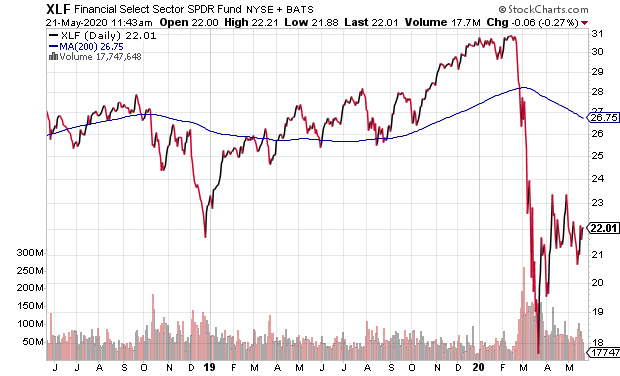

The notion that the bear market for U.S. stocks has ended is fanciful. For example, is it really the case that financial firms are on the mend? They’re restricting access to credit, increasing reserves for loan losses and showing few signs of resilience beyond a bounce of mutli-year lows.

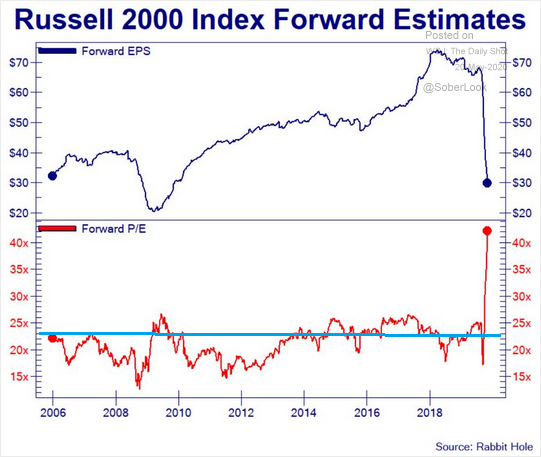

In a similar vein, while mega-cap companies in the Nasdaq 100 or S&P 500 get most of the attention, small companies are the lifeblood of the U.S. economy. Their forward earnings projections for May of 2021? About what they were in May of 2006.

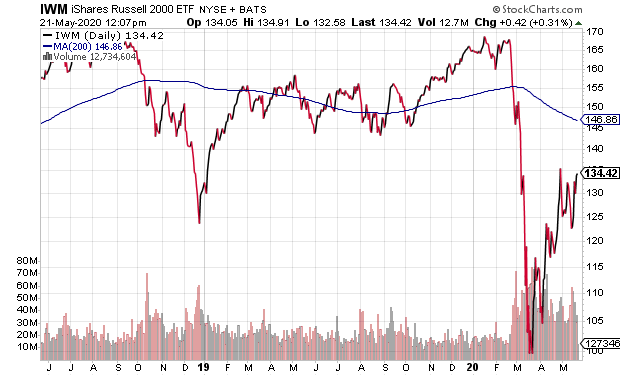

Perhaps shockingly, investors are currently willing to pay 46x forward earnings per share at a price of 1346. At 23x, or “fair value,” the iShares Russell 2000 ETF (IWM) would need to fall 50% to 67.21.

Granted, the federal government and the Federal Reserve will due everything under the sun to reflate the stock bubble. Nevertheless, over-the-top bullishness rarely turns out well.

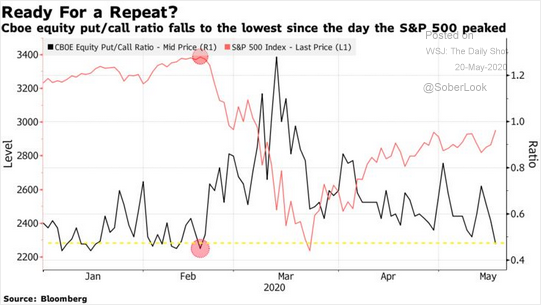

Consider the fact that the put-call ratio has dropped all the way back down to levels not seen since the complacency exhibited at February’s all-time highs. That is more likely a sign of stock selling pressure to come than a signal to invest more aggressively in expensive equities.

Every investor may wish to cheer the U.S. economy’s grand reopening. Indeed, nearly every state has eased stay-at-home policies, including California.

On the flip side, there’s little chance of an economic recovery that reaches pre-crisis levels before Q4 2022 or Q1 2023. Do the math. U.S. GDP grew by roughly $1 trillion in 2018. It grew by roughly $850 billion in 2019. We will end the year down $1.75 trillion (or more) in 2020. If we were remarkably fortunate to grow at pre-crisis levels in 2021 and 2022, GDP would be back somewhere in Q4 2022 or Q1 2023.

Even then, unemployment is likely to remain elevated. That may make it difficult on a services-oriented economy.

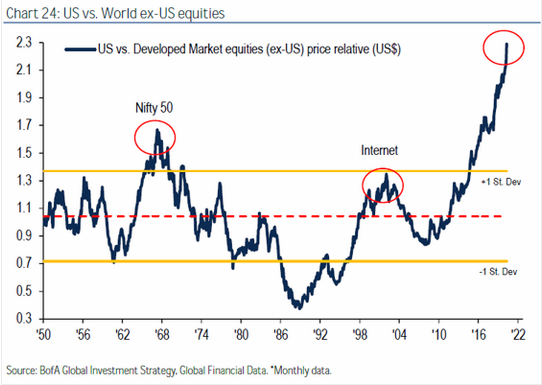

Foreign developed markets seem to grasp reality far better than U.S. markets do. And that goes a long way toward explaining the mutli-generational discrepancy in the price people are paying to own U.S. stocks over Ex-U.S. stocks.

It follows that the U.S. stock bubble may be exhibiting a V-like market snap-back in a U-shaped economic recovery. Smart investors may see the “V” as little more than the first half of a “W.”

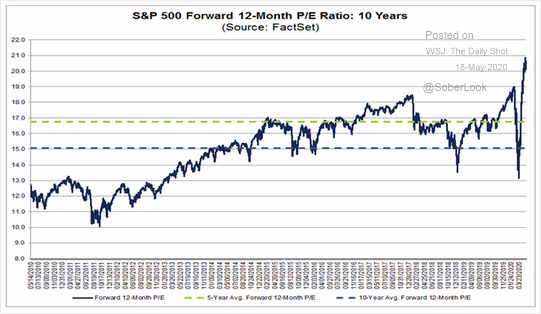

Keep in mind, when the earnings picture has been decidedly murky in the past, investors have chosen to pay a lower price for S&P 500 exposure. The average forward multiple 12 months out? 13.6.

With the S&P 500 at 2950, and non-GAAP earnings per share at $139.13, the Forward P/E is 21.2. To get to the average Forward P/E, the S&P 500 would need to fall 35.8% to 1894.

The financial media have already dismissed all of 2020’s earnings. Worse yet, they’ve resorted to explaining why earnings 12 months from now do not matter. One CNBC contributor actually said, “Stocks look attractive relative to 2022 earnings expectations.”

If mainstream pundits were more truthful, they’d explain that fundamentals have not mattered for a very long time. What does matter? Federal Reserve intervention.

The Fed is buying Treasuries. They’re buying mortgage-backed bonds and munis. They’re even buying quality corporate bonds as well as junk bond ETFs. The near-limitless liquidity indirectly props up equity prices, regardless of price.

Still, the Fed’s monstrous contribution to the money supply is likely to fall short as economic realities come to the forefront. Defaults. Bankruptcies. The wave of insolvencies cannot be papered over entirely by Fed liquidity.

In essence, corporate restructurings as well as defaults will render the Fed’s indirect support for stocks insufficient. Then the stock market will move sharply lower on the second leg of the W-shaped recovery for U.S. stocks.

Yes, the Fed will then take the next step. Like Japan, the Fed (and the Treasury) will find a way to buy hundreds of billions of dollars in stock ETFs. That’s when a more meaningful equity bull will begin.

If you find that you are uncomfortable with a Buffett-like cash position of 33%, or if you have some money that you’d still like to put to work right now, there are a few individual stocks that may be promising. You’ve got Constellation Brands (STZ) that has been able to maintain double-digit profit margins in the middle of a corona-virus shutdown. And for the tech-obsessed, few stocks have analysts raising earnings projections (as opposed to slashing them) the way they have for Dropbox (DBX).

Would you like to receive our weekly newsletter on the stock bubble? Click here.