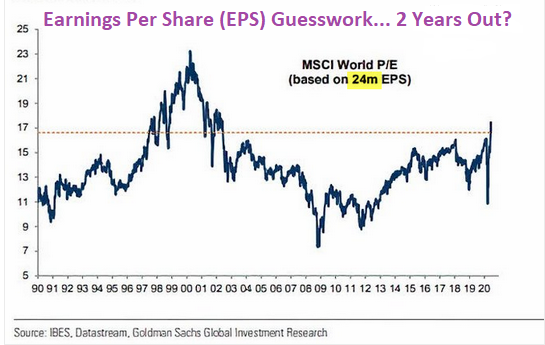

Some analysts have resorted to rationalizing the stock bubble with never-before-seen valuation measures. To wit, if one ignores the past 12 months (Trailing P/E), and disregards projections for the next 12 months (Forward P/E), the 24-month forward “guestimate” for MSCI All-World companies is suggesting that current stock prices are reasonable.

Are you buying this malarkey? Then you may wish to pick up some swamp land in Arkansas.

If investors always chose to look past recessions with unreliable forward earnings projections 24 months out, there would never be any stock declines. A future recovery in profits would always “justify” paying extraordinary premiums in the present.

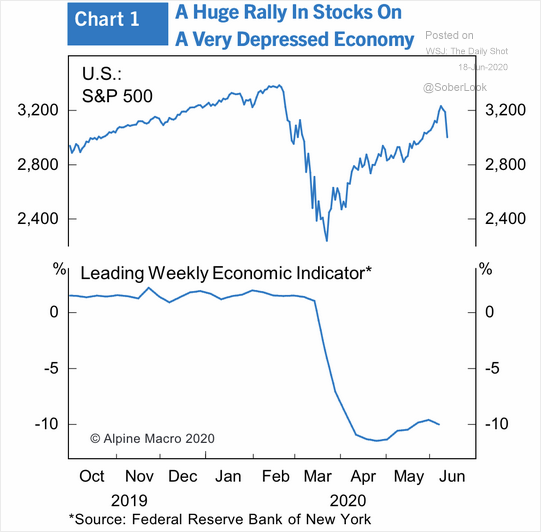

Indeed, this is the Federal Reserve’s pursuit. Bolster asset prices at all costs so that financial market participants brush aside macro-economic realities and corporate fundamentals.

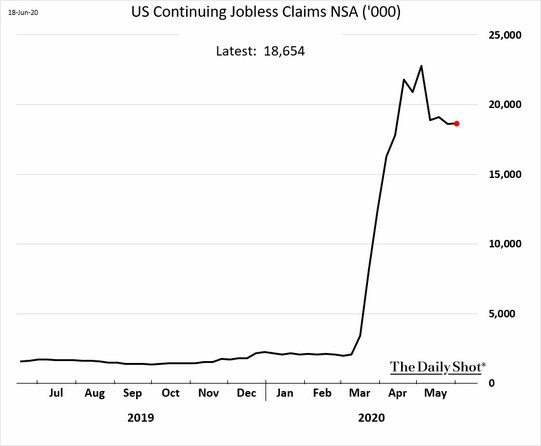

Let’s be candid. The job recovery will take far more than two years to sort itself out.

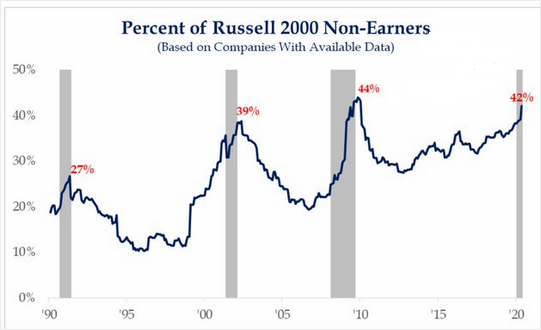

Worse yet, an ungodly percentage of smaller corporations are struggling to make money. And they were struggling before the pandemic.

Meanwhile, public corporations with debt servicing costs that exceed their earnings is approaching 20%. These are dead companies walking.

Does any of this matter? Not to panicky buyers of the stock bubble. Apparently, no price is too high for post-pandemic beneficiaries in e-commerce, e-payment and online entertainment.

Would you like to receive our weekly newsletter on the stock bubble? Click here.