Leading into 2020, the economy was growing at a modest pace (1.9%). By the end of the 2nd quarter, the economy will have recoiled at its quickest clip (-25%+) since the 1930s.

Similarly, at the start of the year, unemployment for working-aged individuals was 3.5%. By the end of Q2, the official unemployment rate may spike as high as 20%.

The economic facts are as disheartening as they are sobering. For example:

(1) Consumer confidence plummeted to a 47-year low

(2) U.S. retail sales dropped by the most ever in March

(3) Small business confidence dropped to a record low in April

(4) 84% of small firms will pay less than half their rent in May; 40% will skip rent altogether

(5) State budgets will rack up $100 billion in deficits in 2020

Deep recession. Depression. Whatever people wish to call it, yes… it is that dreadful.

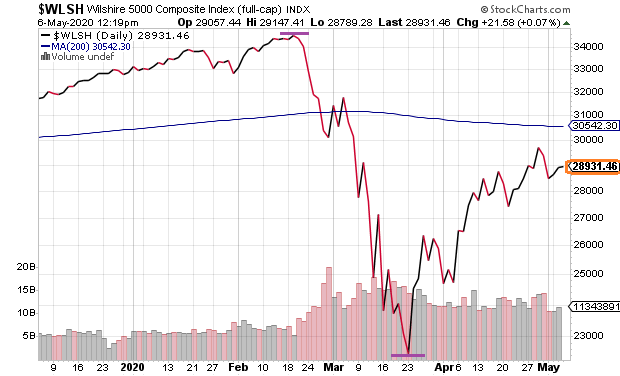

On the other hand, it has not been quite as bad for financial markets. U.S. stocks in the total market Wilshire 5000 Index are roughly halfway between their March lows and record highs from February.

Without question, there is a disconnect between U.S. stocks and the real economy.

Granted, there are those who optimistically tout the imminent reopening of states and businesses across the country. Yet, is it really the case that the post-virus economic environment will snap back quickly? Or is it far more likely that significant damage has been done to global supply chains and domestic demand across a wide range of industries (e.g., energy, transportation, manufacturing, hospitality/tourism, auto, sports/leisure, restaurants, basic materials, lending/insurance/financials, commercial real estate, brick-n-mortar retail, consumer discretionary, etc.).

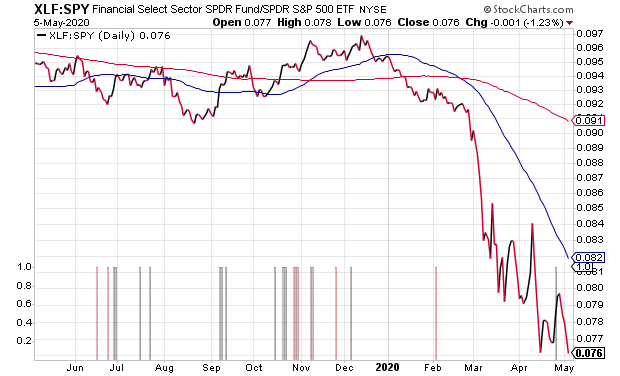

The financial system’s troubles alone should be enough for investors to recalibrate their economic expectations. The dramatic underperformance of the SPDR Financial Select Sector SPDR (XLF) relative to the S&P 500 SPDR Trust (SPY) here in 2020 bears a strong resemblance to the fallout in 2008.

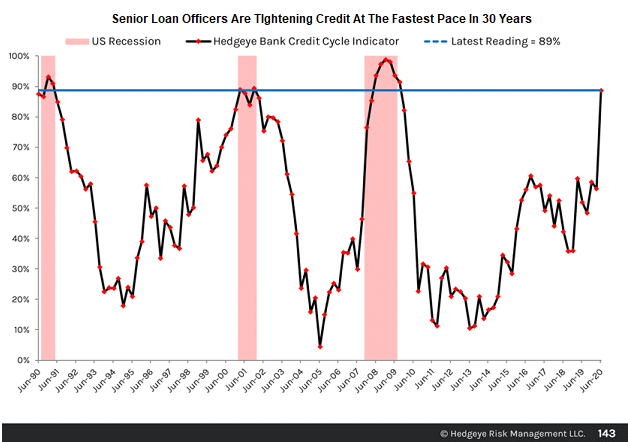

In particular, lenders and banks are tightening the reins. Not only are they hoarding more cash to deal with boat loads of toxic debts, but they’re less willing to extend credit.

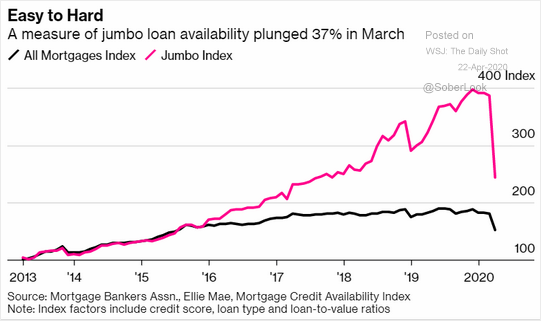

Not just to riskier businesses or families with borderline credit scores. Even wealthier folks are running into trouble securing jumbo mortgage loans.

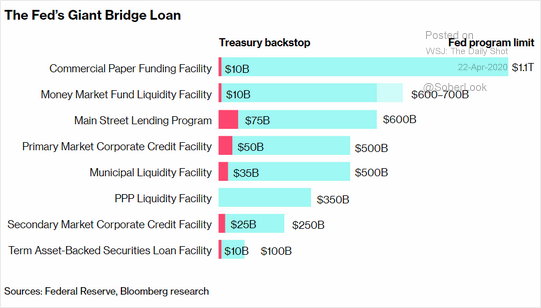

It should go without saying that a whole lot of those aforementioned economic segments — energy, transportation, manufacturing, hospitality/tourism, auto, sports/leisure, restaurants, basic materials, lending/insurance/financials, commercial real estate, brick-n-mortar retail, consumer discretionary — can only “get by” for a short while to make payroll and pay interest on debt obligations. That’s what the Fed’s programs are capable of achieving.

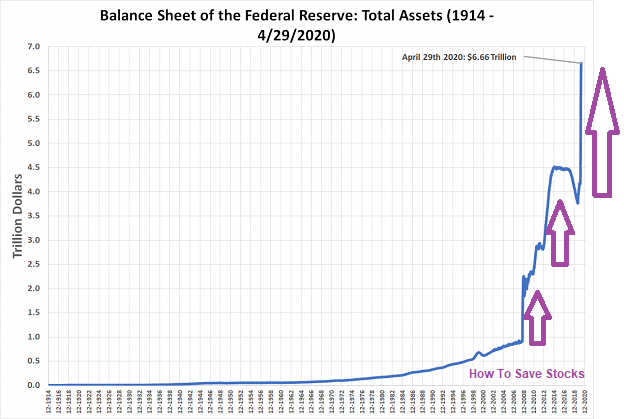

What’s more, in a world where central banks can toss trillions of dollars into the financial ring, the massive amount of monetary stimulus can backstop risk assets from investment grade bonds to “junk” debt to stock prices themselves. (Or at least the activity can stop prices from falling into an abyss.)

What the Fed cannot do, however? The Fed cannot create customers out of thin air.

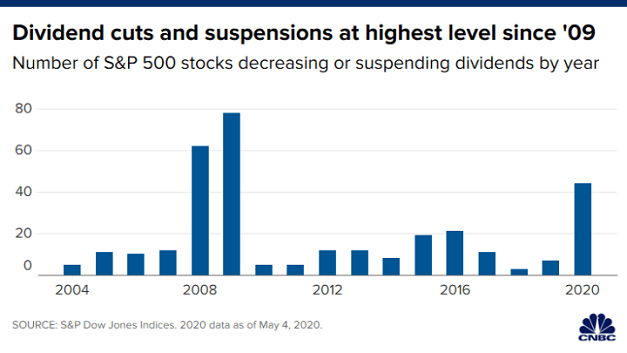

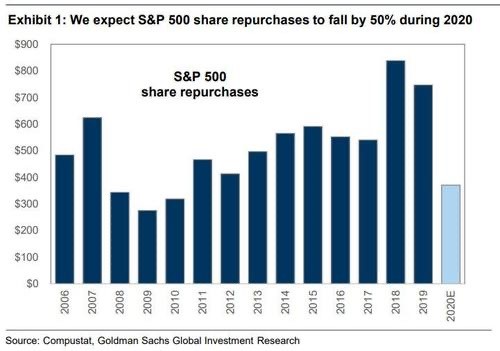

If pandemic-induced hardship adversely affects longer-term demand for goods and services, corporations generate less and less revenue. With less revenue, there is less money to pay back obligations (bonds), offer dividends and/or engage in share buybacks (stocks).

The dividends cuts/suspensions have barely even started, and…

… the decline in buybacks may be wildly underestimated.

Again, the Fed can pump dollars into the system where market participants can choose to speculate on the “work-remotely” economy. Certainly, Jim Cramer will direct you to the hashtag-winners in “work-from-home” technology, life sciences, e-commerce and mega-caps like Facebook (FB), Apple (AAPL), Amazon (AMZN) and Microsoft (MSFT).

Still, when investors pile into a tiny portion of the overall stock pie, the valuations of these companies eventually decouple from common sense. Investors rethink their premises. And the wildly overvalued leaders head down to meet their less vibrant cohorts.

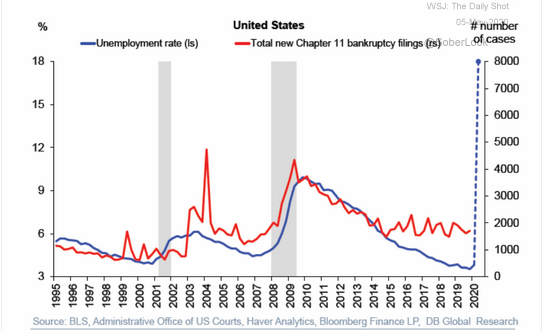

Those who see the Fed intervention as doing enough are not cognizant of the credit cycle realities. When people/businesses cannot get enough credit, when the skyrocketing unemployment rate adversely impacts demand for goods and services, when corporations simply cannot generate enough cash flow to cover their liabilities, they seek bankruptcy protection. Sooner or later, the stock market responds to the accumulation of bankruptcies.

I’ve said it before and I will say it again. This bear won’t end until the Fed is buying stock ETFs. Yet they won’t be buying stock ETFs to directly hold up equity markets until a second collapse in faith occurs. Right now, stocks are sufficiently off their March 23 lows to keep the Fed from firing the ultimate bazooka.

In the meantime, many of our moderate growth and income clients continue to benefit from our tactical shift in February. For the time being, rather than a 60-65 stock target/30-35 income target, our allocation remains protective.

The 33% equity component may be split between large-cap domestic ETFs and select individual securities. In the ETF space, we have been favoring Vanguard Megacap (MGC), iShares S&P 100 (OEF) and/or Vanguard S&P 500 (VOO). Our individual securities include the stock shares of select companies such as Pepsico (PEP), Adobe (ADBE), Abbvie (ABBV), Fortinet (FTNT), Wheaton Precious Metals (WPM), Johnson & Johnson (JNJ) and Crown Castle (CCI).

The 33% income component has been largely assigned to Treasuries and shorter term investment grade like Vanguard Short Term Corporate (VCSH). We also incorporate muni bonds in taxable accounts, Invesco Dollar Bullish (UUP) and a number of digital storage REIT preferreds from Digital Realty Trust (DLR) and QTS Realty Trust (QTS).

The rest is in cash. My Registered Investment Adviser may not be Warren Buffett’s Berkshire Hathaway, but we certainly appreciate the “optionality” of cash.

Would you like to receive our weekly newsletter on the stock bubble? Click here.