Corporate debt downgrades are accelerating. The three-week tally for unemployment claims hit 17 million (4/9/20). And annual rate estimates for 2nd quarter GDP are circling around -30%.

Yet the data points have not stopped the Federal Reserve’s resolve to reflate the 2020 stock bubble.

Its latest move? A decision to buy junk bond ETFs like Blackrock’s iShares iBoxx High Yield Corp Bond (HYG).

The Fed is already hoovering up Treasury bonds and mortgage-backed bonds with its money printing scheme. With the help of the U.S. Treasury, it recently moved into municipal bonds as well as investment grade corporate bond ETFs like Blackrock’s iShares Short Maturity Bond ETF (NEAR).

Yet the latest decision to enter the world of junk debt is a bona fide game changer. For one thing, it makes sure that “fallen angels” that fell from the investment grade ranks will not be overwhelmed by exceedingly high borrowing costs in junk-land. That will keep struggling companies and “zombies” afloat.

More notably, the willingness to acquire risky junk bonds signals to the investing world that the Fed would also buy stocks. No longer are they restricting themselves to Treasuries or quasi-government backed assets like munis and mortgages (a la the GSEs). And they’re not stopping at the high quality corporate credit door either. If the Fed would buy junk bond ETFs, they’d buy stock ETFs if they felt the need to do so.

So that’s it, then? There’s no more risk in the stock market because the Fed will backstop bearish declines? Not exactly.

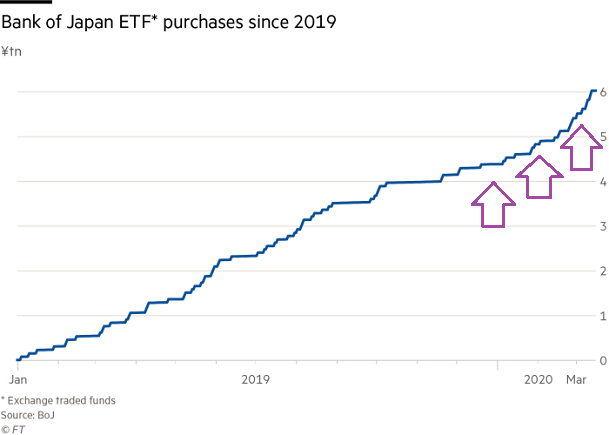

Japan has been buying stock ETFs for years. The Bank of Japan even picked up the pace as its equity markets struggled in 2020.

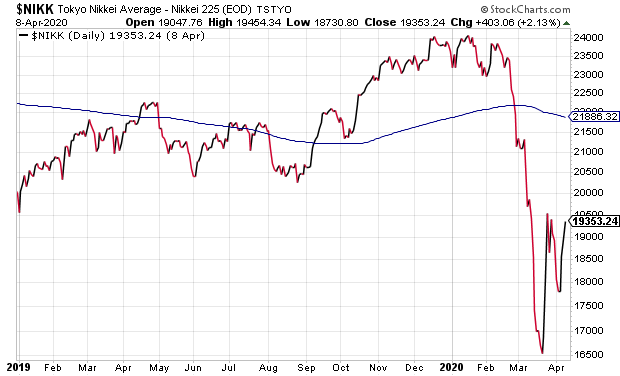

Nevertheless, the Nikkei 25 has still had its share of difficulties since the start of 2019.

In fact, the BOJ has been buying exchange traded funds for almost 10 years to stabilize markets and encourage investment. They’ve held rates at or below zero for about a decade as well.

Yet the policies did not prevent a 29% bear in the Nikkei in 2015 nor the recent 30% bear that has yet to find its ultimate direction. In other words, a central bank’s stock ETF purchasing schemes do not repeal risk of stock market participation. On the contrary. It may actually highlight the point at which a central bank has run out of kitchen sink ammunition.

Please click here if you’d like to receive our weekly newsletter.