Do you ever wonder why bad economic news seems to send stocks higher?

For example, industrial production is growing at a slower pace than anticipated. Ditto for manufacturing. Yet stocks seemed to rally on the news.

Simply put, poor economic data helps share prices move higher because it implies that the Federal Reserve will provide stimulus (a.k.a. “liquidity”) for a longer period of time. Conversely, the stronger the economic numbers, the more likely the Fed will follow through on reducing its money printing activity (a.k.a. “tapering.”)

Is this ass-backwards? Undoubtedly.

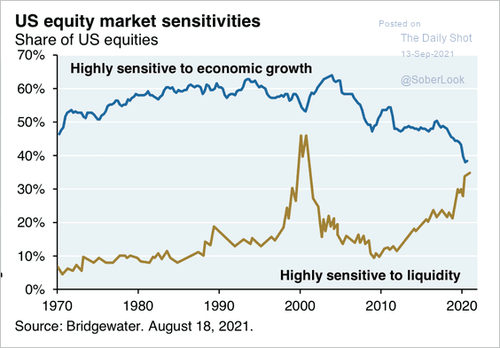

In fact, shares have nave not been this disdainful of economic growth in at least 50 years. In a similar vein, stocks have not been this sensitive to Fed liquidity since the tech wreck in 2000.

Unfortunately, Fed decision-makers may not have the luxury of providing unchecked liquidity much longer. Why not?

Inflation is likely to force their hands.

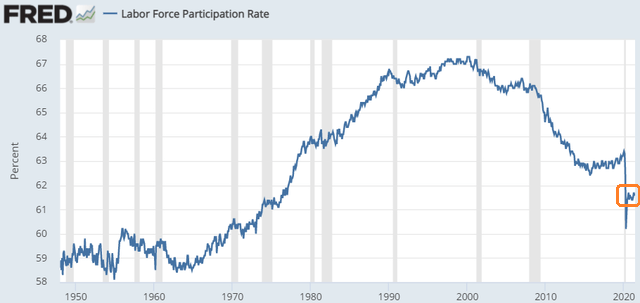

Softer monthly data notwithstanding, millions and millions of workers do not appear to be returning to the labor force. The pandemic seems to have inspired a worker shortage to go along with supply chain disruptions. Both are inflationary.

The Fed’s dilemma? Well, the primary way to battle inflation is to reduce stimulus. Not only by tapering that would reduce the bond acquisitions, but by eventually raising the overnight lending rate.

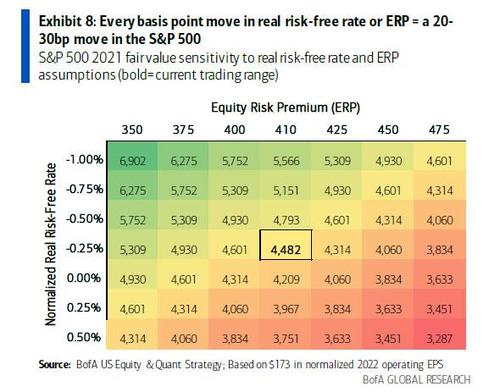

It follows that, absent an extremely robust economy to offset eventual Fed tightening, higher rates could send stocks lower. Maybe a lot lower.

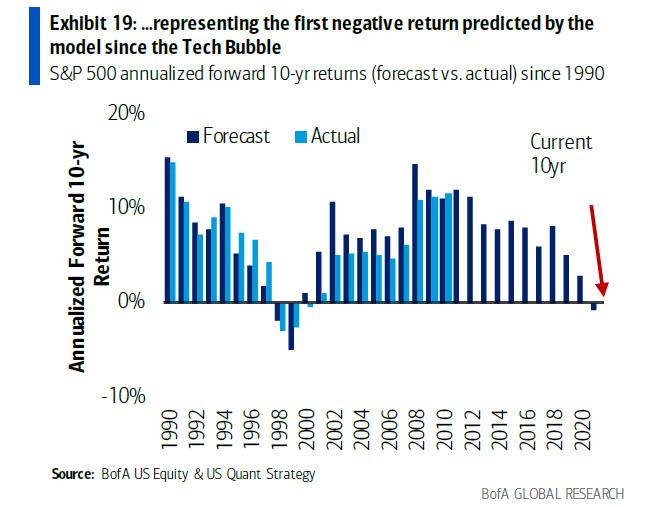

Bear in mind, the S&P 500 has been serving up an astronomical price-to-normalized-earnings ratio (PE) of 29. On a forward 10-year return basis, this valuation metric is suggesting that 10-year annualized returns will clock in at -0.8%.

You read that right. Negative returns for hold-n-hopers over the coming decade.

Of course, there are those who believe that the U.S. can print money indefinitely and issue government debt indefinitely with no adverse consequences. It is difficult to take these folks seriously.

What about those who do see the eventuality of negative consequences? Many of them feel that that there’s little reason to fret about today’s asset prices when authorities are kicking the can way out into the distant future.

Despite historical evidence to the contrary, despite participating in the greatest speculative bubble of all time, the bubble might not burst. There are no rules about when a bubble must pop. Perhaps this one can continue 20, 30, or even 100 more years.

Then again, this hyper-valued bubble is more likely to see multiple pin pricks than endless bliss. Any combination of items could cause a rupture. Inflation, stagflation, Fed tightening, higher taxation. Even hyper-valuation itself.

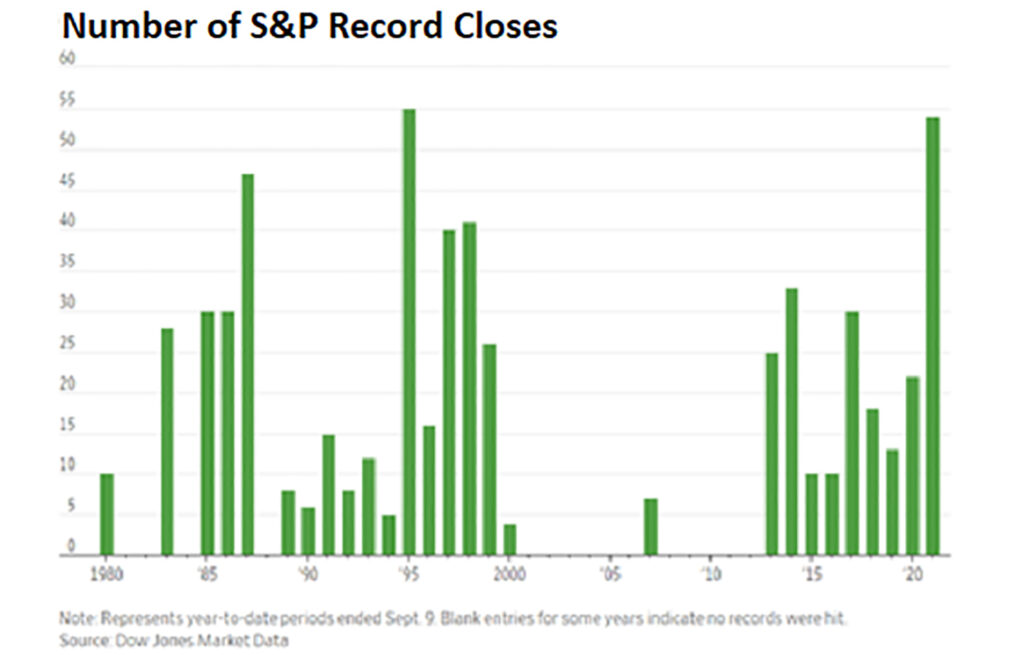

Granted, the investment community remains unfazed. The S&P 500 has set 54 all-time highs in 2021 alone.

Far be it from me to suggest that you should stop dancing in September. Then again, if you’ve been kicking your legs to the Charleston, now might be the time for a romantic waltz.

Would you like to receive our weekly newsletter on the stock bubble? Click here.