Ironic? Humorous? The stock bubble continues to hit high after record high, despite the economy showing definitive signs of weakness.

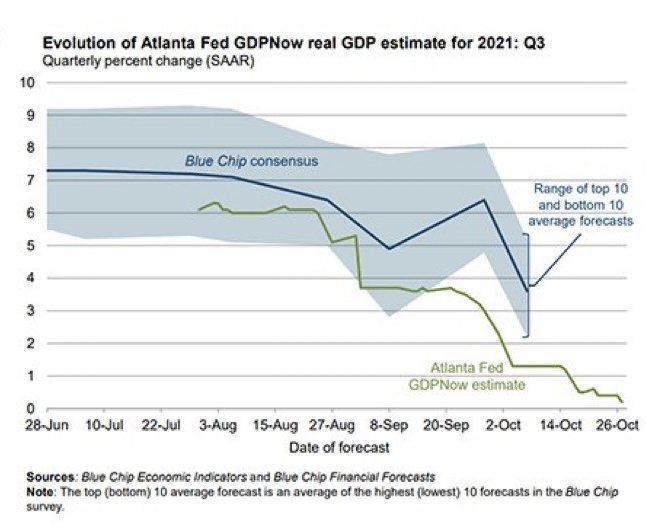

Two months earlier, the projection for the 3rd quarter period was 6.1%. Today? The Atlanta Fed is estimating growth of just 0.2%.

If investors have learned anything about the Federal Reserve it’s that the central bank is unlikely to do anything to upset the apple cart. In fact, the weaker the economy, the less likely the Fed is to taper its money printing and/or bond buying. Even if it begins tapering, it will do so at a slower pace.

What about the Fed’s plans to begin raising its overnight lending rate in the 2nd half of 2022? Members of the committee are more likely to let inflation take root than to take away the dual punch bowl of endless liquidity and ultra-low interest rates.

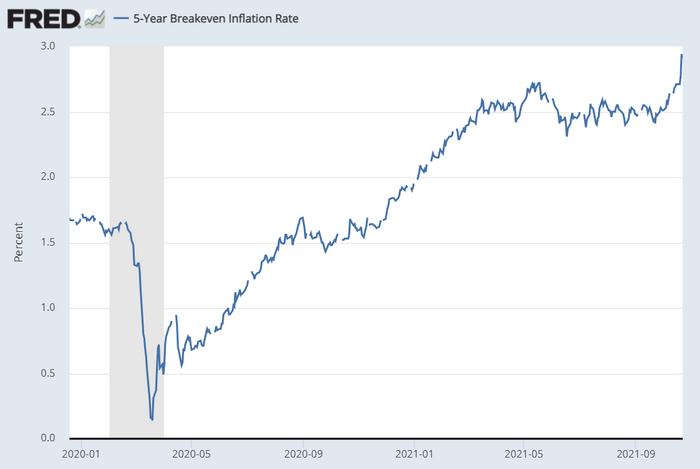

Speaking of inflation, the U.S. bond market is predicting that inflation over the next five years will average 2.91%. That’s the highest figure in the 21st century.

Obviously, the Fed would like to avoid popping the stock bubble. Forcing rates higher might very well do that.

On the flip side, can the central bank afford to let inflation destroy people’s purchasing power? Voting members at the Fed risk doing so by maintaining emergency level stimulus for too long.

The endless monetary magic is still working on the stock bubble. However, the magic may be running out of juice on broader economic well-being.

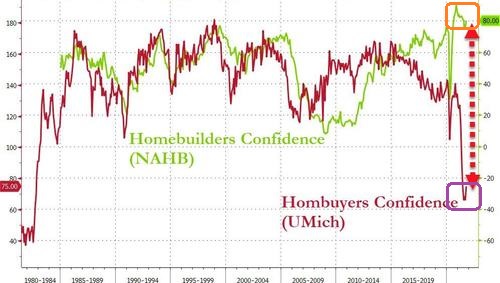

Consider the average priced home. In August of 2020, ultra-low interest rates made $380,000 homes more affordable. But by August of 2021? When the average U.S. residence sells for $440,000? Even if the 30-year fixed manages to stay around the 3% level (down from the 4% level prior to the pandemic), price gains may not be feasible going forward.

There’s more.

Entities like real estate trusts and yield-seeking funds have been hoovering up properties. They’re acquiring 25% of the homes with the intention of renting them.

That may or may not work out for investors in a REIT like American Homes For Rent (AMH). It may, however, exacerbate the gap between the “haves” and “have nots.”

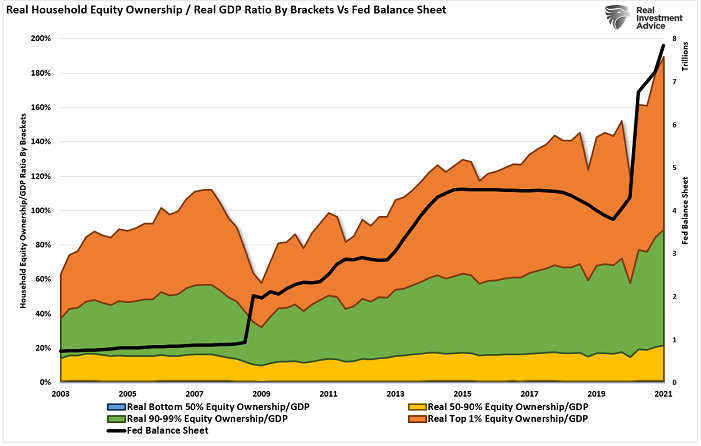

In the chart below, the black line represents the Fed’s money printing via quantitative easing (QE). There is a direct correlation between the Federal Reserve’s interventions and the folks whose net worth expanded the most. The top 1% (orange) as well as the top 10% (green) became significantly wealthier; they own most of the stocks. Everyone else has seen less benefit from the Fed’s digital money printing and rate manipulation.

One sure-fire way to close the wealth gap would be for the Fed to tackle inflation in earnest. Higher rates would likely send home prices lower and stock values lower. Meanwhile, reining inflation in would preserve the purchasing power of those whose well-being depends more upon a paycheck.

Then again, an asset-wide collapse (e.g., stocks, bonds, crypto, collectibles, real estate, etc.) would likely bring about a recession. If the contraction is bad enough, layoffs would hurt employees more than executives.

These are the problems that the Fed wrestles with. And there are no easy answers.

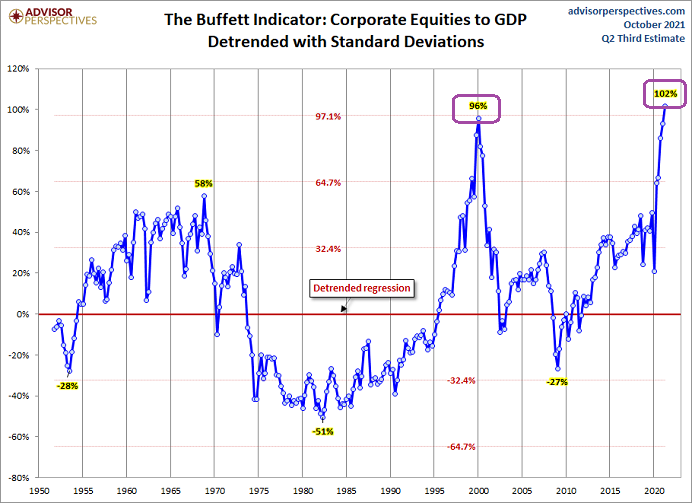

As for the stock bubble itself, some facts are scarier than others. Economic growth since the pre-pandemic highs has been flat. Corporate earnings for the S&P 500 have grown 14%. But the stock market’s price? A whopping 35% surge.

In essence, valuations have taken a back seat to Fed stimulus. Tried-and-true metrics across a century of data have been sidelined whereas Fed policy and liquidity injections have turned investors into frenetic speculators.

Perhaps unfortunately, too many of these folks have let their antipathy for zero-interest yielding cash override rational behavior. They forget that risk aversion can come furious and fast, wiping out huge dollar amounts in a blink of an eye.

Similar to the year 2000, the investment community may eventually witness 50% stock price evisceration. That’s what it would take to find ourselves back at the mean, or typical, market capitalization-to-GDP ratio.

Would you like to receive our weekly newsletter on the stock bubble? Click here.