An investor can look at return on equity (ROE) to determine how well a company is using its assets to generate profits. Additionally, one can calculate ROE by dividing net income by shareholder equity.

Is there a good ROE percentage? Acceptable ROE percentages tend to vary by industry. Nevertheless, the long-term average across the S&P 500 is roughly 14%.

(Note: Analysts deem 10% or lower as atrocious.)

In previous stock bubbles, when ROE began to drop at a rapid clip, the S&P 500 index followed suit. That’s not happening here in the 2020 stock bubble.

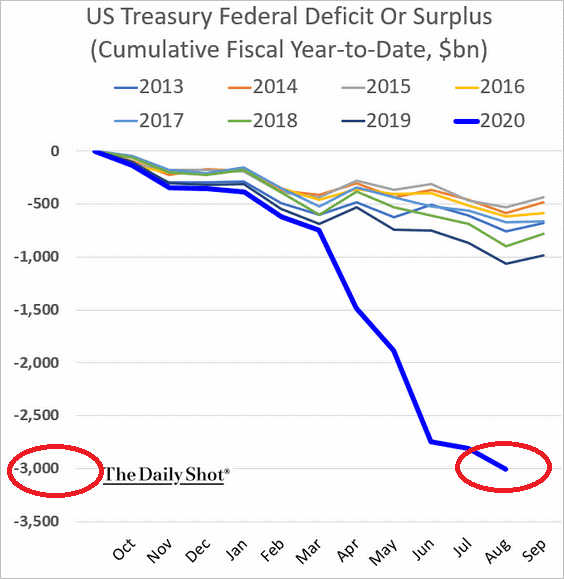

There are a variety of reasons for the disconnect. For one thing, the federal government is spending trillions of dollars it does not have to keep the consumption train moving forward.

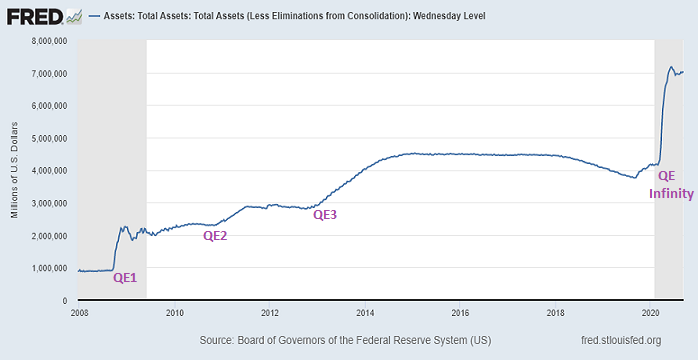

Meanwhile, the Federal Reserve is creating trillions of electronic dollar credits out of hazardous air to buy debt (e.g, muni, mortgage-backed, Treasury, IG corporate, junk corporate, etc.). Not only does the activity manipulate borrowing costs lower and eliminate opportunity for real yield, it bolsters risk appetite for stocks.

Indeed, trillions on top of trillions in dollar stimulus has worked wonders for the stock market. It’s worth noting, though, that the liquidity has primarily found its way into tech shares. The S&P 500 would be down on the year were it not for the influence of tech.

The choice(s) for market participants? Chase tech performance regardless of extreme overvaluation, rotate into areas of long suffering underachievement, or wait in zero-percent yielding cash for future opportunity.

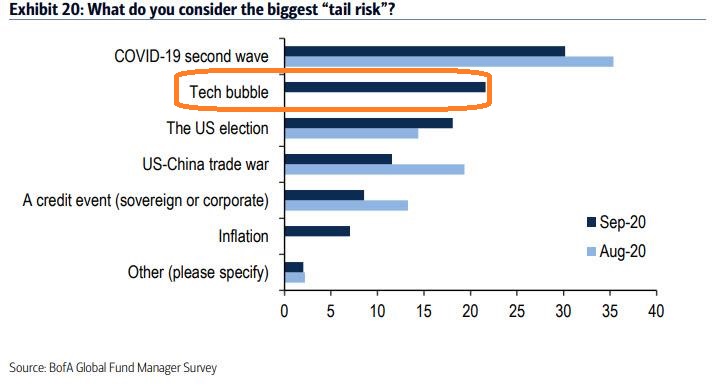

One thing’s for certain: Money managers have become exceptionally wary of the tech stock bubble. It’s not a question of if it will burst, but when.

Would you like to receive our weekly newsletter on the stock bubble? Click here.