Consumers are already grappling with the highest inflation in 13 years. The Fed believes it is transitory, but when was the last time companies lowered employee wages after raising them? When is the last time service providers – restaurants, bike shops, accounting firms – lowered the price that you paid?

For inflation to subside, factories would have to ramp production back up in a very big way. Global lockdowns intended to slow COVID-19 led to significant supply chain woes as well as materials shortages. Semiconductor chips have been atop the list of hardest hit items.

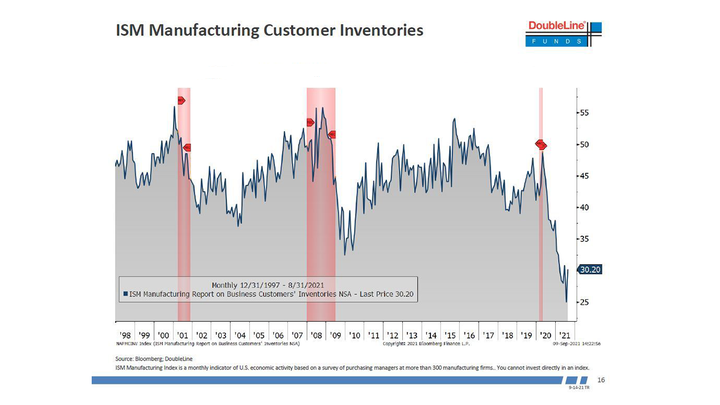

Will record-low inventories lead to persistently high inflation? They might. Retailers are already paying more for the scarce supply of merchandise and, ultimately, charging customers more for product.

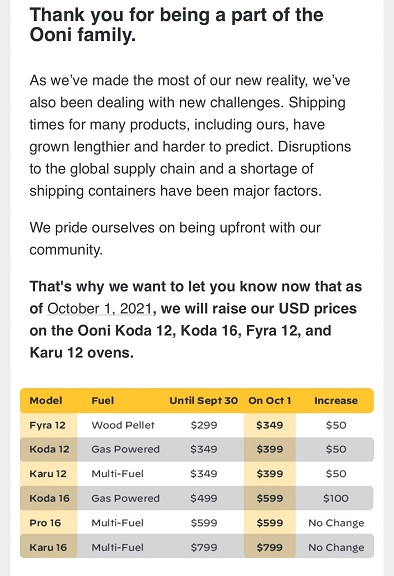

Consider pizza. If you have ordered delivery of the ever-popular treat, then you were likely stunned by the $30 price for a three-topping XL.

Some have responded to the high price at delivery chains by acquiring mini-pizza ovens. (The make-it-yourself pies are amazing!) Nevertheless, one of the top providers of these ovens recently apologized for needing to pass along higher prices to customers.

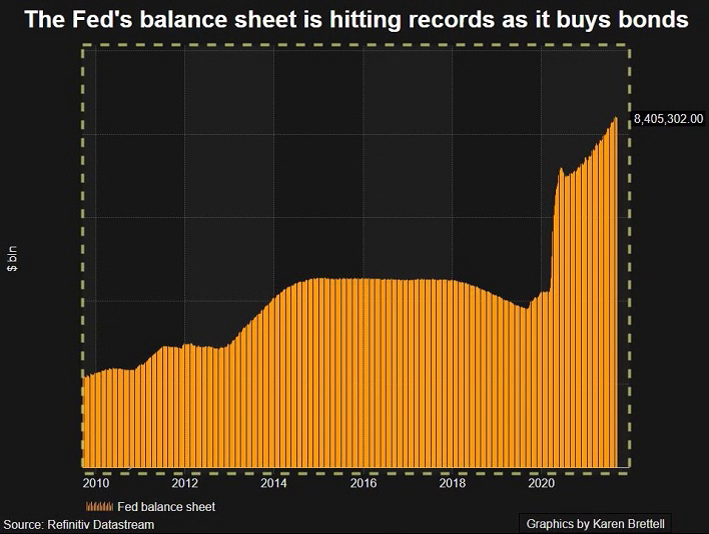

With the Federal Reserve continuing to increase the money supply at an exorbitant pace, the cash bubble gets directed toward a limited supply of stuff. Real estate, raw materials, pizza ovens. The higher prices mean that the purchasing power of dollars goes down.

Talking heads in the media tell us that the inflation caused by Fed money printing cements the need for you to continue acquiring non-cash assets, whether those assets are stocks, bonds, NFTs, crypto, or property. The money madness is part of the reason that Michael Burry described the circumstances as “…the greatest speculative bubble of all time in all things.”

Granted, inflationary pressures may make cash less attractive when the purchasing power is disintegrating before our eyes. And it may be pushing more money into the same limited investment opportunities.

On the other hand, the collective aversion to zero-percent yielding cash cannot support hyper-valued asset pricing indefinitely. When the investment community fears risk, the belief in the Federal Reserve backstop tends to fade. Similarly, hyper-valuation will suddenly matter again.

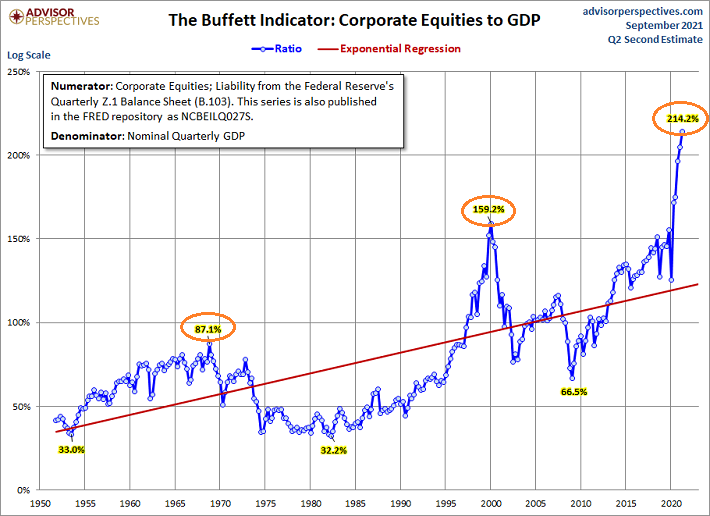

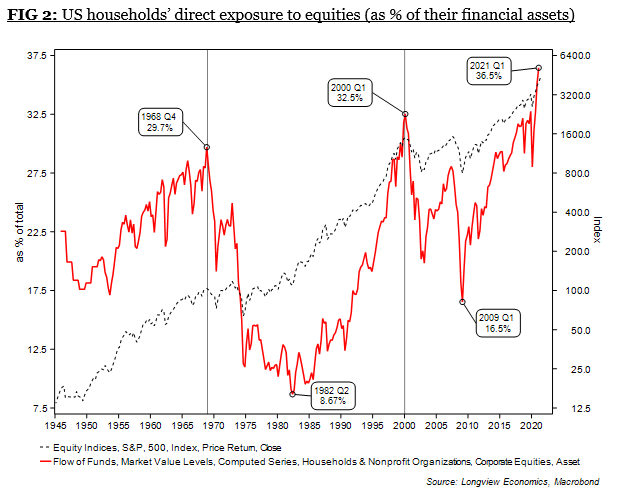

Perplexingly, investors have never placed greater faith in stocks. Allocation to equity has never been higher.

That didn’t work out particularly well in previous devastating bear markets. The 1969 bear erased 35% of stock wealth, while the 1973-1974 bear destroyed 50% of stock value. More notably, the 2000 tech wreck decimated 51% of the S&P 500 and three-quarters of the Nasdaq’s price.

Can the economy surge forward in Q4 as it comes out of a summer slowdown? Even if it is expected to, it may not be able to offset eventual Fed tightening and tapering of its money creating QE policies.

It is also worth noting that pandemic stimulus from the fiscal side (a la the federal government) made up as much as 40% of disposable personal income in Q2 2020. Those handouts are rapidly declining.

Absent government handouts, most Americans would find themselves increasing their debt burdens yet again, just to maintain consumption habits. Otherwise, they’d be consuming less.

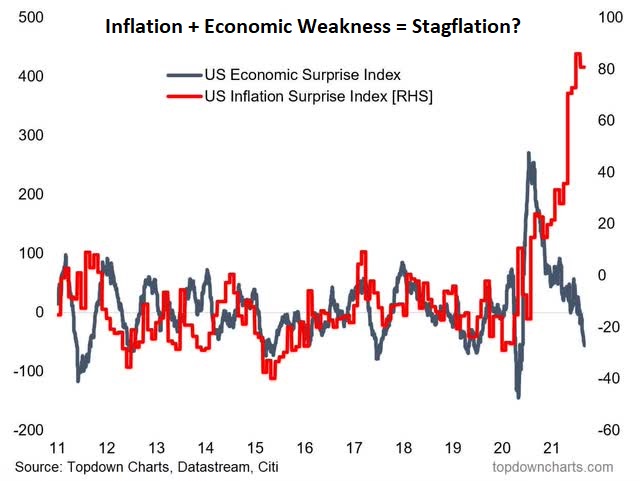

Less consumption? Higher inflation? There’s a word for a period of high inflation and stagnant economic growth. Stagflation.

Let’s face it. No matter how economic growth stagnates, central banks like the Fed would prefer to let inflation run amuck rather than fight it. Inflation reduces the real value of obscene debt ratios that governments carry. What’s more, by ignoring inflationary pressures with never-ending monetary stimulus, financial markets might not crash. (At least not in the near term with faith in fiat currencies as well as the Fed.)

In truth, the Fed is looking for any excuse to avoid upsetting stock and bond markets. They will not commit to slowing the $120 billion in money printing activity, only stating that “a moderation in the pace of asset purchases may soon be warranted.” Even more behind the curve? The Fed is not likely to raise overnight lending rates off the 0%-0.25% range until the end of 2022 or, more likely, somewhere in 2023.

The Fed is neither committed to battling inflation per their dual mandate, nor will decision-makers at the institution be able to increase stimulus. Similarly, the federal government is coming to the end of its COVID-related government handouts, and that implies that economic conditions will slow.

Are you prepared for an economy that’s about to go stag?

Would you like to receive our weekly newsletter on the stock bubble? Click here.