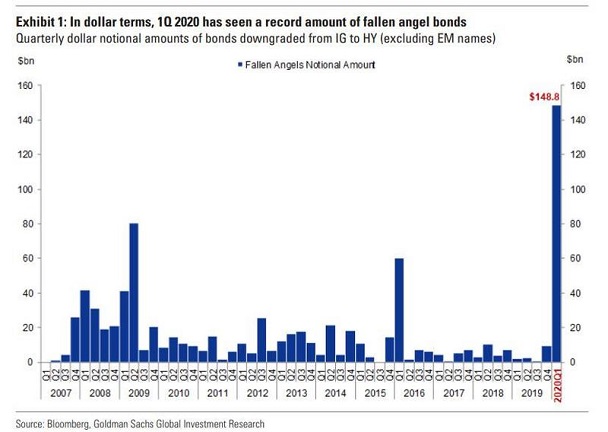

They call ’em, “Fallen Angels.” They’re bonds that the credit agencies demote from investment grade (IG) to high yield (HY).

Unfortunately, there’s nothing angelic about a wave of downgrades happening all at once. And that’s what transpires in recessions.

For example, in the first quarter of 2020 alone, $150 billion in “high quality” IG bonds have been re-rated as HY, or “junk.” Goldman Sachs analysts anticipate $550 billion more in fallen angel activity over the next two quarters, bringing the total to $700 billion.

Putting the tsunami into perspective, 10% of the IG universe must get dumped from pensions, mutual funds and investment grade bond ETFs. And it likely would not stop there.

BBB-rated debt already comprises one-half of the IG marketplace. Triple Bs can be deadly since they are only one notch above a double B junk rating. In other words, estimates on the downgrade wave are likely to be understated.

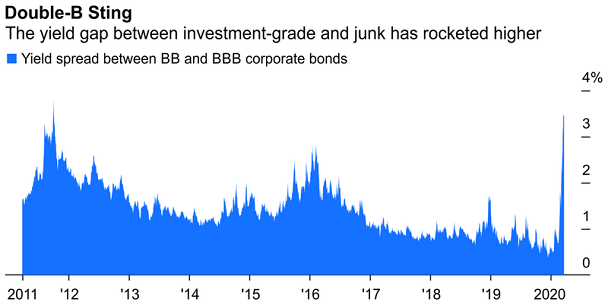

Recently, the yield spread between BB and BBB moved north of 300 basis points. Borrowing costs for fallen angel companies are literally skyrocketing. And there’s no telling if they will come back to earth quickly enough for these businesses.

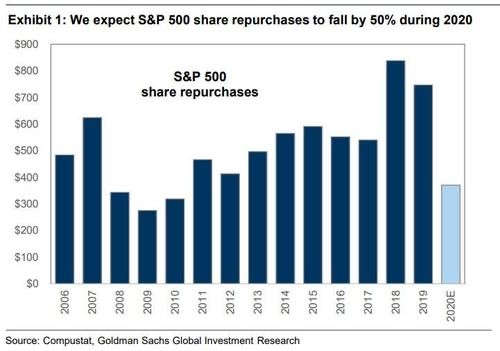

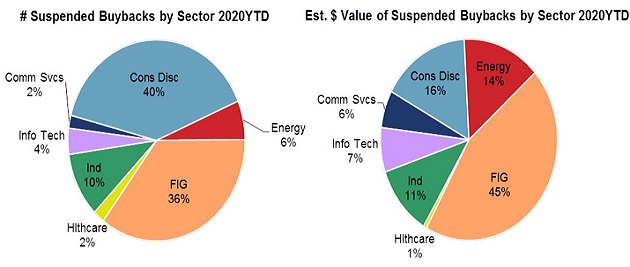

Bondholders are not the only ones who get hurt. Those companies looking to avoid dreaded downgrades scramble to shore up their balance sheets by slashing dividends, selling assets and suspending stock buyback programs. Those corporations that receive downgrades? Higher borrowing costs mean that there won’t be money for buybacks or dividends at all.

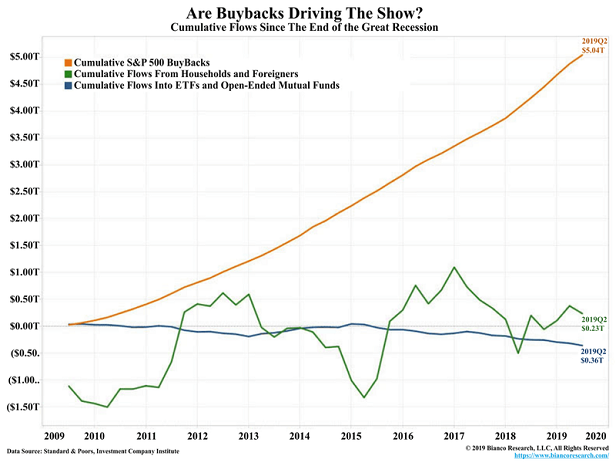

According to a recent article in the Wall Street Journal, corporate share buybacks added a net of $4 trillion to the U.S stock market since the start of 2009. Contributions from elsewhere? They net out to ZERO.

What that means is, since the end of the Great Recession, the only net buyers of stock were corporations. They borrowed in the debt markets to pump up their stock prices.

All the other sources? Insurers, mutual funds, broker dealers, pensions, hedge funds, foreign buyers, households? Net nada.

Now, however, the greatest source for stock demand is disappearing. According to Goldman Sachs, share buybacks will be cut in half in 2020. Meanwhile, others have identified a 75% suspension of buybacks for 2020.

Granted, the wind may be shifting in a favorable direction when it comes to flattening the COVID-19 curve. Hospitalizations in hot spots like New York have slowed. Meanwhile, new cases in Spain and Italy are falling.

However, the coronavirus impact is not about the number of new cases, hospitalizations, or deaths. The impact is about the longer-term effects of having shut down the world economy.

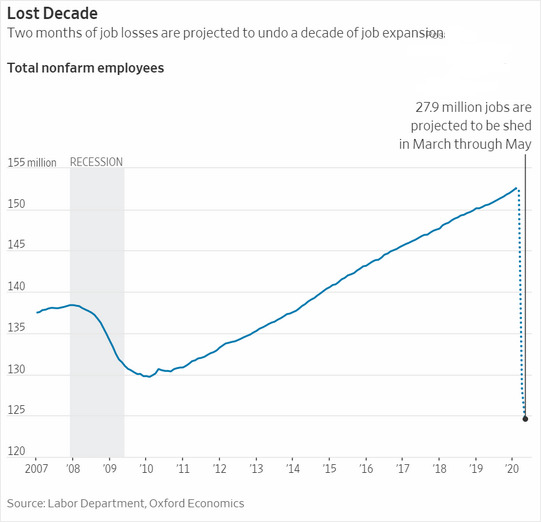

For example, having shut down the U.S. economy, 25-30 million jobs will be gone. That takes us all the way back to the Great Recession with unemployment rates higher than they were in the Great Recession.

“But the American consumer is resilient,” you say. The consumer is resilient when the consumer has a job.

Keep in mind, 78% live paycheck to paycheck. 50% of citizens do not have savings or retirement dollars. Many of these folks consume by adding to the revolving door of credit card debt.

It follows that slowing or containing the virus alone will not be enough to send the economy back to the top of the GDP mountain. Indeed, history shows that consumers take a while to spend in earnest after a pandemic, even as they begin returning from furloughs or finding new employment.

The reality for investment markets? This will continue to be an epic battle between unfortunate economic circumstances and unprecedented amounts of economic stimulus. And the primary winner of the battle in the near-term is intra-day price volatility.

On the stimulus side, stock bulls know that there has never been anything quite like it. Get a gander at what the Federal Reserve is throwing at the financial system:

- Indefinite zero percent rate policy (ZIRP)

- Open-ended and unlimited asset purchasing (a.k.a. quantitative easing or “QE”) for U.S. Treasuries, mortgage-backed bonds and investment grade corporate bonds

- The relaxation of regulatory constraints on banks

- Emergency funding facilities to “stabilize” markets

- Critical support for asset-backed securities like auto loans, credit card loans and Small Business Administration (SBA) loans

And that’s just the Fed!

Congress and the White House passed the CARES Act at a stimulus cost of $2.2 trillion. They’re already working on the next package with a prospective price tag of $1 trillion.

It seems clear that stimulus measures — electronic money printing, asset purchasing, favorable loan terms, trillions in additional government debts, trillions in deficits, bailouts, bail-ins, tax deals and so forth — they’re decidedly positive for investment portfolios. They are nearly certain to keep the stock market from experiencing a 90% price evisceration like the one that occurred in conjunction with the Great Depression. (Note: Longer-term concerns about the dollar as a viable currency or the country’s debt circumstances will need to be addressed at a future date.)

On the other hand, it’s difficult to look past valuation concerns entirely. On virtually every traditional indicator at the start of 2020, stocks were extremely overvalued.

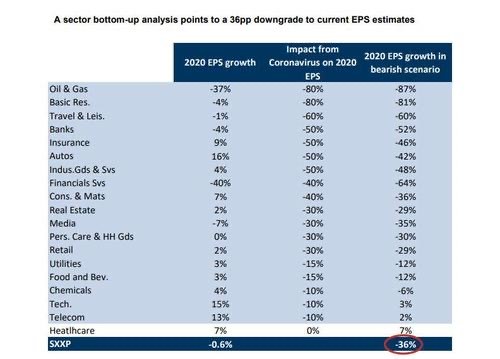

So what happens when earnings per share fall 36%? From the highest historical percentiles of stock valuations in history? Will investors simply ignore corporate reality and “follow the Fed?”

The S&P 500 at 2700-2725 trades roughly 19.5%-20% off an all-time high. That’s a lot of hope for a rapid-fire return to corporate well-being.

Long-time readers know that our investing process guided us to reduce our equity exposure for balanced clients from 60% large cap long down to 30% large cap… before the worst of the selling pressure. Later, where there was room to swap out index exposure in the SPDR S&P 500 (SPY) and Vanguard Total Stock Market (VTI), we nibbled on individual stocks that had fallen 35%-60% plus from their highs. Some of our wish list names included, but were not limited to Cisco (CSCO), AB InBev (BUD), Fortinet (FTNT), Exxon Mobil (XOM), Mastercard (MA) and Home Depot (HD).

That said, our net long stock exposure for balanced clients remains near our tactical target of 30%-33%.

There will be several opportunities to buy quality names at bargain prices over the course of the next six months. Chasing a bear market rally into a beehive after it has catapulted 20%-22% is likely to sting.

Said differently, the bear market will reward patience. Identify the names of stocks on your wish list. Then, wait for them to fall into your lap at prices that are likely to reward handsomely over the next five years.

I gave you some of mine above. Here are a few more: Caterpillar (CAT), Scotts Miracle-Gro Co (SMG), Square (SQ).

Not all of them will be winners simply because you acquire them 35%-60% off of their highs. Be prepared for the possibility that some companies get obliterated in the way that they did in 2000’s tech wreck. Use stop-limit loss orders or other methods for protection.

In the meantime, if you’re going to follow the Fed in your thirst to “buy, buy, buy,” follow them into direct areas of support. The Fed is directly backstopping municipal bonds, making iShares National Muni Bond (MUB) worthy. The central bank is directly buying mortgage-backed bonds, making iShares MBS ETF (MBB) an investable option. And, not to be outdone, short-term corporate bonds via Vanguard Short Term Corporate (VCSH) should provide you with a relatively safe yield.

Please click here if you’d like to receive our weekly newsletter.