Popular media personalities wanted you to believe that this bear market would be “stick-saved” by the Q4-2018 bottom. Yet hope is not a bear market survival strategy.

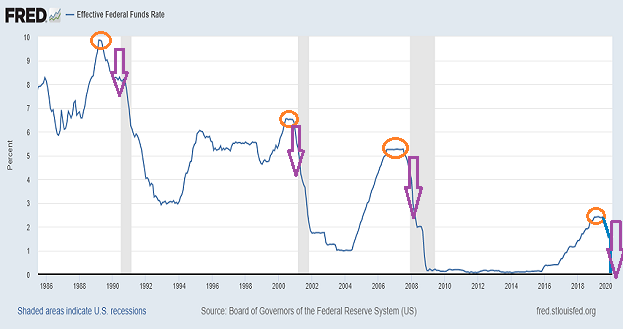

Even the idea that we’d see a miracle turnaround in 2020 the way that we did during Christmas in 2018 was problematic. Back then, the Federal Reserve had gobs of ammunition to flip policy on a proverbial dime. They ended their rate hiking campaign as well as promised to terminate reductions on their balance sheet. They even hinted at future rate cuts.

Today? The Fed has already dropped the overnight lending rate like a hot yam, taking it all the way down to 0% from 2.25%. Not only is this insufficient to avoid economic contraction, but stock bears rarely tap out at 30% during a recession.They’re more likely to be associated with 40%-50% losses. (Never mind that this time around, we started with the highest stock valuations in history.)

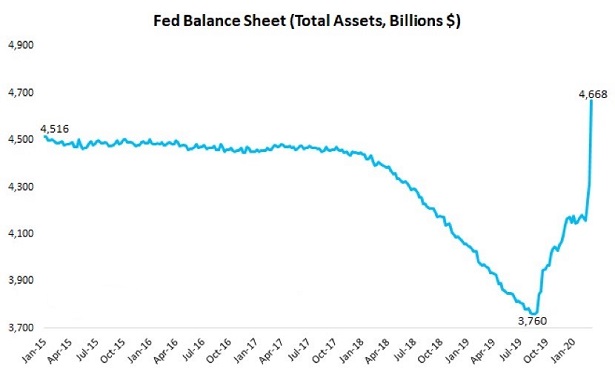

Additionally, the fabulous folks at the Fed have been feverishly purchasing hundreds of billions in Treasuries and mortgage-backed securities. They’ve already set a brand new record for their balance sheet, but it still hasn’t inspired investors to take risk yet.

Sadly, the Fed still needs to figure out a way to get bidders for short-term corporate credit. Absent a quick resolution, one should bank on a credit crisis every bit as agonizing as subprime in 2008.

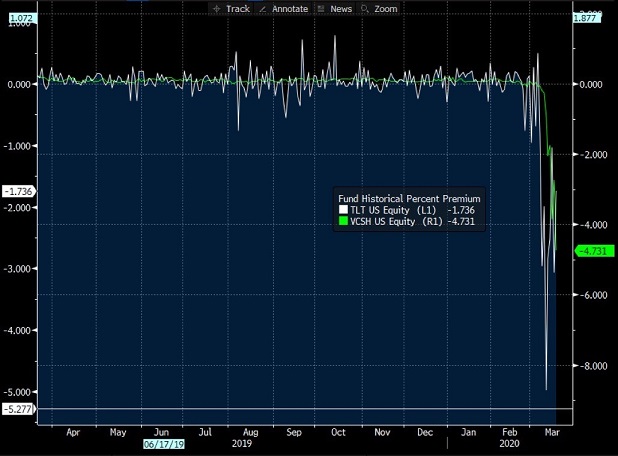

Short-term corporate credit ETFs like iShares Short Maturity Bond (NEAR) and Vanguard Short Term Corporate (VCSH) trade at a 4%-6% discount to Net Asset Value (NAV). They’re supposed to trade “near” NAV at all times.

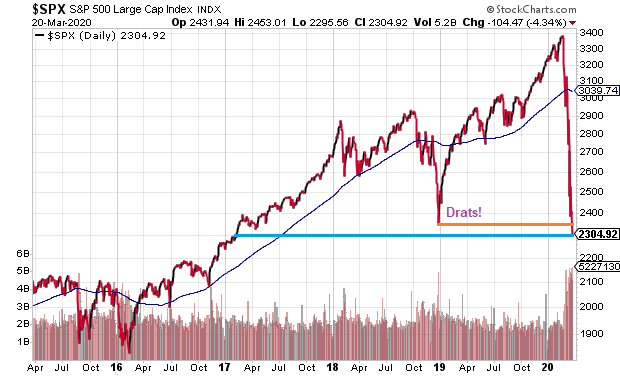

Even if the Fed finds a way to restore liquidity to bond land, from commercial paper to repurchasing agreements, from short-term corporates to munis, from preferreds to convertibles, they cannot alter the “Iron Rule.” Specifically, reversion back the mean (regression to the trend) suggests that the bottom would be a 57.6% decline to the 1400 level for the S&P 500.

Granted, nobody wants to think about the prospect of reversion to the mean in stocks. If it makes one feel better, we could bottom out at a median S&P 500 P/E of 14.82 around the 1970 level.

Problem there is that stocks rarely stop at a fair value P/E level on the bearish path downward. Markets tend to overshoot.

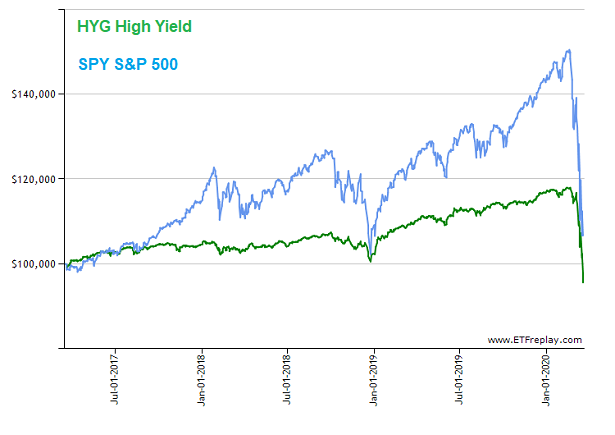

Even if one rejects the notion of reversion to the mean that could take us to 1400 on the S&P 500, or a median S&P 500 valuation level of 14.82 that could take us to 1970, one might need to concede that 2300 is not the bottom. Total returns for high yield bonds here in 2020 definitively cracked the Christmas 2018 lows, all but ensuring that the S&P 500 will follow suit.