ago, but stocks and real estate are dramatically higher. Why would large-cap stock investors be comfortable with borrowing costs that may continue to climb? At hyper-valuation levels that rival the stock bubble of 2000?

CEOs and corporate insiders of S&P 500 companies have already backed away. Rare is the case when insider buying activity has been this depressed.

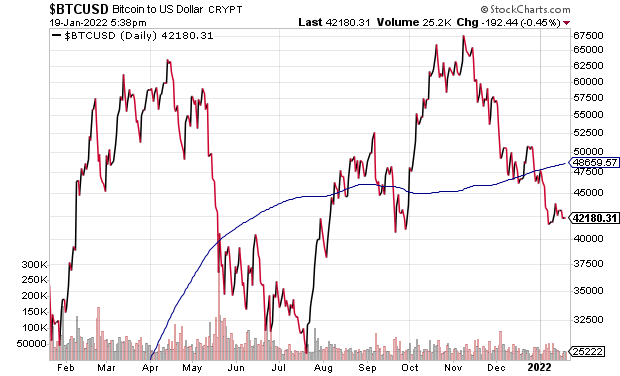

Other speculative assets like bitcoin have fallen on harder times as well. The popular crypto has given up 40% since November.

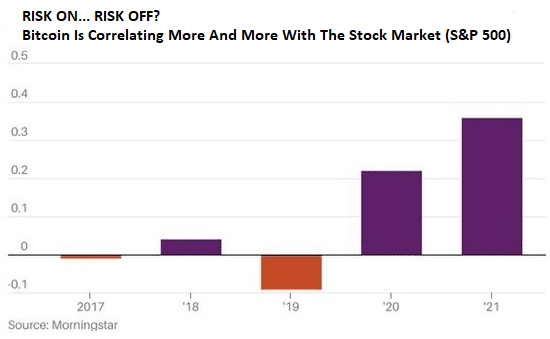

Granted, buying the proverbial dip in crypto might favor the bold. On the other hand, bitcoin is a speculative asset that increasingly moves in the same direction as the S&P 500. And that may spell trouble for risk taking in January of 2022.

Would you like to receive our weekly newsletter on the stock bubble? Click here.