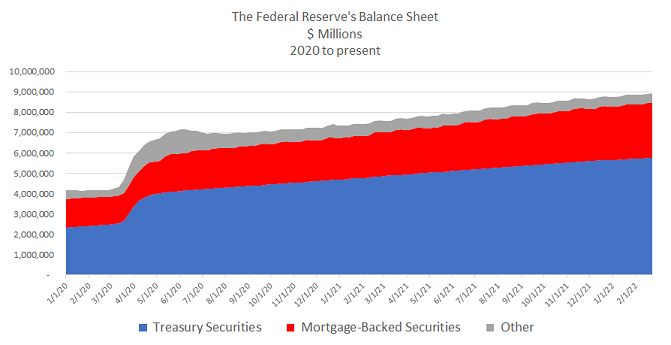

The Federal Reserve added $5 trillion to its balance sheet to battle the Covid-19 pandemic. That’s a whole lot of digital money creation in a matter of months.

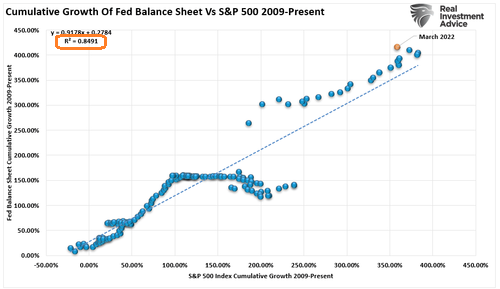

In actuality, the Fed started to print money digitally to manage the fallout from 2008’s financial crisis. They call it “quantitative easing” or “QE.” And the policy shows an 85% correlation with S&P 500 stock prices.

In other words, for 13 1/3 years, Federal Reserve QE has accounted for 85% of the stock market’s movement. That’s downright remarkable.

Think about it.

If the Fed is printing dollars to buy bonds (e.g., Treasuries, mortgage-backed, investment grade corporates, junk, etc.), the stock market is moving higher. If the Fed is neutral and/or reducing its balance sheet, stocks struggle.

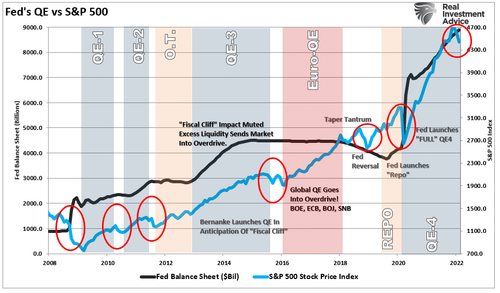

Indeed, virtually every pullback and sell-off since the systemic financial collapse of 2008 occurred when the Fed ended or nearly ended QE activity. (See the red ovals in Lance Roberts’ chart below.)

Throughout the 2010s, in fact, ultra-low interest rates represented the quintessential reason for acquiring stocks at any price. Valuations be damned. Of course, one of QE’s largest goals was to force borrowing costs downward.

Now, however, the Fed has terminated QE. And it is expected to reduce its balance sheet in the weeks and months ahead to push borrowing costs higher.

Why is the Fed expressing a determination to raise rates and potentially engage in quantitative tightening (QT)? It needs to battle inflation — a 1970’s style inflation caused by the Fed as it subsidized the federal government’s monstrous deficit spending.

The take-home? Since balance sheet expansion (QE)/ultra-low rates drove stocks to the moon, balance sheet reduction (QT)/higher borrowing costs will cause tremendous difficulties for stocks.

Granted, the S&P 500 has corrected 10%-12% already; the Nasdaq has already dropped 18%-21%. Essentially, Fed guidance on future policy, dramatically higher bond yields, and inflationary pressures are already making a mark. (The Russia invasion of Ukraine certainly did not help matters.)

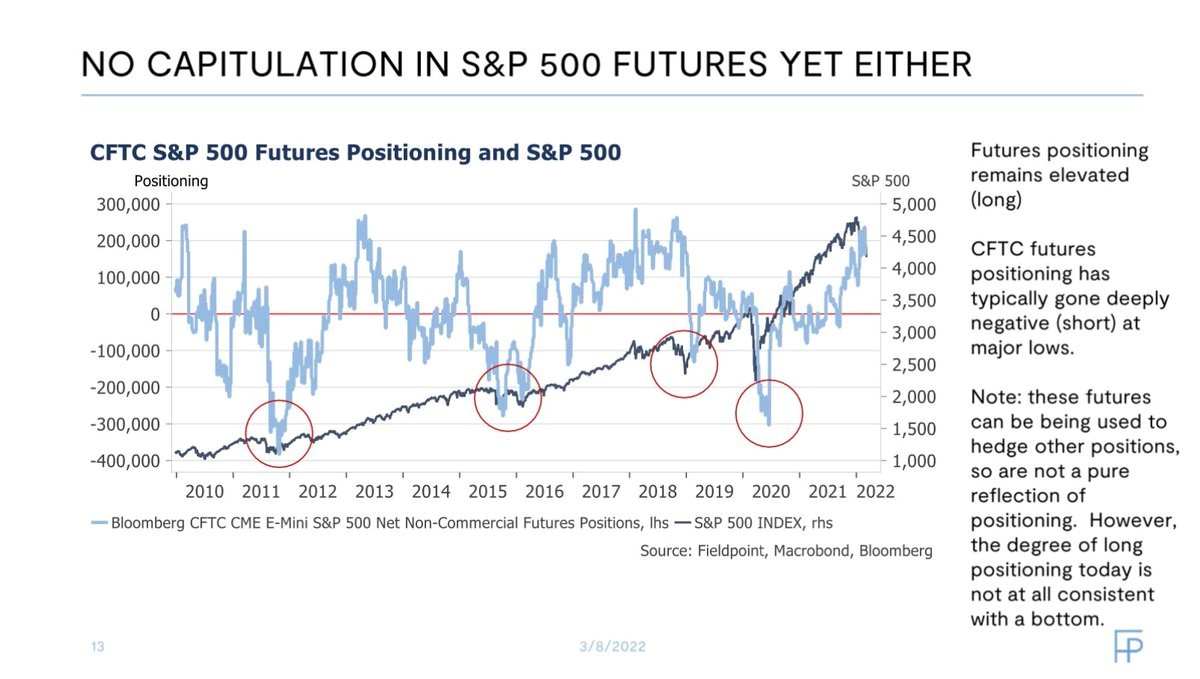

On the flip side, investors have not been bearish enough. Consider how the positioning of S&P 500 Futures often signal when a “bottom” for stocks is close at hand. Yet there is very little evidence of investor capitulation in the futures arena.

In a similar vein, previous stock bears involving oil concerns and inflation required 18-21 months to recover. And we are nowhere near the S&P descending 28%-48%.

There will be reflexive bounces and short covering. Bear market bounces are commonplace.

However, stocks are likely to falter without one of two things: (1) Fed stimulus/rate cuts/QE5 or, (2) An economy that is so resilient, its consumers and businesses can spend freely and ignore inflation entirely.

I don’t see it.

The economy is already cracking. Look at mortgage origination woes. Or look at the weakness in GDP projections.

More critically, the Fed is likely a long way from returning to rate cuts and QE. As long as they’re committed to reining inflation in, the stock train will sputter.

Would you like to receive our weekly newsletter on the stock bubble? Click here.