Many folks wonder why the Federal Reserve needs to be so aggressive with interest rate hikes. After all, 30-year fixed mortgages have topped 5%, making it nearly impossible for homebuyers to qualify.

The primary way for a central bank to beat back inflation is to increase borrowing costs. Specifically, the Fed reduces demand by curbing the appetite for credit.

The risk? Demand is whacked so hard that the country finds its economy shrinking.

Granted, Fed Chair Powell has explicitly stated that the goal is to tame inflation without causing a recession. Yet pressures may already be building.

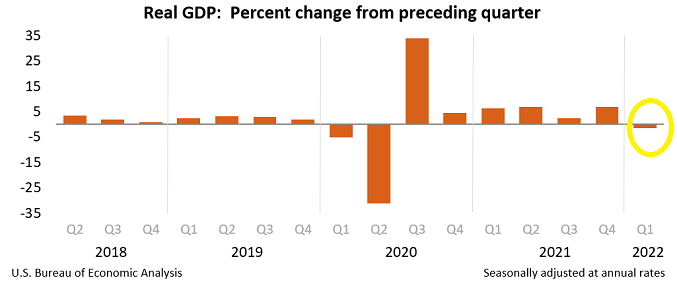

Consider the first quarter of 2022. Gross domestic product (GDP) registered -1.4%.

The idea that the Fed can engineer a “soft economic landing” may be fanciful. According to Rosenberg Research, the central bank has only achieved this aim in 3 out of 14 tightening cycles.

Tech stocks in the Nasdaq have already hit 20% bearish declines. Meanwhile, disruptor stocks in funds like Cathie Wood’s ARKK Innovation (e.g., Zoom ZM, Teledoc TDOC, Roku etc.) have plummeted like dot-com disasters from the 2000 stock bubble.

There’s more.

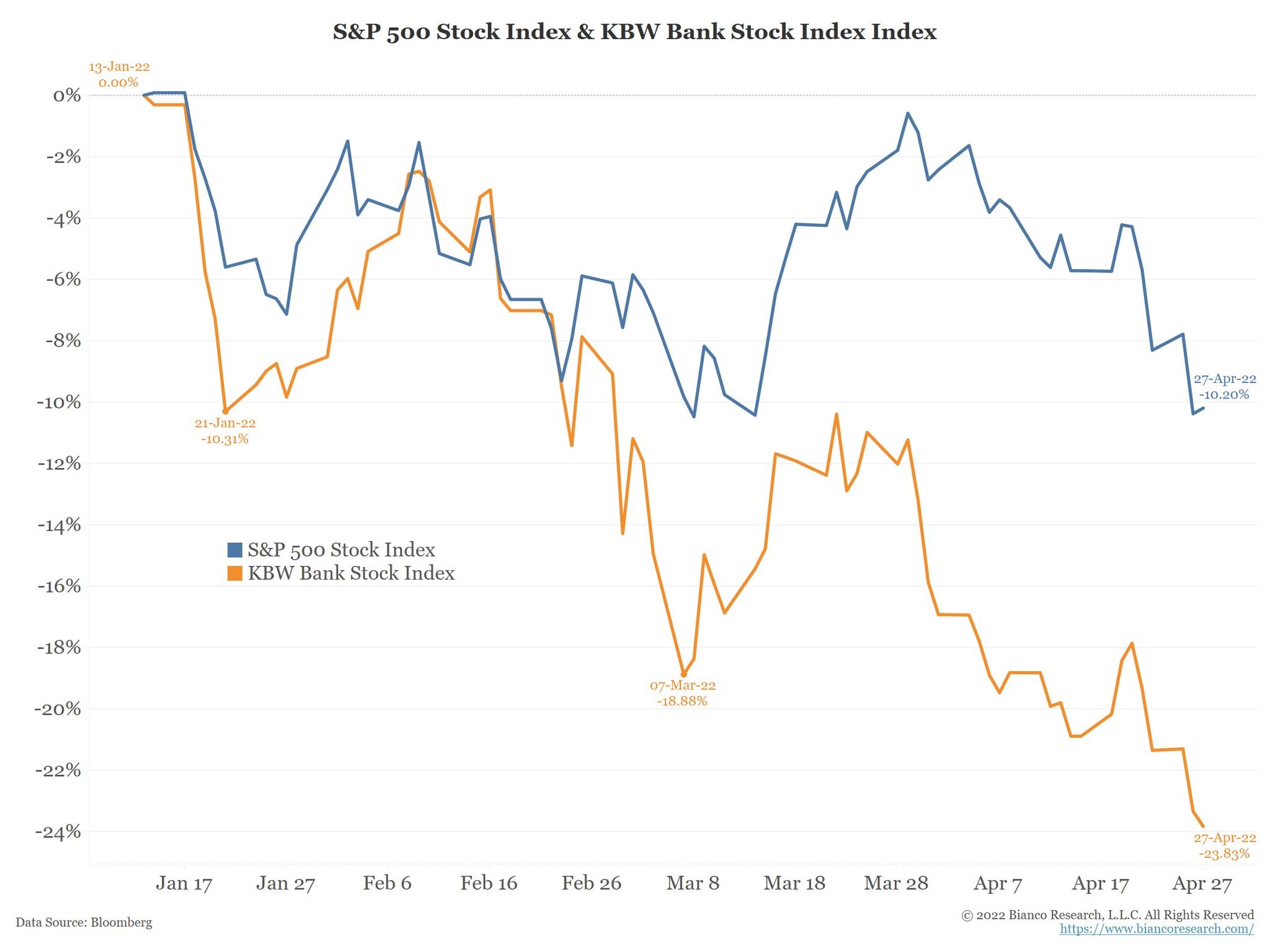

The entire bond market has already moved to the point where the Fed intends to go. And that means yields across the entire Treasury market are flatter than the queen of spades from a poker deck.

The implication for banks? There’s little to no money to be made when there’s no difference between borrowing for 0-1 years and lending for 5-30.

Bank stocks have been getting slammed.

In a similar vein, rate-sensitive homebuilders have been eviscerated.

Throughout the 2010s and for the better part of the 2020s, Wall Street bulls enthusiastically exclaimed that stocks were the only game in town. With interest rates so low, they said, “There is no alternative!” (TINA).

Today? The 10-year Treasury bond provides a far superior yield to the S&P 500’s dividend.

It’s not that investors should be salivating over a risk-free 3% return. On the other hand, the Fed will inevitably revisit zero-percent rate policy in a recession. When it does, the iShares 7-10 Year Treasury Bond ETF may very well garner 25%-plus in total return.

Would you like to receive our weekly newsletter on the stock bubble? Click here.