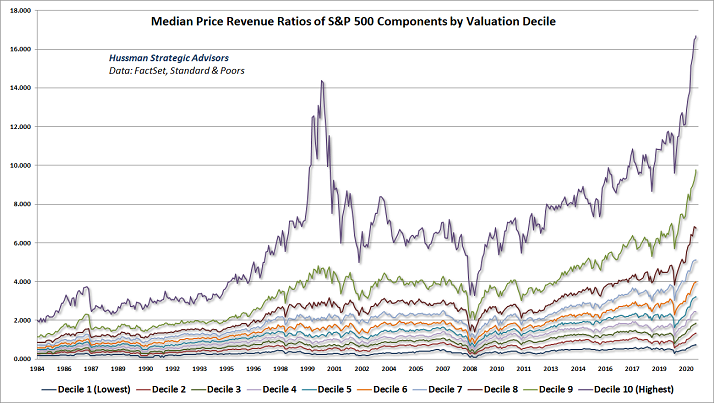

Theoretically, the extent of corporate success (e.g., sales, profits, cash flow, financial health, etc.) propels stock prices. That is no longer the case.

For example, one can examine the price-to-sales metric (P/S) by S&P 500 decile. Low valuation deciles might include sectors like industrials as well as brick-n-mortar retail. High valuation deciles might include economic segments like biotechnology and information technology.

The result? Every decile resides at a historical valuation extreme. And that means prices are dramatically outpacing revenue gains across the stock board.

If corporate success is not the key driver of stock prices, then what is? Federal Reserve monetary policy.

The Fed creates digital dollars to acquire mortgage bonds and Treasury bonds. Not only does the activity manipulate interest rates lower than they’d otherwise be, but bond sellers find themselves with cash that they put to work in riskier assets. Stocks get bid up accordingly.

Perhaps one could argue that the Fed’s quantitative easing (QE) activity was necessary during the pandemic and corresponding recession. Trillions of additional dollars on the Fed’s balance sheet gave investors the confidence to buy the 2020 collapse in faith.

But now?

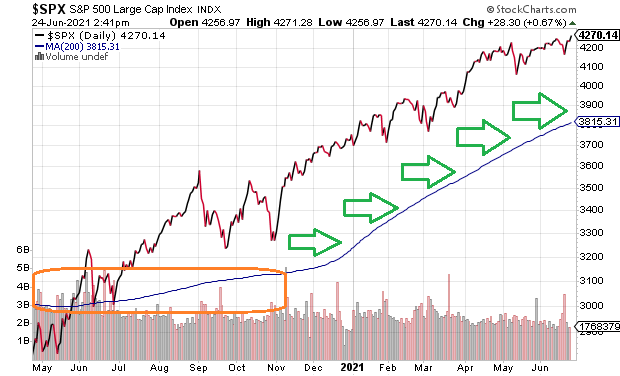

Today, things are just getting silly. The S&P 500 barely responds to anything other than what the Fed does. (Or says that it will do.)

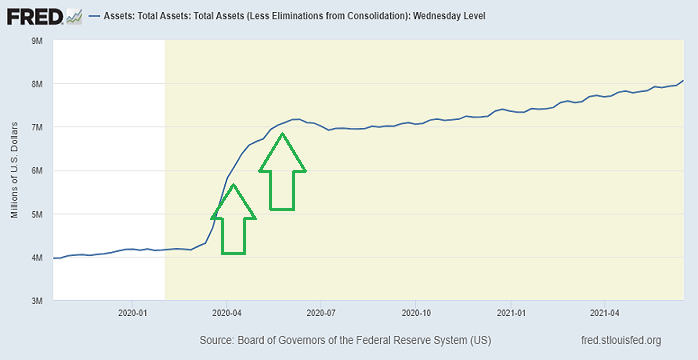

When the Fed balance sheet declined from a record peak in June of 2020, stock prices began to slide. The Fed then stabilized its balance sheet for a number of months around the $7.00-$7.20 trillion level.

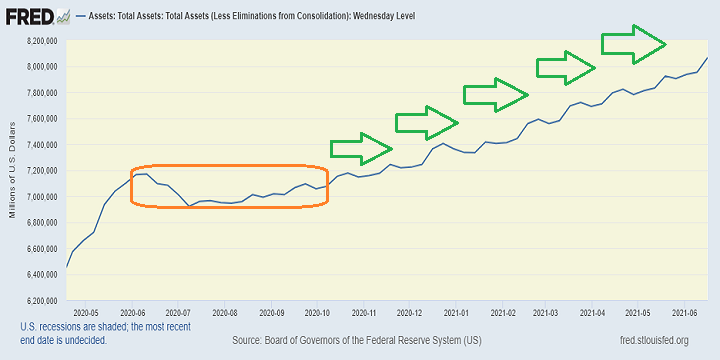

Yet even that was not good enough. By October of 2020, the Fed became more aggressive, recently pushing its assets beyond the $8.00 trillion mark. Stocks have been ratcheting up alongside the balance sheet highs.

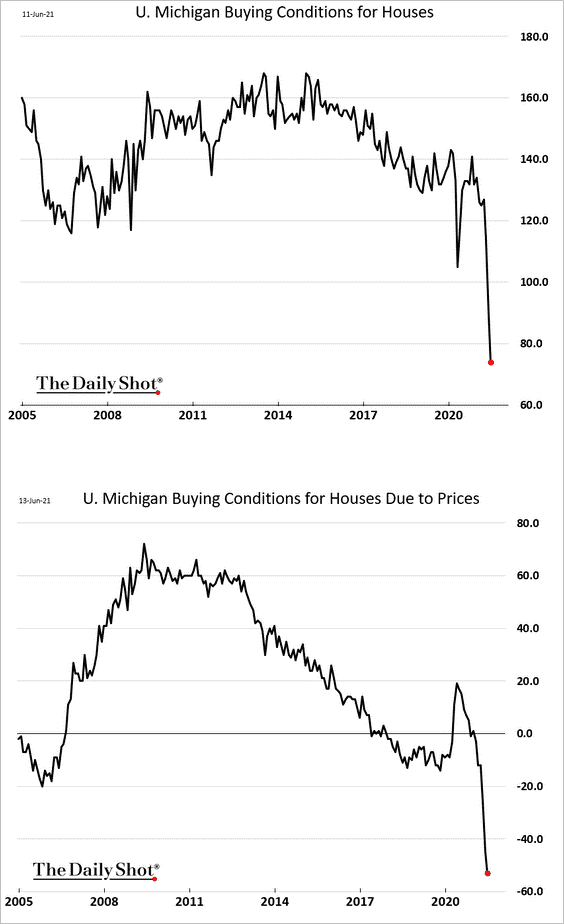

Stocks are not the only assets getting bid up to ridiculous peaks. Homeowners are particularly encouraged with residential real estate up somewhere in the order of 18% year-over-year.

Of course, even the red hot real estate market may cool. And quickly.

Dramatically lower interest rates made it possible for more buyers to afford real estate purchases. With a significant increase in buyers overwhelming a limited number of sellers and/or new construction, home prices skyrocketed.

However, prices have appreciated to the point whereby the buying public is becoming discouraged. Sellers in the year ahead might be selling significantly lower than those who have already cashed in.

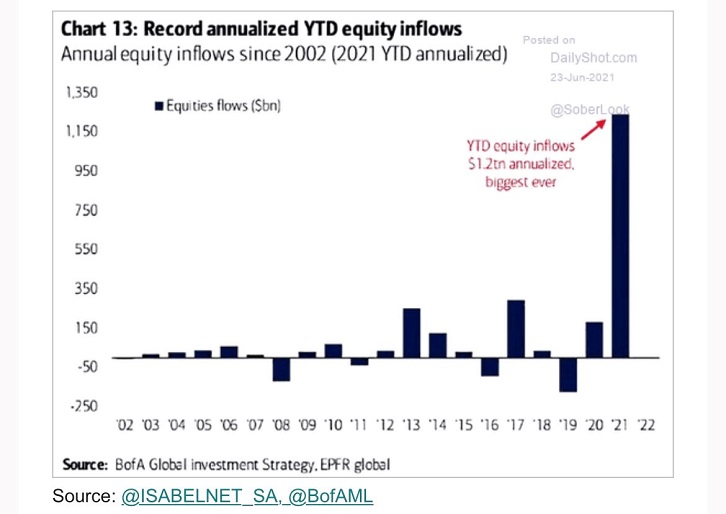

What about the stock market bubble? The way that mutual funds and exchange-traded funds continue to add record-breaking inflows, one wonders if stocks could be in for a rude awakening.

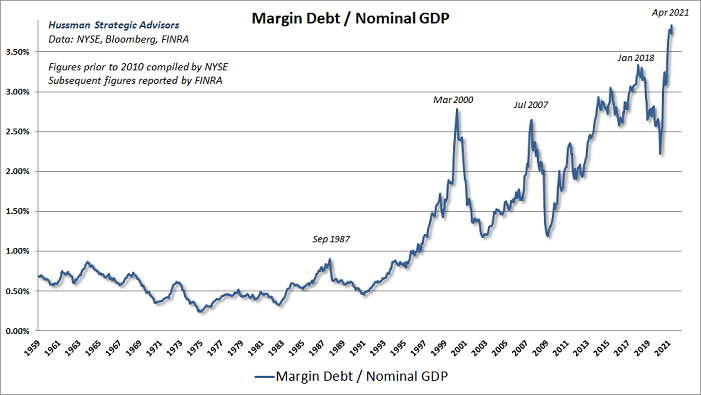

Similarly, one ponders the carnage that could occur when margin debt unwinds in earnest. The results were less than pretty leading into the crash of 1987, the tech wreck of 2000, the housing crisis of 2008, and the Fed’s monetary policy tightening of 2018.

The worst part? Stocks, bonds and real estate not only depend on a stimulating Fed, but on the expectation of never-ending easy money in the future.

There are reasons why never-ending Fed accommodation is unlikely (e.g., potential for hyperinflation, loss of faith in the financial system and/or the dollar, etc.). It follows that when catalysts drag the Fed toward meaningful monetary tightening, stocks could plummet precipitously.

Would you like to receive our weekly newsletter on the stock bubble? Click here.