The 2022 stock bubble is well-documented. Yet, what about the present-day real estate balloon?

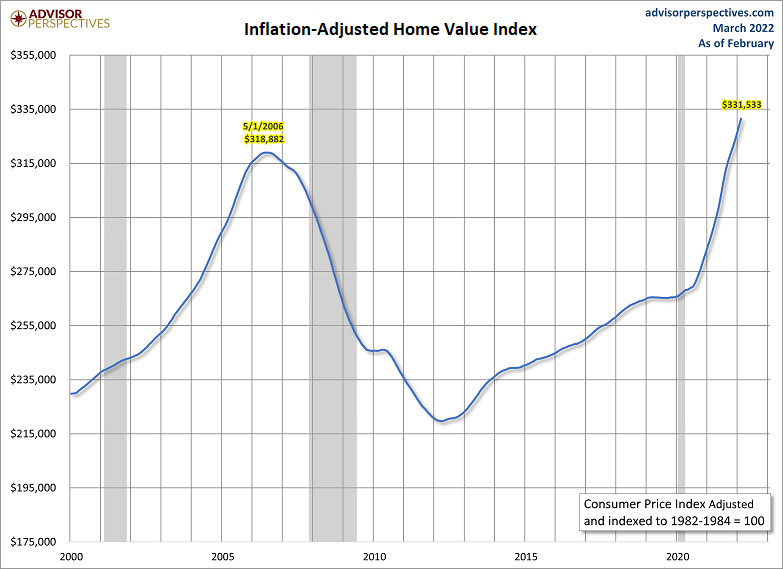

For instance, home prices are bounds and leaps beyond anything seen in the mid-2000s insanity. To make sense of the true dollars, however, one has to adjust for inflation.

Even when you adjust for inflation, home prices have never been higher than they are right now.

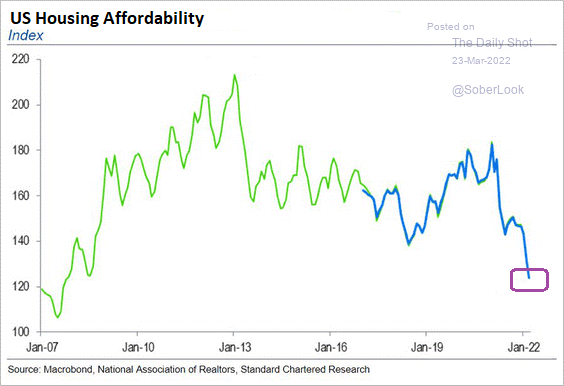

In and of itself, the highest inflation-adjusted prices for real estate would not a bubble make. What might? Affordability.

Back at the height of the mid-2000s housing stupidity, lenders gave money to people who could not afford the homes that they were buying. That recklessness (e.g., subprime mortgages, negative amortization loans, no-documentation loans, etc.) led to a complete breakdown in the financial system.

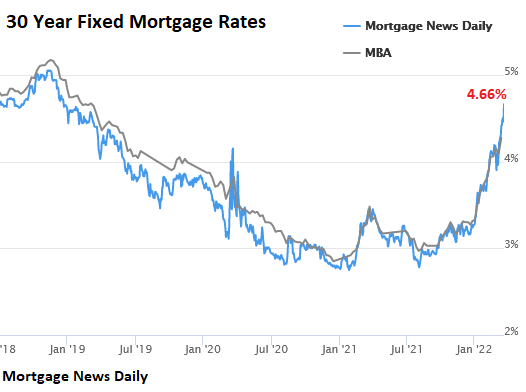

Today’s financial institutions are more cognizant when it comes to approving mortgages. Still, with mortgage costs rising dramatically, and with residential home prices skyrocketing, affordability is nearly as bleak as it was before the mid-2000s real estate bubble popped.

What makes the current situation particularly precarious is that the Fed appears resolute in a desire to push borrowing costs upward. That’s how they are fighting inflation… by destroying demand.

Putting the facts into perspective, home prices are currently 30% higher than they were three years ago. Yet mortgage costs are roughly back to where they were three years prior. That makes it exceedingly difficult for prospective homebuyers to qualify.

And it shows.

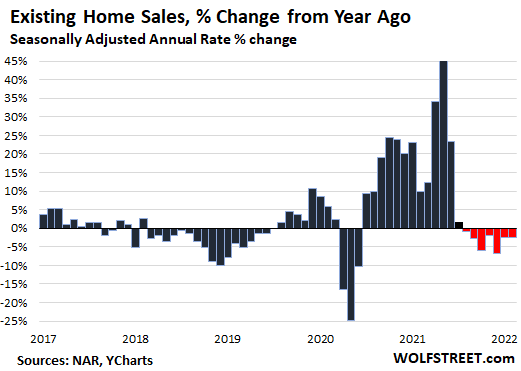

Already, on a year-over-year basis, existing home sales have fallen for seven consecutive months.

Okay. So residential real estate may have a few challenges going forward. Is this really the same for the U.S. stock market?

Consider the reality that when the real estate bubble popped in 2007, the stock market logged -57% from 10/07-3/09. It took roughly 4 1/2 years… just for stocks to break even.

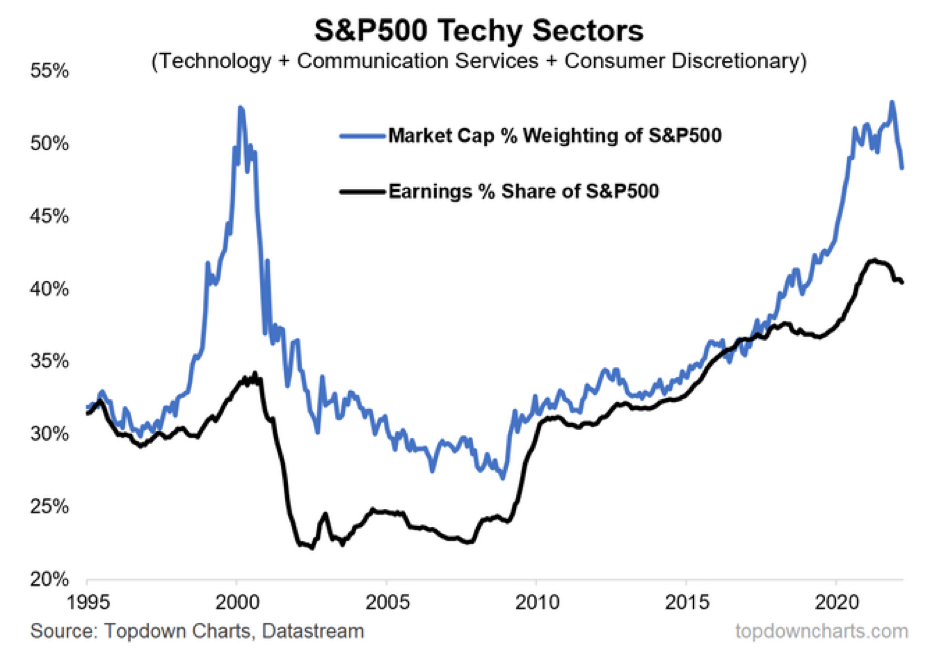

Equally worthy of note, the Fed’s intention to raise borrowing costs substantially to fight inflation has an adverse impact on corporate earnings. With the S&P 500 largely devoted to “growthy” or “techy” sectors — Communication Services, Technology, Consumer Discretionary — prices of those stocks may need to reverse course to meet up with the Earnings Per Share (EPS).

And then there’s this: Ultra-low interest rates supposedly justified exceedingly high stock valuations in the latter half of the 2010s. The idea had some of its roots in the notion that cheaper borrowing costs boost bottom-line earnings.

Although I do not subscribe to the explanation, let’s assume that it is true. Ultra-low rates support the “E” in P/E, making it possible for stock valuations to rocket into the stratosphere.

With rates zooming higher, with the Fed determined to keep hiking them, how can folks suggest that this too is bullish for stocks? If ultra-low rates and slow/modest economic growth were bullish for record valuation (P/E) peaks, how can higher interest rates, a stagnating economy, and inflation be beneficial as well?

They can’t.

Bottom line? Balance sheet reduction (a.k.a. “quantitative tightening” or “QT”) alongside higher borrowing costs will eventually rupture the 2022 stock bubble.

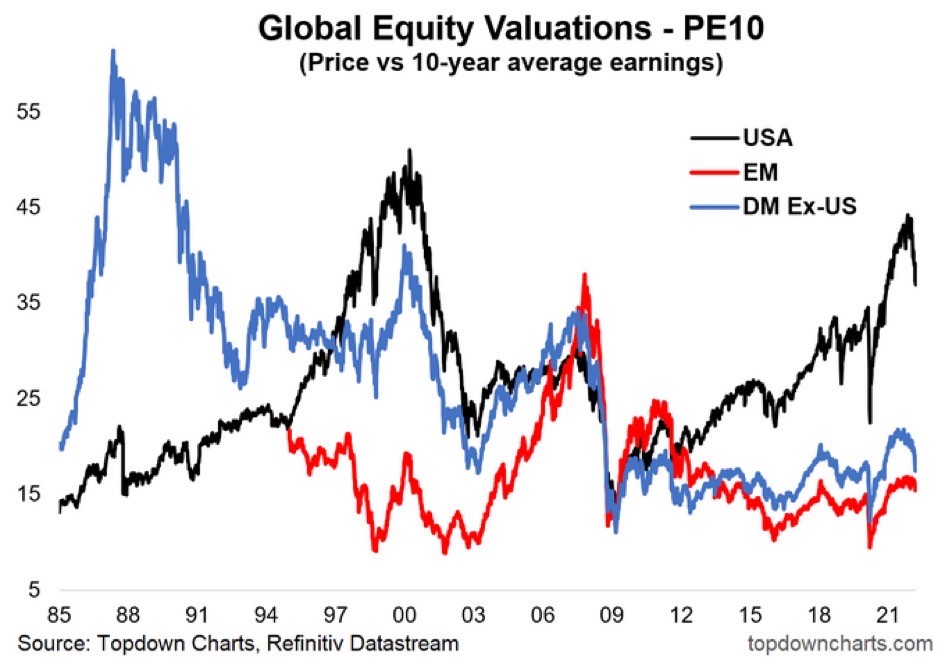

It follows that oversubscribed and overvalued U.S. equities will come down the way they did in the 2000-2002 stock bear. Judging by the extraordinary gap between U.S. valuations and foreign stocks (e.g., developed foreign markets, emerging markets, etc.), the realignment could be brutal.

Would you like to receive our weekly newsletter on the stock bubble? Click here.